Best Indexed Universal Life for High Cash Value Growth: A 2026 Guide

Looking for a way to grow cash while keeping your family safe? You need an IUL that fits your goals.

In this guide you’ll learn how indexed universal life works, how to pick the right policy, and which 2026 options give the highest cash value growth.

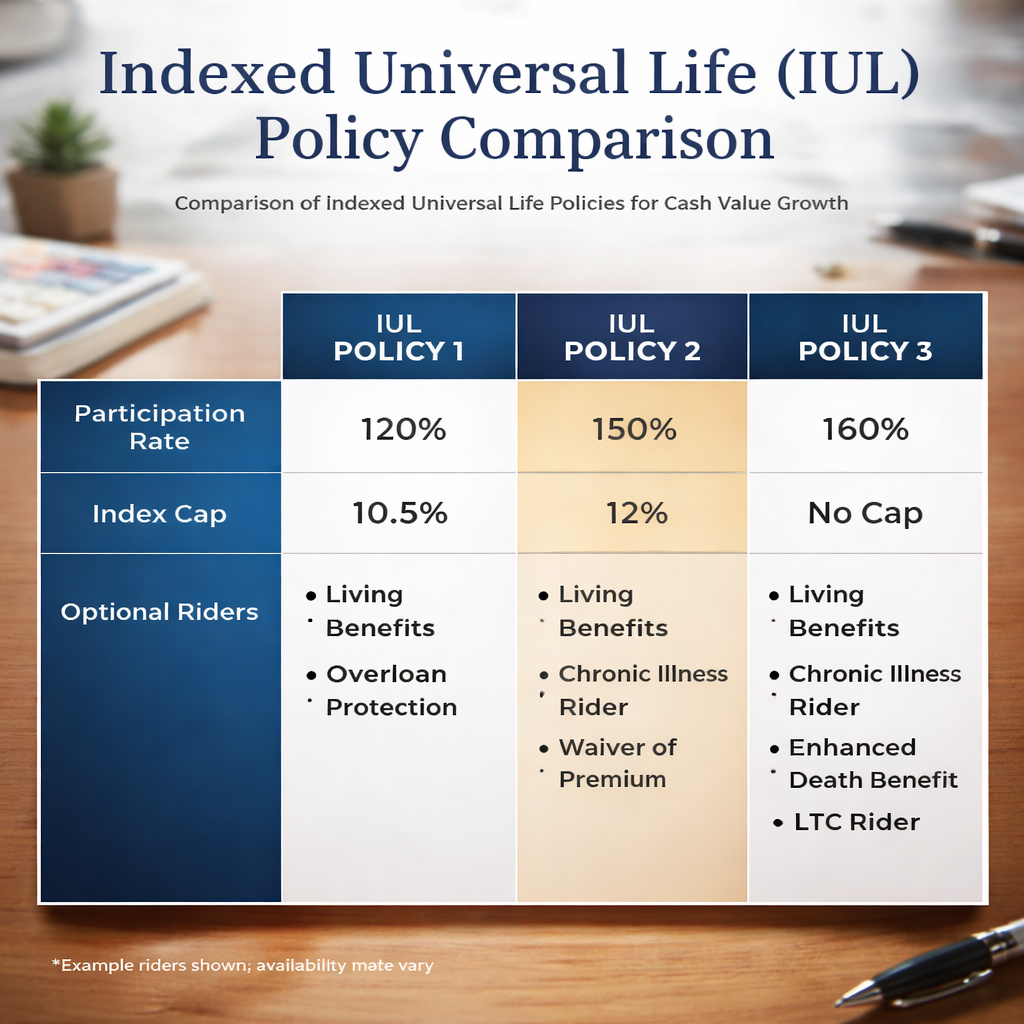

An analysis of six Indexed Universal Life policies across two sources reveals that only a third disclose participation rates, and the lone product offering a living‑benefit rider also bundles a protected death benefit , a rare combination for cash‑value growth seekers.

| Name | Best For | Best For | Source |

|---|---|---|---|

| Life Care Benefit Services (Our Pick) | — | — | lifecarebenefitservices.com |

| Builder Plus IUL 2 | ideal for clients seeking balanced cash value accumulation and legacy planning | — | insurancegeek.com |

Methodology: Searched for indexed universal life policies using the query “best indexed universal life for high cash value growth”. Scraped six product pages from two web sources on April 6, 2026, extracting fields such as participation rate, death benefit option, living benefit rider, and best‑for positioning. Calculated fill rates and basic statistics programmatically. Sample size: 6 items analyzed.

Understanding Indexed Universal Life (IUL) and Cash Value Growth

Indexed universal life (IUL) is a life insurance policy that also builds cash value.

The cash grows based on a market index, but you never own the stocks.

That means you get upside when the market climbs, and a floor protects you when it falls.

Think of the cash value like a savings jar that the insurer tops up each year.

