Picture this: you’re sipping coffee on a rainy Thursday morning, scrolling through your phone, and you stumble across a headline that says “What Is Life Insurance With Living Benefits?” The headline sparks a quick, almost guilty curiosity—what’s the deal? In a world where financial security feels more like a game of hide‑and‑seek, knowing that your life insurance can actually work for you while you’re still breathing can feel like finding a cheat code.

So, what exactly is this “living benefits” thing? Think of it as a safety net that’s not just waiting for a future event to pay out. Instead, it lets you tap into the policy’s value during your lifetime if you hit certain medical or financial milestones—like a hospital stay, a diagnosis, or even a sudden cash crunch. It’s like having a financial backup plan that can be activated before you’re gone.

In practice, the most common rider is the Accelerated Death Benefit. Imagine you’re diagnosed with a serious illness and the policy sends you a portion of the death benefit early, helping cover treatment costs or simply keeping your household budget afloat while you recover. Another popular option is the Long‑Term Care Rider, which can be used to pay for assisted living or in‑home care when you’re no longer able to manage daily tasks.

Now, let’s bring this to life. Suppose Sarah, a small‑business owner, purchased a policy with living benefits. Two years later, her small office faced unexpected equipment failure. The policy’s living benefit paid her a lump sum that covered repairs without dipping into her business savings. That’s the power of flexibility. It’s not a gimmick; it’s a concrete tool that can bridge gaps in unexpected times.

What’s great about these riders is that they’re built into standard life‑insurance products from the same insurers that offer traditional coverage. If you’re a homeowner, teacher, or small‑business owner, you can explore options like Indexed Universal Life or whole‑life policies that bundle living benefits right from the start. For more detail on how these work together, check out What Is Living Benefits Life Insurance? A Complete Guide for Homeowners, Teachers, and Small Business Owners.

But living benefits aren’t just about insurance. They’re about the overall health of your financial ecosystem. That’s why we often pair them with proactive health programs to keep premiums low and the policy’s value high. If you want to see how a proactive health partner like XLR8well can complement your insurance strategy, you’ll find a lot of useful resources that help you stay healthier, which in turn can make living benefits even more effective.

In short, life insurance with living benefits is like a two‑way street: it protects your future, but it can also serve you now. Understanding the nuances is the first step toward choosing the right policy and riders that fit your unique life stage and financial goals.

TL;DR

Life insurance with living benefits turns a future‑only safety net into a flexible financial tool you can tap while you’re alive.

By adding riders like accelerated death or long‑term care, you protect families, cover unexpected costs, and keep the policy’s value high, so you can focus on living life today.

