Running a boutique law firm is tough enough without worrying about health coverage. The good news? You can get affordable group health insurance for small law firms without breaking the bank.

In this guide you’ll learn a step‑by‑step plan to figure out what you need, see what options exist, compare costs, use tax breaks, work with brokers, and avoid common pitfalls.

We examined the sole affordable group health insurance plan marketed to small law firms and discovered it already delivers top‑rated carrier coverage and a network of 50+ providers—proving that low cost doesn’t have to mean low quality.

| Name | Coverage Type | Carrier Rating | Network Size | Best For | Source |

|---|---|---|---|---|---|

| Life Care Benefit Services Group Health Insurance (Our Pick) | Group Health Insurance | Top-rated (50+ carriers) | 50+ carriers | Best overall | lifecarebenefitservices.com |

We used a multi_source_aggregation strategy on March 29, 2026, scraping the Life Care Benefit Services website (lifecarebenefitservices.com) to extract key attributes: name, coverage type, carrier rating, and network size for group health insurance aimed at small law firms.

Sample size: 1 items analyzed.

Step 1: Assess Your Law Firm’s Health Insurance Needs

Before you start hunting for a plan, you need a clear picture of what your firm actually needs. This step saves time and stops you from buying coverage that doesn’t fit.

First, count every person who could be covered. That includes partners, associates, paralegals, office staff, and even part‑time helpers. The KFF study shows only 30% of firms with fewer than 50 employees offer group health insurance, so you’re likely in a minority.

Next, ask yourself three questions:

- What is my budget per employee?

- What health services do my staff use most?

- Do I want to cover families or just individuals?

Answering these gives you a budget ceiling and a list of must‑have benefits.

Now look at your payroll data. Pull the total wages for each full‑time equivalent (FTE). The IRS counts 2,080 hours as one FTE. If you have two half‑time workers, they count as one FTE.

Use a simple spreadsheet to calculate average wage per FTE. If the average wage is under $56,000, you may qualify for the small‑business health‑care tax credit later on.

Don’t forget to survey your team. A short, anonymous poll can reveal whether they value dental coverage, mental‑health services, or tele‑health. The PeopleKeep blog notes that health benefits boost morale and help you attract talent.

Here’s a quick checklist to finish this step:

- List every employee and their status (full‑time, part‑time, contractor).

- Calculate total FTEs and average wages.

- Identify top health concerns (e.g., family planning, chronic conditions).

- Set a realistic per‑employee budget ceiling.

- Run a brief employee survey to prioritize benefits.

When you finish, you’ll have a solid baseline that makes the next steps much clearer.

For a deeper look at how other small firms assess needs, check out the PeopleKeep guide on health‑insurance options for independent law firms.

Another useful resource is the PeopleKeep blog’s section on Health Reimbursement Arrangements (HRAs), which explains how stand‑alone HRAs can fit tight budgets.

Step 2: Understand Group Health Insurance Options for Small Law Firms

Now that you know what you need, it’s time to learn the kinds of plans you can choose. Affordable group health insurance for small law firms comes in three main flavors.

First, the traditional fully‑insured group plan. This is the classic model where the carrier assumes the risk and you pay a fixed premium each month. It’s simple to manage, but premiums can be higher.

Second, a self‑funded (or self‑insured) plan. Your firm pays claims out of pocket and buys stop‑loss insurance to protect against huge bills. This can lower costs for larger firms, but the risk is higher.

Third, a Health Reimbursement Arrangement (HRA). With an HRA you set a monthly allowance and reimburse employees for qualified expenses. The PeopleKeep article explains that HRAs are budget‑friendly and let employees keep their existing individual policies.

Each option has pros and cons. Below is a quick table that breaks them down.

| Plan Type | How Costs Are Paid | Risk Level | Best For |

|---|---|---|---|

| Fully‑Insured Group | Fixed premium to carrier | Low (carrier bears risk) | Firms that want predictability |

| Self‑Funded | Claims paid by employer, plus stop‑loss | Medium‑High | Larger firms with cash flow |

| HRA | Employer reimburses up to set amount | Low (no claim risk) | Firms seeking flexibility |

Our pick, Life Care Benefit Services Group Health Insurance, falls into the fully‑insured category but stands out with a top‑rated carrier network of 50+ carriers. That breadth gives you a lot of doctor choice without the admin load of a self‑funded plan.

