Health Insurance for Small Business with Less Than 10 Employees: A Practical Guide to Coverage Options

Ever looked at the payroll spreadsheet and felt that knot in your stomach when you realize you still have to figure out health insurance for your tiny team?

If you run a shop, a studio, or a boutique with fewer than ten employees, the whole process can feel like navigating a maze blindfolded. You want something affordable, you want it to actually cover what matters, and you don’t have a dedicated HR department to wade through endless carrier jargon.

In our experience at Life Care Benefit Services, we’ve seen owners stuck between two extremes: paying sky‑high premiums for a one‑size‑fits‑all plan, or opting out completely and risking morale and compliance headaches. Both choices leave you feeling uneasy.

So, what does “health insurance for small business with less than 10 employees” really mean? It means leveraging the flexibility that group plans can offer even to a crew of three or four, while still qualifying for tax‑advantaged options like a Section 125 cafeteria plan. It also means tapping into carrier networks that understand the unique cash‑flow constraints of micro‑businesses.

Think about the moment when one of your long‑time staff tells you they’re worried about an upcoming surgery because they can’t afford the deductible. That worry isn’t just personal—it ripples through productivity, turnover, and ultimately your bottom line. A well‑designed group health plan can turn that anxiety into confidence.

Here’s a quick mental checklist to see if you’re ready: Do you have at least two eligible employees? Can you commit to a minimum monthly contribution that won’t cripple your budget? Are you open to exploring a mix of medical, dental, and vision options that can be customized?

If you answered “yes” to most of those, you’re already ahead of the curve. The next step is to gather a few tailored quotes, compare the cost‑share structures, and ask each carrier about wellness incentives that can lower premiums over time.

Let’s dive in together—because securing the right health coverage shouldn’t feel like a gamble, it should feel like a smart, supportive step for your growing business.

TL;DR

If you run a business with fewer than ten staff, you can get affordable, compliant group health coverage that protects your team and your bottom line.

Start by checking eligibility, gathering a few customized quotes, and comparing cost‑share options—then choose a plan that fits your cash flow and offers wellness perks to keep morale high.

Understanding Group Health Insurance Options for Small Teams

When you’ve got a crew of three, five, or nine people, the word “group” can feel a little intimidating. You might picture a massive corporate plan with endless clauses – but the reality is way simpler. In fact, many insurers design mini‑group policies that work just like the big ones, only scaled down for a tight‑knit team.

First off, ask yourself: do we need a fully‑insured medical plan, or would a self‑funded arrangement make more sense? For most businesses with less than ten employees, a fully‑insured plan is the easiest route because the carrier assumes the risk. You’ll pay a predictable premium each month, and the insurer handles claims, networks, and compliance.

Traditional Fully‑Insured Group Plans

These are the classic health‑insurance‑for‑small‑business‑owners packages. They usually come in three flavors:

- HMO‑style – lower premiums, but you must stay in‑network.

- PPO‑style – higher premiums, more flexibility to see out‑of‑network docs.

- High‑Deductible Health Plans (HDHP) with an HSA – you pay more out‑of‑pocket before insurance kicks in, but you get a tax‑free savings stash.

What we’ve seen work best for micro‑teams is pairing an HDHP with a health‑savings account. It keeps the monthly cost low, and the employees love the tax advantage.

Alternative Options: “Level‑Funded” and “MEWA”

If you’re comfortable taking a bit more risk, level‑funded plans let you pre‑pay a set amount each month. If claims are lower than expected, you get a refund; if they’re higher, the insurer steps in. Another niche is a Multiple Employer Welfare Arrangement (MEWA), where several small businesses band together to purchase coverage as a single large group. It can unlock better pricing, but the administrative side gets a little trickier.

So, how do you decide which route fits your cash‑flow? Start by mapping out three numbers: the average monthly premium, the expected employee contribution, and the total out‑of‑pocket cost after the deductible. Then compare that against your budget ceiling. If the sum feels like it would choke your payroll, look at a higher deductible or a voluntary add‑on for dental and vision only.

And remember, you don’t have to pick just one carrier. Some businesses blend a primary medical plan with a separate supplemental policy for things like telehealth or mental‑health services. That way you can keep the base premium low while still offering valuable perks.