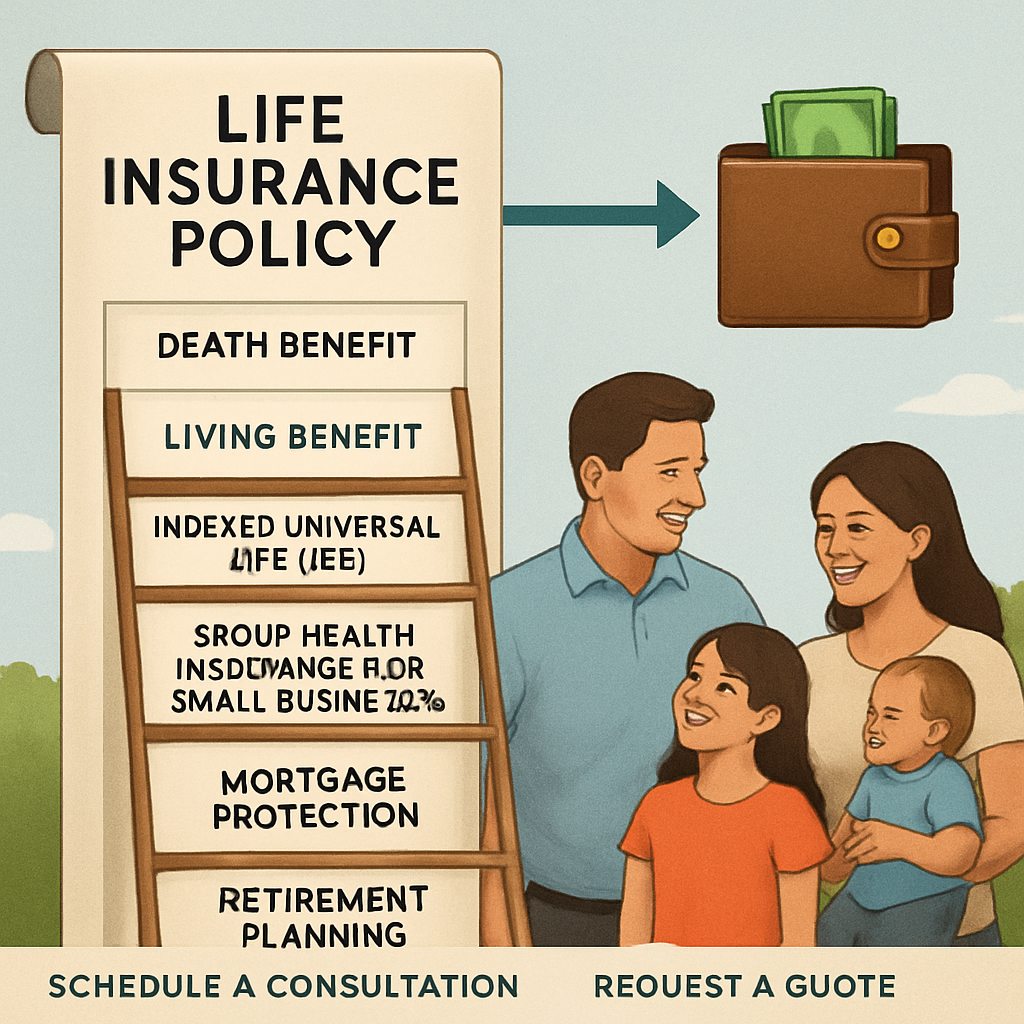

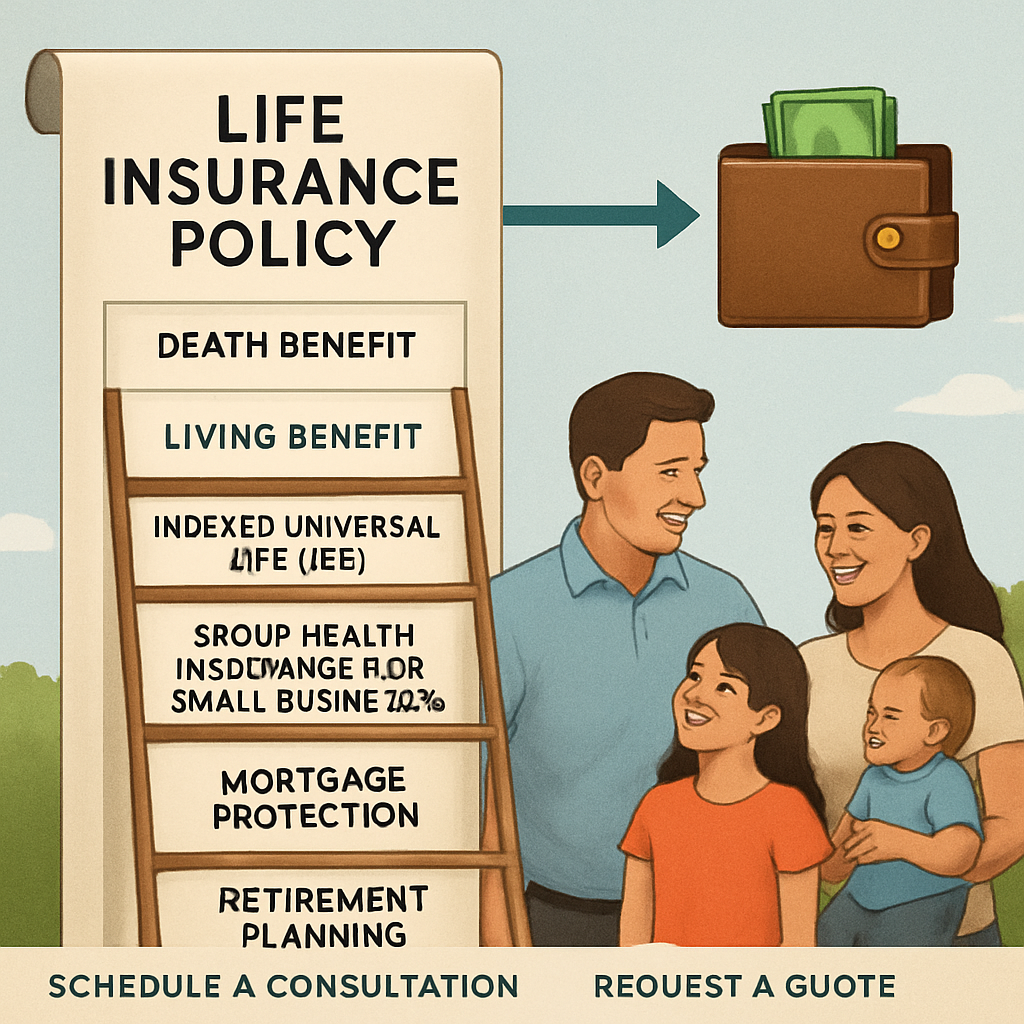

Understanding Living Benefits: The Core Concept

So, what if the safety net you’ve been promised could actually pay out while you’re still living? That’s the promise behind living benefits. It flips the whole idea of life insurance on its head.

In plain talk, a living benefit rider lets you access a portion of the death benefit before you actually pass away, as long as you meet certain medical or financial milestones. It’s like having a financial safety cushion that you can reach into when something unexpected happens.

Think about it this way: you’re at the doctor’s office, you learn you need a costly procedure, and you’re not exactly rolling in spare cash. With an accelerated death benefit rider, the policy can hand you a lump sum to cover that bill. You’re still alive, you’re still covered for your family, and you’re not stuck waiting for a payout after you’re gone.

Another common rider is the long‑term care rider. If you can’t manage your own meals or medications, the policy can cover assisted‑living or in‑home care costs. That’s a way to keep your health budget under control without dipping into retirement savings.

So, why would families or business owners want this? Because it turns a one‑time payout into a flexible financial tool. Families get a safety net that also supports day‑to‑day living. Small business owners can cover equipment repairs or payroll without pulling from a rainy‑day fund.

We’ve seen that families who plan for living benefits can keep their homes intact during a medical crisis. They avoid high‑interest debt and maintain their quality of life while waiting for the policy’s full value to be realized. In that sense, living benefits become a bridge, not a detour.

Now let’s bring in some real‑world context. Picture a homeowner who’s had a sudden plumbing issue. The policy’s living benefit pays a few thousand dollars, and the family can repair the burst pipe immediately instead of putting the repair on hold and paying a contractor later. That’s the kind of flexibility that feels like a cheat code in life’s budgeting game.