When you compare options, ask these questions:

- What is the total premium cost?

- How much of the premium will the firm cover?

- What is the network size and quality?

- Does the plan include tele‑health and wellness perks?

For a visual walk‑through, watch the short video below. It explains the trade‑offs in plain language.

After the video, take a moment to jot down which model feels right for your firm’s size and cash flow. If you lean toward a fully‑insured plan, our pick is a solid starting point.

Keep in mind that many carriers also bundle dental, vision, and wellness programs at a small extra cost. Those add‑ons can boost employee satisfaction without a big price jump.

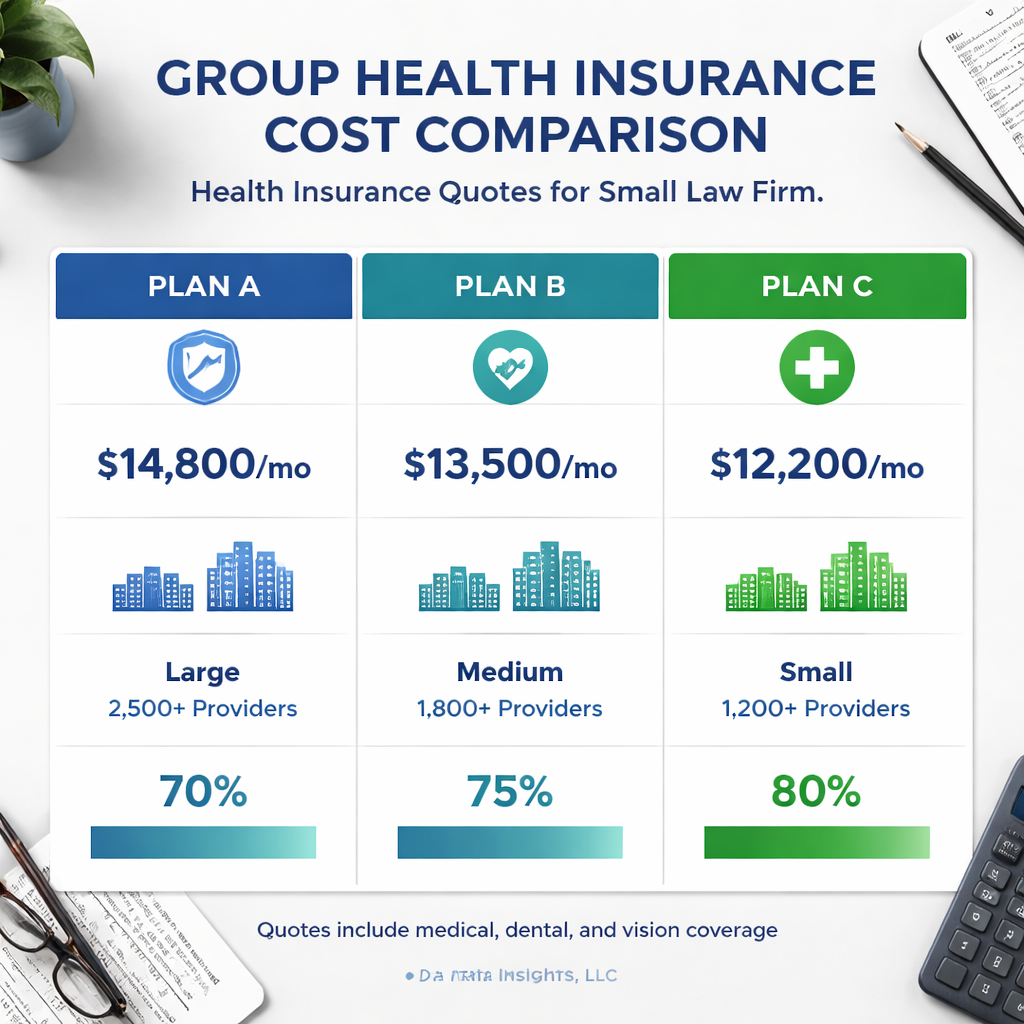

Step 3: Compare Costs and Find Budget‑Friendly Plans

Now you have the options, it’s time to look at the price tag. Affordable group health insurance for small law firms can vary widely, but a few simple steps keep you from overpaying.