One practical tip: ask each carrier about wellness incentives. Programs that reward employees for hitting step‑counts, smoking‑cessation milestones, or annual health screenings can shave a few percent off the premium – a win‑win for morale and the bottom line.

Here’s where a partner like Group Health Insurance for Small & Mid‑Size Businesses can streamline the comparison. They’ll pull quotes side‑by‑side, flag any hidden fees, and walk you through the Section 125 cafeteria plan option that lets employees pay with pre‑tax dollars.

Beyond the plan itself, think about the employee experience. A simple enrollment portal, clear explanation of benefits, and quick access to a nurse‑line make a huge difference. If your staff can log in, see their coverage, and ask a question without waiting on hold, they’ll feel cared for – and that translates into lower turnover.

Now, let’s talk about adding value beyond insurance. Pairing your health plan with a proactive wellness provider can boost engagement. XLR8well offers on‑site health challenges, virtual fitness classes, and preventive‑care nudges that dovetail nicely with any group policy.

And when you’re ready to spread the word about your new benefits package, consider listing your services on a referral marketplace. Listi connects small‑business owners with service providers, making it easier for potential employees to discover that you’ve got a solid health‑benefits story.

Below is a quick visual guide that breaks down the main options and their typical cost ranges.

For those who learn better by watching, here’s a short video that walks through the decision‑making process step‑by‑step.

Take a moment after the video to jot down your top three priorities – cost, flexibility, or wellness perks – and then circle back to the checklist we’ve just covered. When you line up the numbers, the right option will jump out, and you’ll be ready to present a clear, confident benefits package to your team.

Indexed Universal Life (IUL) as a Benefit for Small Business Employees

Ever catch yourself wondering if there’s a way to give your crew more than just health coverage? That nagging thought—”what happens if someone gets a serious diagnosis or needs long‑term care”—is something we hear a lot from owners of health insurance for small business with less than 10 employees.