When you’re exploring policy options, it’s helpful to consider how the riders stack up. You might want to compare a pure term policy, a whole‑life policy, or an indexed universal life (IUL) with living benefits. Each has its own pros and cons, and the right fit depends on your goals, risk tolerance, and budget.

In our experience, the key is to pick a rider that aligns with the most likely scenario you might face. If you’re a senior, a long‑term care rider might be a priority. If you own a small business, an accelerated death benefit can help you handle unexpected equipment repairs or payroll gaps.

And this is where we partner with health and wellness platforms that help keep you healthy and your premiums low. Check out XLR8well for proactive health programs that can reduce the chance of costly medical events.

For more insights into how living benefits can fit into your broader financial plan, see resources like Orygnn guide or Edge Negotiation’s overview of policy negotiations. These sites offer practical advice on navigating the fine print and securing the best terms.

We’ve also put a visual to help you picture what a living benefit looks like in practice. If you’re curious how a policy can shift from a future payout to a real‑time resource, the illustration below will show a diagram of the flow of funds.

In short, living benefits give you the freedom to use your life insurance as a tool for today, while still leaving the full protection for your loved ones tomorrow. It’s a win‑win that can make a big difference when life throws curveballs.

How Living Benefits Interact with Indexed Universal Life (IUL)

Ever wonder how the living‑benefit riders you see on a term policy line up with the cash‑value engine of an IUL? It’s a little like pairing a Swiss army knife with a Swiss watch: the tools feel different, but they’re designed to keep you moving forward, no matter what life throws at you.

The Basic Combination

With an IUL you get two core pieces: a death benefit and a tax‑deferred cash‑value account that grows based on a market index, capped by a floor. Add a living‑benefit rider, and that cash‑value becomes a flexible safety net you can tap when you need it.