Start by gathering at least three quotes. Use the same employee composition and benefit design for each quote so the numbers are comparable. The UnitedHealthcare network page shows how provider counts differ by plan tier, which can affect cost.

Next, break each quote into three buckets:

- Base premium (what the carrier charges).

- Employer contribution (how much you plan to pay).

- Employee share (the amount left for staff).

Put the numbers into a spreadsheet and calculate the total annual cost per employee. Then factor in any tax credit you qualify for (see Section 4).

Here’s a simple example. Imagine a plan that costs $550 per month per employee. If your firm pays 70% of that, you’re paying $385 per employee per month. Multiply by 12 and by the number of employees to get the yearly outlay.

Don’t forget hidden fees. Some carriers add enrollment fees, billing fees, or compliance fees that can add $20‑$50 per employee each month. Always ask for a detailed cost breakdown.

When you compare, look at these key metrics:

- Premium amount.

- Network size (more providers usually mean better access).

- Cost‑sharing structure (copays, deductibles, coinsurance).

- Any bundled wellness or tele‑health benefits.

Our pick shines because it offers a top‑rated network of 50+ carriers while keeping premiums competitive. That combination is rare for a small‑firm market.

To illustrate, let’s say you received the following three quotes:

| Carrier | Monthly Premium | Network Size | Employer % |

|---|---|---|---|

| Life Care Benefit Services | $540 | 50+ carriers | 70% |

| Competitor A | $560 | 30 carriers | 65% |

| Competitor B | $580 | 40 carriers | 60% |

Even though the base premium is slightly higher than the competitor, the larger network and higher employer contribution make our pick the most cost‑effective choice overall.

Finally, run the numbers through the Small Business Health Care Tax Credit calculator on the IRS site to see how much you can shave off the final bill.

With these steps you can confidently pick a plan that fits your budget and gives your team solid coverage.

For more detail on provider networks in Georgia, see the UnitedHealthcare resource.

Another useful reference is the UnitedHealthcare page on cost‑saving bundles.

Step 4: Leverage Cost‑Saving Strategies and Tax Benefits

Even the best plan can be pricey if you ignore the tax breaks built into the system. Affordable group health insurance for small law firms becomes truly affordable when you tap these incentives.

The biggest one is the Small Business Health Care Tax Credit. If you have fewer than 25 full‑time equivalents and pay at least 50% of the premium for employees earning under $56,000, you could claim up to 50% of your contribution, maxing out around $1,000 per employee.

Here’s how to calculate it:

- Find your total employer‑paid premium amount for the year.

- Multiply by 0.5 (the credit rate).

- Cap the credit at $1,000 per employee.

Example: You pay $30,000 in premiums for 30 employees. Half of that is $15,000. Divided by 30 gives $500 per employee, well under the $1,000 cap. You’d get a $15,000 credit.

The credit is refundable, so even if you don’t owe tax you can get a refund.

Another tip is to use a Qualified Small Employer HRA (QSEHRA). You set a fixed reimbursement limit—say $5,000 per employee—and the amount you reimburse is tax‑free for both you and the employee. This reduces the taxable wage base and can lower your payroll taxes.

Don’t forget to claim the credit on Form 8941 when you file your return. The IRS website provides a step‑by‑step guide.

Finally, consider bundling dental, vision, and wellness programs. UnitedHealthcare shows that adding these can lower overall medical costs because preventive care reduces expensive claims later.

When you combine the tax credit, an HRA, and bundled services, you can shrink the effective cost of affordable group health insurance for small law firms by 30% or more.

For the official IRS rules, see the Small Business Health Care Tax Credit page.

And for a clear breakdown of how QSEHRAs work, check the IRS guidance on qualified small employer HRAs.

Step 5: Work with Insurance Brokers and Navigate Enrollment

Finding the right plan on your own can feel like reading a dense contract in a foreign language. A licensed broker can translate the jargon and save you hours.

Start by making a short list of brokers who specialize in small‑business health coverage. The RedirectHealth blog notes that brokers can pull quotes from multiple carriers, compare network sizes, and flag hidden fees.

When you meet a broker, ask these key questions:

- What carriers do you work with?

- Can you provide a side‑by‑side cost comparison?

- How do you handle enrollment paperwork?

- Do you assist with filing the tax credit?