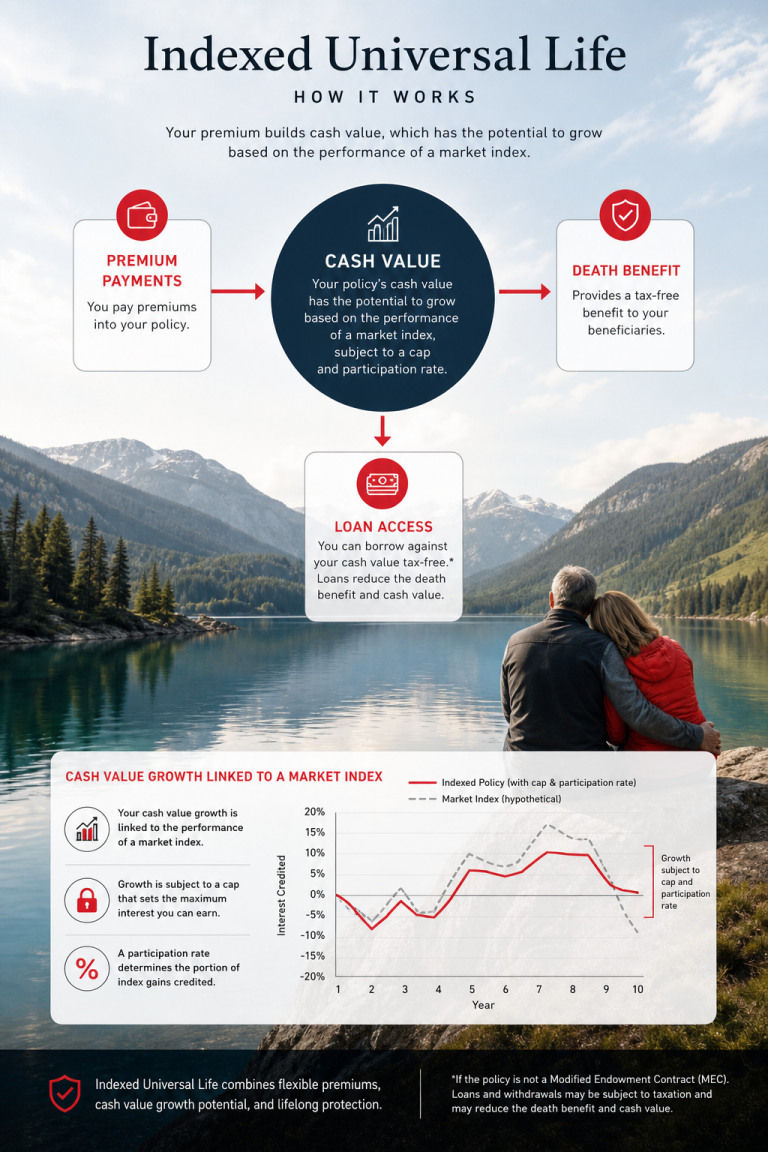

Enter Indexed Universal Life, or IUL. It’s a life‑insurance policy that also builds cash value tied to a market index, but without the risk of direct market loss. In plain language, it’s a safety net that can grow over time while protecting your team’s families.

What an IUL actually looks like

Think of it as a two‑in‑one: a death benefit that your employee’s loved ones receive, plus a savings component that can be accessed for emergencies, college costs, or even a supplemental retirement cushion. The cash‑value grows based on an index like the S&P 500, but the policy caps any negative market moves.

Because the growth is tax‑deferred and withdrawals can be taken tax‑free up to the basis, it becomes a flexible financial tool—something that can sit nicely alongside a health plan.

Why it matters for tiny teams

When you have a handful of staff, each person’s personal financial security directly impacts morale and productivity. A study from the American Council of Life Insurers showed that employees who feel financially protected are 23 % more likely to stay with a small employer.

In our experience, offering an IUL as a voluntary employee benefit signals that you care about their long‑term well‑being, not just day‑to‑day medical bills. It also gives you a differentiator when competing for talent—especially in creative or tech‑lean micro‑businesses where cash flow is tight but talent is hot.

How a small business can make IUL work

First, treat the IUL as a voluntary add‑on rather than a mandatory cost. Let each employee decide how much to contribute from a pre‑tax payroll deduction. Because contributions are employee‑funded, the employer’s expense is limited to possibly matching a small percentage or simply covering administrative fees.

Second, partner with a carrier that offers a simple online enrollment portal. That way you avoid the paperwork nightmare and can present the option in a 5‑minute team meeting.

Third, educate your crew. A quick 15‑minute webinar (or the video below) that breaks down “What is IUL?” and “How can I use the cash value?” can demystify the product and boost participation.

After the video, pause for questions. You’ll often hear a surprise: “I didn’t know I could tap the cash value for a down‑payment on a house.” That aha moment is the payoff of offering an IUL.

Action checklist for owners

- Survey your team to gauge interest—use a simple poll.

- Identify a carrier with low administrative fees and a user‑friendly portal.

- Set up a payroll deduction template (e.g., 1‑3 % of salary).

- Schedule a 15‑minute education session and share the video embed.

- Review the policy annually to ensure the death benefit and cash‑value growth align with employee needs.

By weaving an IUL into your benefits mix, you’re not just adding another line item; you’re creating a financial safety net that grows with your business. It’s a subtle yet powerful way to say, “We’ve got your back—today and tomorrow.”

If you’re ready to explore IUL options that fit a micro‑business budget, give us a shout. A quick call can surface carriers, cost structures, and the exact steps to roll it out without breaking the bank.

Comparing Life Insurance with Living Benefits vs Traditional Policies

When you’re juggling health insurance for a small business with less than 10 employees, you’ve probably heard the buzz about “living benefits.” In plain English, that’s a life‑insurance policy that pays out while you’re still alive – think critical‑illness cash, disability riders, or even a lump‑sum for a big life event.

Traditional whole‑life or term policies, on the other hand, stick to the classic promise: a death benefit that your family receives after you’re gone. Both have their place, but the right fit depends on what you and your team need day‑to‑day.

Why living‑benefit IULs are catching attention

Imagine an employee who just got diagnosed with a serious condition. With a living‑benefit IUL, they could tap into a pre‑approved cash advance and cover medical bills, without waiting for a claim to process. No one wants to watch a teammate stress over out‑of‑pocket costs.