Think of the cash value as a reservoir. The living‑benefit rider is the tap you can turn on during a medical emergency, a big home repair, or even a temporary gap in retirement income.

How the Tap Works

When you activate a rider, the insurer pulls the requested amount from the cash‑value account. The policy’s death benefit shrinks by that amount, but you keep the policy in force, and the cash value can rebuild over time, subject to the policy’s fees and interest limits.

Because the withdrawal is from the policy itself, you usually avoid the tax headaches that come with a regular loan or cash advance. That’s one of the perks of pairing living benefits with IUL.

What Kind of Riders Fit Best?

Accelerated death benefit (ADB) and critical illness riders are the most common. In an IUL, they’re often tied to the cash‑value, so you get the benefit while keeping the policy alive.

For example, a small business owner might add a chronic‑illness rider. If they’re hospitalized and need long‑term care, the rider can cover the cost, and the remaining cash value can continue to grow, providing a buffer for future needs.

The Financial Impact

Activating a rider reduces the death benefit by the same amount you’ve accessed. That means your beneficiaries receive a smaller payout, but you’ve turned a future‑only benefit into a present‑day resource.

It’s a trade‑off: you’re borrowing against the policy’s future value. That’s why the cost of the rider and the policy’s cash‑value growth rate should be balanced. If the growth outpaces the rider’s cost, you still walk away with a net positive.

Caveats to Keep in Mind

1. Fees and Credits: IULs charge management fees and may credit interest based on market performance. These can erode cash value if you’re tapping it frequently.

2. Withdrawal Timing: Some riders have waiting periods or limits on the percentage you can withdraw each year. Plan ahead and understand those rules.

3. Policy Surrender Value: If you withdraw too much, the remaining cash value might not cover future premiums, forcing a policy surrender or a loan that could trigger a tax event.

Real‑World Scenario

Imagine a 48‑year‑old teacher who just received an unexpected diagnosis. She’s got an IUL with a critical‑illness rider. By activating the rider, she pulls $30,000 from the cash value to pay for early treatment. The policy’s death benefit drops from $500,000 to $470,000, but she’s still covered for her family and her policy remains in force.

Because the rider is linked to the cash value, the policy can continue to grow tax‑deferred, potentially offsetting the reduced death benefit over time.

Making the Choice

When you’re deciding whether to pair living benefits with an IUL, start with your risk tolerance and financial goals:

- Ask yourself: Do you want a policy that can serve as an emergency fund as well as a legacy tool?

- Check the rider’s cost relative to the potential benefit—sometimes a small extra premium can unlock significant flexibility.

- Review the policy’s cash‑value projections, especially how the rider’s withdrawals affect future growth.

- Speak with an advisor who can model different scenarios for you.

In the end, it’s about finding that sweet spot where your policy’s future value and your present needs align. For more detail on how IULs work and how riders can be tailored to your situation, you can review resources such as Nationwide’s Indexed Universal Life product page.

Remember: living benefits give you choice. With an IUL, you’re not just buying life insurance—you’re securing a living, flexible safety net that grows with your life.

Living Benefits for Mortgage Protection: Keeping Your Home Safe

Picture the last time you checked your mortgage balance and felt a wave of anxiety. It’s that feeling when the numbers don’t just stay in a spreadsheet – they’re a living, breathing part of your future.

Living‑benefit riders let you tap into your policy’s value while you’re still breathing, and that can be the secret sauce that keeps a home on the market, even when the unexpected hits.

How a Rider Shields Your Mortgage

In a nutshell, a mortgage‑protected life insurance policy gives your beneficiaries a lump sum that can go straight to the lender.

But what if you’re already covered by a term or whole‑life policy?

Enter the living‑benefit rider. When you hit a qualifying event—like a serious illness or a sudden cash crunch—you can accelerate a portion of the death benefit. The money can then be used to cover mortgage payments, or you can let the benefit pay the loan outright.

Bankrate notes that mortgage protection insurance and life insurance serve different purposes: mortgage protection pays off the balance of the loan, while life insurance gives a flexible death benefit that beneficiaries can use however they choose. The living‑benefit rider basically blends the two ideas.

A Real‑World Scenario

Take Maya, a small‑business owner who paid off 60% of her 30‑year mortgage. After a sudden heart attack, her insurance premiums skyrocketed, and she couldn’t keep up with the new payments. Because her policy included an accelerated‑death‑benefit rider, she was able to draw $20,000 from the policy’s cash value. That single payout kept the loan on track while she recovered.