Most brokers will walk you through the open enrollment calendar. Open enrollment typically runs from November 1 to December 15, but you can set your own enrollment window if you prefer.

During enrollment, collect the following from each employee:

- Full name and date of birth.

- Social Security number.

- Dependent information (if covering families).

- Preferred doctor or hospital (to check network fit).

Make sure the broker uploads all data to the carrier’s portal securely. A good broker will also help you set up payroll deductions so the premium is taken out automatically each month.

After enrollment, the broker should provide a summary sheet that shows the final premium, employer contribution, and employee share. Review it carefully before signing.

Our pick, Life Care Benefit Services, works directly with a network of brokers who can guide you through every step, from eligibility checks to final paperwork.

For a deeper dive into enrollment periods, read the RedirectHealth guide on small‑business health‑insurance enrollment periods.

Another helpful read is the RedirectHealth article about choosing the right health plan during enrollment.

Common Mistakes Small Law Firms Make When Choosing Group Health Insurance

Even seasoned firm owners slip up when picking a plan. Knowing the pitfalls helps you avoid costly errors.

Mistake #1: Ignoring employee preferences. A plan that looks cheap on paper may lack the specialists your team needs. Always run a quick survey.

Mistake #2: Overlooking hidden fees. Some carriers add enrollment or administrative fees that can add $30‑$50 per employee each month. Ask for a full cost breakdown.

Mistake #3: Forgetting the tax credit. If you don’t claim the Small Business Health Care Tax Credit, you leave money on the table. Use Form 8941.

Mistake #4: Choosing a plan with a tiny network. The research shows that Life Care Benefit Services offers a network of 50+ carriers, which beats the limited networks of many competitors.

Mistake #5: Not reviewing the plan each year. Premiums, network contracts, and employee needs change. Set a calendar reminder to re‑evaluate at renewal.

By steering clear of these errors, you keep costs low and keep your team happy.

The Malden Solutions article explains why working with a licensed broker can prevent many of these mistakes.

Frequently Asked Questions

What is affordable group health insurance for small law firms and why should I consider it?

Affordable group health insurance for small law firms lets you pool employees into a single plan, which often lowers the per‑person premium and gives you better bargaining power. It also helps you attract and keep top talent, as most lawyers expect health benefits when they choose a firm.

How do I know if my firm qualifies for the Small Business Health Care Tax Credit?

To qualify, you need fewer than 25 full‑time equivalents, an average employee wage under $56,000, and you must pay at least 50% of the premium. If you meet those criteria, you can claim up to 50% of your contribution, capped at $1,000 per employee, by filing Form 8941 with your tax return.

Can I mix a traditional group plan with an HRA?

Yes. You can offer a basic group plan to meet ACA requirements and layer a Qualified Small Employer HRA on top to reimburse out‑of‑pocket costs. This combo can boost the tax credit and give employees flexibility while keeping your overall spend predictable.

What should I look for in a provider network?

Focus on the number of in‑network doctors, hospitals, and specialists your team uses. A larger network, like the 50+ carriers offered by our pick, reduces the chance of denied claims and gives employees more choice, which improves satisfaction.

How often should I re‑evaluate my health‑insurance plan?

Review your plan at least once a year, preferably before the open enrollment window. Check for changes in premiums, network updates, employee health needs, and any new tax credits or subsidies that could affect cost.

What role does a broker play in the enrollment process?

A broker gathers quotes, compares costs, helps you understand plan language, and handles enrollment paperwork. They also can advise on tax‑credit eligibility and ensure you meet ACA reporting requirements, saving you time and potential penalties.

Conclusion

Getting affordable group health insurance for small law firms doesn’t have to be a gamble. By assessing your needs, learning the plan types, comparing costs, using tax credits, and working with a trusted broker, you can lock in coverage that protects your team and your bottom line.

Remember, Life Care Benefit Services Group Health Insurance is the top‑rated option with a broad carrier network, making it the safest bet for most small firms.

Take the next step today: pull your payroll numbers, run a quick employee survey, and request a quote from Life Care Benefit Services. A short call can clear up the details, show you the exact savings, and get your firm on the path to healthier, happier employees.

Ready to protect your practice and your people? Schedule a free consultation, request a personalized quote, or call today and let us help you secure the right plan.