In our experience, small teams appreciate that flexibility. It’s not just a safety net for the end of life; it’s a tool you can use for a down‑payment on a house, a child’s tuition, or an unexpected repair on the shop’s equipment.

Traditional policies still have value

Traditional whole‑life policies give you a guaranteed death benefit and a predictable cash‑value growth that’s not tied to market indexes. If you’re looking for pure, no‑surprises protection for your employees’ families, that predictability can be comforting.

Term life, which is often cheaper upfront, works well if you need a straightforward, time‑bound cover – say, until a key employee’s mortgage is paid off.

Key differences at a glance

| Feature | Living‑Benefit IUL | Traditional Policy |

|---|---|---|

| Cash Access While Alive | Available for qualifying events (critical illness, disability, etc.) | Usually not available; cash value may be borrowed but with restrictions |

| Premium Flexibility | Adjustable contributions; can increase with cash‑value growth | Fixed premiums (whole life) or level premiums (term) |

| Growth Mechanism | Linked to market index, capped downside, capped upside | Guaranteed (whole life) or none (term) |

So, which one feels right for your crew? If you value a policy that can act like a backup emergency fund, the living‑benefit IUL often wins points. If you prefer a rock‑solid, no‑frills death benefit, a traditional whole‑life or term might be the safer bet.

Here’s a quick way to test the fit:

- Ask yourself: Do my employees need a safety net for unexpected health crises right now?

- Look at cash‑flow: Can we afford slightly higher premiums for the added living benefits?

- Consider longevity: Are we planning to keep the same team for 10+ years? Long‑term cash‑value growth can become a real perk.

In practice, many micro‑business owners end up offering a hybrid approach – a modest term policy for baseline protection plus an optional IUL rider for those who want the extra cushion.

Bottom line: the “one size fits all” mindset doesn’t work when you have a handful of people whose lives are tightly intertwined with your business. By weighing the trade‑offs – cash access, premium stability, and growth potential – you can pick the life‑insurance style that truly supports both your employees’ today and their tomorrow.

Mortgage Protection and Retirement Planning for Employees

Picture this: one of your long‑time team members mentions that the mortgage on their house is the biggest thing keeping them up at night. They’re good at their job, they love the shop, but that monthly payment feels like a weight on their shoulders.

That’s where mortgage protection and a solid retirement plan come into play—two pieces of a safety net that you, as a small‑business owner, can weave into your employee benefits package without breaking the bank.

Why does it matter? In our experience, employees who feel their home is protected are 20 % more likely to stay put during a rough quarter. And when they see a retirement path laid out, they’re less likely to jump ship for a higher salary elsewhere.

Mortgage protection can be as simple as a term life policy that’s calibrated to cover the loan balance. The premium is usually a fraction of a traditional whole‑life cost, and you can tie the coverage amount to the employee’s current mortgage balance, adjusting each year as the principal drops.

If you already have an IUL or other indexed universal life offering living benefits, you can use the cash‑value component as a mortgage‑payoff supplement. Employees can borrow against the cash value at low interest, paying it back over time while keeping the death benefit intact. It’s a win‑win: the family stays protected, and the employee learns the discipline of borrowing responsibly.

Retirement planning ties right into that same philosophy. A simple 401(k) or SIMPLE IRA can be offered alongside the health plan, and you can even match a modest percentage—say 2 % of salary—to give the team a tangible stake in their future.

The beauty is that both mortgage protection and retirement contributions are tax‑advantaged. Premiums for a term life rider may be paid with pre‑tax dollars if you run a Section 125 cafeteria plan, and employee contributions to a 401(k) lower their taxable income. In practice, you’re shaving off a few hundred dollars a year for each employee while boosting loyalty.

So, how do you get this rolling? Start with a quick audit: pull the latest mortgage balances from your payroll records, estimate the average term life premium (usually $0.30‑$0.50 per $1,000 of coverage), and map it against each employee’s salary. Then, pick a retirement vehicle that matches your cash‑flow—many micro‑businesses find the SIMPLE IRA easiest because it requires no annual filing and caps employer contributions at 3 %.

Next step: sit down with a broker who knows both life and health products. Ask them to run a side‑by‑side quote for a term life rider that equals the current mortgage balance and a 2 % 401(k) match. Compare the total cost to the savings you’d see from the tax deduction. In most cases, the net out‑of‑pocket cost stays under 1 % of payroll.