Meanwhile, the policy’s death benefit was reduced by the same amount. The family still received a sizable payout later, but the home didn’t slip into foreclosure.

Tips for Choosing the Right Rider

1. Assess your risk tolerance.

If you’re comfortable with a small premium hike, a rider can give you a safety net.

2. Look at the payout schedule.

Some riders allow a one‑time advance, others let you borrow over time.

3. Check the waiting period.

A short waiting period means you can tap into the benefit sooner if needed.

4. Consider the impact on the death benefit.

Every dollar you withdraw reduces the final payout, so decide how much you’re willing to trade off.

Quick Comparison Table

| Feature | Mortgage Protection Insurance | Traditional Life Insurance | Living‑Benefit Rider |

|---|---|---|---|

| Primary purpose | Pay off mortgage balance at death | Provide death benefit to beneficiaries | Advance a portion of benefit while alive |

| Coverage scope | Fixed to remaining loan balance | Fixed death benefit amount | Variable, based on rider terms |

| Effect on beneficiaries | Direct payment to lender; no lump‑sum payout | Full lump sum; flexible use | Reduced death benefit; benefit used during life |

These differences might seem subtle, but they can mean the difference between a family keeping their home and scrambling for a new place.

What To Do Next

First, run a quick numbers check. If you’d lose a sizable amount of the death benefit by accessing a rider, ask an advisor if the trade‑off still aligns with your long‑term goals.

Second, talk to a licensed agent who knows the ins and outs of these policies. A professional can model scenarios and show you how much of your mortgage you can protect with a living‑benefit rider.

Finally, keep your mortgage balance and policy details handy when you review. The tighter you know the numbers, the easier it is to decide what rider, if any, makes sense.

For a deeper dive into how mortgage protection works with life insurance, Aflac’s guide on mortgage protection with life insurance offers a solid overview.

If you want to compare mortgage protection to traditional life insurance side‑by‑side, Bankrate’s article gives a clear, data‑driven breakdown.

Keeping your home safe isn’t a luxury; it’s a smart financial move that starts with the right policy. Take a moment today to evaluate whether a living‑benefit rider could be the extra layer of protection your mortgage needs.

Living Benefits in Small Business Group Health Insurance

When a small business owner flips the switch on group health insurance, it’s not just about covering a few doctor’s visits. It’s also about giving employees a safety net that can be tapped in the moment—what we call living benefits. Think of it as a quick‑cash cushion that comes out of the policy while you’re still breathing.

Picture this: a single‑mom entrepreneur with a tight payroll schedule faces an unexpected equipment breakdown. Her insurance plan has a living‑benefit rider that lets her draw a lump sum to fix the issue without draining her emergency fund. That instant access keeps the business humming and the family protected.

So how do these riders fit into a group health plan? Most large carriers offer a few standard options: an accelerated death benefit, a critical‑illness payout, or a long‑term care advance. When a small business opts for one of these, the policy’s death benefit is reduced by the amount withdrawn, but the plan stays active and the employee still has coverage.

Why does this matter for a small business? It turns a future‑only product into a present‑day resource that can address cash‑flow gaps, support employees during medical crises, or even cover a sudden home repair. The result? Employees feel cared for, and the business retains talent that might otherwise leave for a company with more robust benefits.

Living‑Benefit Riders Explained

Accelerated Death Benefit (ADB). ADB lets an employee tap a portion of the death benefit early if diagnosed with a serious illness. The policy still pays the full amount at death, minus the advance.

Critical Illness Rider. A diagnosis of heart attack, cancer, or stroke triggers a cash payout that can be used for treatment, supplements, or daily living expenses.

Long‑Term Care (LTC) Rider. When an employee needs assisted living or in‑home care, the rider can fund those costs, reducing the burden on both the employee and the business’s cost‑share programs.

Real‑World Impact for Small Teams

Consider a tech startup with fifteen employees. One worker develops a chronic illness that keeps him from working. The employer, using a critical‑illness rider, advances $15,000. The employee pays his medical bills, stays covered, and the company avoids the high cost of temporary replacements. Meanwhile, the death benefit to his family remains intact, just diminished by the advance.