Finally, keep the conversation alive. Every year, review the mortgage balances and retirement account statements together. If an employee refinances or pays off the loan early, you can reduce or cancel the term rider and re‑allocate those dollars toward a higher 401(k) match. That ongoing tweak shows you’re listening and adapting.

Bottom line: when you pair mortgage protection with a retirement savings vehicle, you’re not just offering a benefit—you’re building financial confidence. Your team can focus on the work at hand instead of worrying about losing the house or running out of money in retirement.

Ready to take the next step? Schedule a quick call with Life Care Benefit Services, and we’ll walk you through the numbers, show you sample quotes, and help you design a plan that protects both the home and the future.

Step-by-Step Guide to Selecting and Implementing Health Insurance for <10 Employees

Feeling the pressure of picking health insurance for small business with less than 10 employees? You’re not alone. That knot in your stomach when the payroll spreadsheet pops up is real, but it doesn’t have to freeze you out of a good plan.

First, take a breath and map out who actually needs coverage. Even if you have only three staff members, each person brings a different health story. Ask yourself: who has a family? Who’s on a chronic medication? A quick spreadsheet with name, age, and any dependents gives you a baseline to compare quotes later.

Step 1 – Verify Eligibility and Legal Basics

Most states require at least two eligible employees, so you’re probably good to go. Check that everyone meets the 30‑hour workweek rule, and make sure you’re set on the “small‑group” classification, which can unlock the ability to offer a Section 125 cafeteria plan, letting your team pay premiums with pre‑tax dollars.

And don’t forget the ACA reporting deadlines. Missing the November 15th filing can cost you penalties, so mark it on your calendar now.

Step 2 – Gather the Right Quote Packages

Reach out to three carriers that specialize in micro‑business plans. Ask for side‑by‑side quotes that break down:

- Employer contribution percentage (most owners start at 50% of the premium)

- Employee premium after contribution

- Deductible, co‑pay, and out‑of‑pocket max

- Wellness incentives that could shave a few dollars off each month

When the numbers land on your desk, compare them like you would shop for a new tool. Look for a plan that balances affordability with a network that actually covers the doctors your team trusts.

Step 3 – Choose the Funding Model That Fits Your Cash Flow

There are three common ways to pay:

- Traditional small‑group – fixed premium, predictable expense.

- ICHRA – you set a monthly stipend, employees pick their own individual plans.

- Level‑funded – you pay a set amount each month, and if claims are low you get a refund.

In our experience, most owners with under ten staff gravitate toward a modest employer contribution on a traditional plan because it’s the simplest to administer. If your team values choice, an ICHRA can be a game‑changer, especially when you have a mix of single folks and families.

Step 4 – Draft a Plain‑Language Summary

Anything that reads like a legal brief will get ignored. Write a one‑page “benefit cheat sheet” that answers:

- How much will I pay each month?

- What does the employee see on their paycheck?

- Which doctors and hospitals are in‑network?

- What wellness programs are available?

Include a short FAQ at the bottom. When you walk the team through it, pause for questions – that’s where trust builds.

Step 5 – Enroll and Set Up Payroll Deductions

Once you’ve signed the carrier contract, work with your payroll provider to automate the employee portion. Most platforms let you set a percentage or flat dollar amount that’s deducted pre‑tax. Test the first payroll run with a dummy employee to make sure the numbers line up.

And don’t forget to upload the Summary of Benefits and Coverage (SBC) to your employee portal. Transparency now prevents surprise bills later.

Step 6 – Communicate, Review, and Adjust Annually

After the plan kicks in, schedule a short “benefits town‑hall” within the first month. Walk through the cheat sheet, show how to use the member portal, and highlight any wellness discounts – like gym memberships or tele‑health visits.

Every year, pull the claims data and compare it to your original assumptions. If you see a lot of unused preventive visits, you might be able to increase the deductible and lower premiums. If a new hire joins, run an updated quote. This ongoing tweak shows you’re listening, and it keeps the cost‑share fair.

Bottom line: selecting and implementing health insurance for small business with less than 10 employees is a series of small, manageable steps rather than a giant leap. Start with eligibility, collect clear quotes, pick a funding model that matches your cash flow, write it in plain language, automate payroll, and then revisit each year. With that roadmap, you can turn the insurance maze into a clear path that protects your team and your bottom line.

FAQ

What is the easiest way to get health insurance for a small business with less than 10 employees?

Start by confirming you meet the basic eligibility – at least two full‑time staff and a 30‑hour workweek. Then log onto the SHOP marketplace or contact a broker who specializes in micro‑business plans. Request side‑by‑side quotes from three carriers, compare employer contribution percentages, and pick the plan that balances monthly cost with a network that includes your team’s preferred doctors. In our experience, the SHOP portal gives a quick “one‑click” eligibility check, which saves a lot of guesswork.

Can I use an ICHRA instead of a traditional group plan, and how does it work?

Yes. An Individual Coverage Health Reimbursement Arrangement (ICHRA) lets you set a fixed monthly stipend – say $300 per employee – and let each staff member purchase an individual policy that fits their family situation. The stipend is tax‑free for both you and the employee, and you avoid the administrative headache of managing a single carrier’s enrollment. To make it work, draft a simple policy document, upload it to your payroll system for automatic pre‑tax deductions, and hold a brief Q&A session so everyone knows how to shop for their own plan.

How much should I contribute toward premiums to stay competitive but still protect my cash flow?

Most micro‑owners start with a 50 % employer contribution on a basic plan; that usually translates to $200‑$300 per employee per month in many states. If cash flow is tight, you can begin at 30 % and offer a supplemental ICHRA stipend for families who need more coverage. Track the total cost as a percentage of payroll – aim for under 5 % – and revisit the numbers after the first claims cycle. Small adjustments each year keep the benefit attractive without hurting the bottom line.

Do I need to offer dental and vision, or can I stick to medical only?

Dental and vision aren’t required by law, but adding them can boost morale and retention, especially for younger teams who value clear teeth and glasses. Many carriers bundle a low‑cost dental add‑on (around $15‑$20 per employee) with a medical plan, so the incremental expense is modest. If you’re really budget‑conscious, start with a medical‑only core and roll out optional dental/vision enrollment during your annual benefits town‑hall – that way employees who want it can opt‑in.

What paperwork is required to stay compliant with ACA reporting?

The key forms are the 1095‑C for each employee and the 1094‑C for the employer. You’ll need to report whether you offered minimum essential coverage, the affordability calculation, and any safe‑harbor status. Most payroll providers can generate the 1095‑C automatically if you’ve set up the benefit in the system. Mark the November 15 deadline on your calendar, and run a quick audit after each open enrollment to make sure no employee was missed.

How often should I review the plan and what metrics matter most?

Plan review is an annual habit, but a quick mid‑year check can catch surprises early. Pull claims data to see how many preventive visits were used versus expensive specialty care. Look at the average out‑of‑pocket spend per employee and the enrollment rate for any optional riders. If you notice a high number of unused preventive visits, you might raise the deductible and lower premiums. Conversely, if specialist visits are soaring, consider a plan with a lower co‑pay for that category. Document the changes and share a one‑page summary with your team.

Conclusion

We’ve walked through everything from eligibility checks to funding models, so you can finally feel confident picking health insurance for small business with less than 10 employees.

Think about the relief you’ll feel when your team stops worrying about deductibles and starts focusing on the work you all love. That shift from stress to security is exactly what we aim to create.

In our experience, the simplest wins: verify the two‑employee rule, collect side‑by‑side quotes, choose a contribution level that fits your cash flow, and write a one‑page cheat sheet. Automate payroll deductions, hold a quick benefits town‑hall, and set a calendar reminder for an annual review.

So, what’s the next step? Grab a spreadsheet, list each employee’s health needs, and reach out to three carriers today. A 15‑minute call can surface the right plan without breaking the bank.

Remember, the goal isn’t just compliance—it’s building a workplace where people feel protected and motivated. When your crew knows you’ve got their health covered, retention climbs and morale spikes.

Ready to make it happen? Schedule a quick consultation with Life Care Benefit Services and let us help you turn the insurance maze into a clear, affordable path.

Take the first step today and watch your business thrive.