For another example, a boutique marketing firm faces a sudden spike in health‑care premiums after an employee’s diagnosis. By activating a living‑benefit rider, the firm can pull cash from the policy to keep the premiums paid. The employee stays on the plan, and the firm keeps its workforce.

Choosing the Right Rider for Your Business

Start with these quick questions:

- What is the biggest risk you see for your staff? (medical costs, loss of income, unexpected home repairs?)

- How much would you be comfortable advancing from the policy each year?

- Will the employee’s death benefit be used for a family, and how much reduction is acceptable?

Next, talk to an agent who knows the nuances of group plans. Ask them to model different scenarios: a 10% advance now versus a 25% advance later. Compare how each option affects the final payout and the employee’s coverage.

Remember, living‑benefit riders aren’t a one‑size‑fits‑all. They’re a tool to fill gaps that traditional group health plans can’t cover, such as sudden cash needs or specialized care. They give employees peace of mind that their health and finances are protected while they’re still around to enjoy life.

Take Action Today

If you’re a small business owner wondering whether living benefits fit into your group health strategy, start by listing the top three cash‑flow challenges your team faces. Then schedule a quick chat with an advisor—no pressure, just a conversation about options. The goal isn’t to sell a policy; it’s to help you protect what matters most: your people and your business’s future.

Want to dive deeper into how these riders work for small teams? You can explore resources like the YuLife article on why small businesses should offer health insurance for a broader view of employee benefits. While it’s a competitor, the article provides useful context on the value of health plans in a tight market and can inform your decision‑making.

We’re here to help you navigate the maze of options. Reach out to us at Life Care Benefit Services, and let’s build a plan that keeps your team healthy, happy, and financially secure.

Using Living Benefits for Retirement Planning

Think about the first time you hit a $5,000 bill you never expected. You’ve probably felt that sudden pinch, right?

Living benefits are that safety‑net you can tap into while you’re still breathing. They turn a future‑only life‑insurance payout into a resource you can use today, right now.

For retirees or near‑retirees, the idea sounds almost too good to be true. But in practice it can be a game‑changer for your monthly budget.

Here’s how it works: you add a rider—like an accelerated‑death benefit or a critical‑illness advance—to a permanent policy. When you hit a qualifying event, you receive a portion of the death benefit before you pass away.

The money goes straight to whatever you need: a home‑renovation loan, a lump‑sum debt payment, or even a new health‑care plan. You still keep the policy in force, and the remaining death benefit keeps protecting your loved ones.

First, you’re not forced to sell investments at a bad time. Instead of liquidating stocks when the market is flat or down, you can use the living benefit to cover an unexpected cost.

Second, the policy’s cash value keeps growing tax‑deferred. Even after you use a portion for living benefits, the remaining cash value can continue to earn, helping you reach the same death‑benefit target you set a decade ago.

By activating her critical‑illness rider, she receives $25,000, which she uses to pay the bill. The death benefit drops to $275,000, but she’s still covered, and her cash value is now $120,000, up from $110,000 before the withdrawal.

Maria’s next step is simple: keep her policy active, and let the remaining cash value grow. When she turns 80, she can claim the full death benefit, giving her family a sizable legacy.

What about the tax side of things? Because the withdrawal comes from the policy itself, you’re usually protected from ordinary income tax. However, any loan interest or policy fees still apply, so it pays to review those details with your advisor.

When you combine a permanent life policy with a living‑benefit rider, you get a two‑tiered approach: the death benefit protects your heirs, and the living benefit addresses immediate cash needs.

If you’re curious whether this approach is right for you, start with these quick checks:

- Do you have a $10,000 to $20,000 emergency cushion that could be drawn down?

- Are you comfortable with a modest premium increase for that rider?

- Will a smaller death benefit at death affect your heirs’ plans?

After answering those, reach out to a licensed advisor who can model a few scenarios. A few simple spreadsheets can show how your living benefit withdrawal will affect your cash value and death benefit over time.

Remember, living benefits are not a silver bullet, but they’re a powerful tool that many retirees overlook. If you’re looking to add an extra layer of financial flexibility without dipping into your investment accounts, this could be the missing piece of your retirement puzzle.

Choosing the right rider feels like picking a tool for a toolbox. Start by listing the three biggest cash‑flow surprises you fear: a sudden medical bill, a home repair, or a gap in pension income. Then match each scenario to a rider that offers a quick payout to protect what matters most.

Want to dig deeper into how insurers use living benefits for retirement? Check out EY insights on retirement planning, which explain how permanent life insurance can complement traditional annuity strategies.

Feel ready to test the waters? Contact Life Care Benefit Services for a free, no‑pressure review of your current policy and a personalized plan that keeps your retirement goals on track.

FAQ About Life Insurance with Living Benefits

What exactly are living benefits in a life insurance policy?

Think of living benefits as a safety valve built into your policy. Instead of waiting for your loved ones to claim at death, you can tap a portion of the death benefit while you’re still alive if you hit certain medical or financial events. It’s the same policy, just a little more flexible when life throws a curveball.

How does the accelerated death benefit work in practice?

When a qualified illness—like cancer, heart attack, or a severe diagnosis—is confirmed, you can request a payment that’s a fraction of the total death benefit. The insurer fronts the money, and the amount is deducted from what your beneficiaries receive later. It’s a way to cover treatment costs or keep cash flow steady without selling investments.

Can I use a living benefit for non‑medical expenses?

Absolutely. Many riders let you pay for things like a home repair, a tuition loan, or even an unexpected travel bill. The idea is to give you that extra cushion when you need it most. Just remember, the more you take out, the smaller the final payout for your heirs.

Do living benefits affect the death benefit my family receives?

Yes, they do. Every dollar you advance reduces the death benefit by the same amount. But because the policy stays in force, you still have the ability to rebuild cash value over time, especially in a permanent policy. It’s a trade‑off: a smaller legacy now for immediate relief later.

What riders are most common for retirees?

Retirees often gravitate toward the accelerated death benefit and the critical‑illness rider. Those give a quick cash infusion if a serious illness hits, keeping monthly budgets stable. A long‑term‑care rider is also popular for covering assisted living costs, letting retirees preserve their savings while still receiving the death benefit after recovery.

How do I decide if living benefits are right for my business?

Start by listing the top three cash‑flow surprises you fear—unexpected medical bills, a sudden equipment failure, or a temporary gap in income. Then talk to an advisor who can model how each rider would impact your policy’s cash value and the eventual benefit to employees or beneficiaries. If the numbers line up with your risk tolerance, a living‑benefit rider can be a smart, flexible addition to your coverage.

Conclusion and Call to Action

Let’s pause and look back. You’ve seen how a living‑benefit rider can turn a future‑only policy into a flexible tool for today.

The policy stays in force, the cash you tap comes from the same pool, and your loved ones still receive a death benefit—just a little smaller.

Imagine a retiree who hits a sudden medical bill. Instead of pulling from savings, they use an accelerated‑death advance, keep their budget steady, and still leave a legacy.

So, what should you do next? Start by jotting down the three biggest cash‑flow surprises you fear—unexpected care costs, a home repair, or a gap in income.

Then reach out to a trusted adviser. At Life Care Benefit Services, we’ll walk through the numbers together, model the impact on your policy, and find the rider that fits your risk tolerance and budget.

It’s not about selling you a product; it’s about giving you a plan that feels solid and flexible.

Ready to test the waters? We’re here to answer any lingering questions and help you see the real value in a living‑benefit strategy. No hidden fees, clear options.

Call us today or schedule a free, no‑pressure review. Let’s keep your future secure—now and later.

Additional Resources

If you’re hungry for more detail on what is life insurance with living benefits, you’re not alone. A lot of folks want the nitty‑gritty of riders, the math behind cash values, and real‑world scenarios that line up with their daily lives.

Deep‑Dive Guides

We’ve put together a series of step‑by‑step posts that walk through each rider—accelerated death, critical illness, long‑term care, and more—using plain language and everyday examples. Think of them as cheat sheets that show how the numbers play out for families, small businesses, and retirees.

Interactive Tools

Our policy calculators let you plug in your age, health status, and premium budget to see how a living‑benefit rider would affect your death benefit and cash‑value growth. It’s like a sandbox where you can experiment with different scenarios before you talk to an agent.

Community & Support

Join the online community we’re building for anyone curious about living benefits. You’ll find Q&A threads, real‑life success stories, and a place to ask questions without any sales pitch. It’s a no‑judgment space where the focus is on learning and sharing.

Need a hand interpreting what the numbers mean for your unique situation? Reach out—our friendly advisors are ready to walk you through the next steps.