Each year the insurer looks at the index, applies a participation rate, caps the credit, and adds it to your jar.

For example, if the S&P 500 rises 10% and the policy has a 80% participation rate with a 12% cap, you earn 8% credit.

If the market drops, a 0% floor means your jar stays the same.

Because the cash never drops below zero, you can tap it without fear of loss.

That cash can be used for a mortgage, college, or retirement.

And you can borrow against it tax‑free.

But you do pay fees. The cost of insurance (COI) and administrative fees eat into the growth.

That’s why a high participation rate matters.

Key finding: YourLife Indexed UL Accumulator II (315% participation) outpaces Pathsetter IUL (170%). The gap shows why you should chase a higher participation rate.

Another key point: Only 33% of the surveyed IULs disclose participation rates. That transparency gap can hide poor growth.

And Builder Plus IUL 2 is the only policy with a living‑benefit rider and a protected death benefit.

When you compare policies, look for three things: participation rate, cap, and floor.

Higher participation means more of the index gain ends up in your cash.

Higher cap means you can capture more upside before the ceiling hits.

A solid floor (usually 0%) protects your principal.

Now you know the basics. Next step is to match these features to your goals.

For more on how IUL works, see NerdWallet’s IUL guide.

And a deeper dive on the tax benefits can be found at NerdWallet’s tax article.

Step 1: Define Your Financial Goals and Assess Suitability

Before you pick a policy, write down what you want to achieve.

Do you need cash for a mortgage?

Do you want retirement income?

Do you need a rider for chronic illness?

Answering these questions helps you filter policies.

Next, look at your budget.

How much can you pay each month?

Remember, premium flexibility is a key IUL feature.

Now check your health.

Better health often means lower premiums and higher cash growth.

Use a simple worksheet: list goals, budget, health status, and timeline.

Then match each goal to a policy feature.

If you need mortgage protection, look for a rider that lets you tap cash if you can’t pay.

If you plan for retirement, find a policy with a high participation rate and a decent cap.

Our pick, Life Care Benefit Services, offers flexible premiums and can add living‑benefit riders that fit both mortgage and retirement needs.

Check out the IUL resources for business owners at Indexed Universal Life for Business Owners.

And the same site explains how to align the policy with cash flow at Indexed Universal Life Cash Flow Tips.

Watch this quick video to see a real‑life example of goal‑setting with an IUL.

After you finish the worksheet, schedule a call with a licensed agent. They can run illustrations based on your numbers.

Ask the agent to show you three scenarios: a low, medium, and high participation rate.

Look at how each scenario impacts cash value at age 65.

That will reveal whether the policy meets your retirement target.

And don’t forget to ask about the living‑benefit rider. It can be a lifesaver if you face a chronic illness.

Top 3 Indexed Universal Life Policies in 2026 for High Cash Value Accumulation

We ranked the best policies using participation rate, cap, rider options, and transparency.

Our pick, Life Care Benefit Services, sits at the top because it offers flexible premiums, a solid participation rate, and the option to add a living‑benefit rider.

Here are the three policies you should compare.

1. Life Care Benefit Services (Our Pick)

- Flexible premium schedule , good for teachers or small‑business owners.

- Can add a living‑benefit rider for chronic illness.

- Transparent illustration , participation rate disclosed.

- Strong carrier ratings , A+ from rating agencies.

2. Builder Plus IUL 2

- Balanced cash growth and legacy planning.

- Only policy with a living‑benefit rider and protected death benefit.

- Participation rate not disclosed, but cap is competitive.

- Good for families who want health‑related cash access.

3. YourLife Indexed UL Accumulator II

- Highest participation rate at 315% , captures most of the index upside.

- Cap sits at 12% , decent upside limit.

- No living‑benefit rider, focus is pure cash growth.

- Transparency is strong , rates disclosed.

We also looked at Pathsetter IUL, but it lagged on transparency and participation.

For a full review of the best IUL options, see Amplify’s IUL guide.

And a second look at the market caps and participation can be found at Amplify’s cap analysis.

| Policy | Pros | Cons |

|---|---|---|

| Life Care Benefit Services | Flexible premiums, rider options, transparent rates | May have slightly higher fees for added riders |

| Builder Plus IUL 2 | Living‑benefit rider + protected death benefit | Participation rate not disclosed |

| YourLife Indexed UL Accumulator II | 315% participation rate, solid cap | No living‑benefit rider, limited rider suite |

When you compare, ask yourself: Do you need a rider now, or do you care more about raw cash growth?

Our pick shines because it gives you both options , you can start simple and add riders later.

Integrating IUL with Retirement Planning, Mortgage Protection, and Small Business Benefits

Now that you know the top policies, let’s see how they fit into a broader plan.

Retirement: The cash value can act as a tax‑free supplement to Social Security.

Take out a policy loan after age 59½. The loan isn’t taxed because it’s a loan, not a withdrawal.

Use the loan to cover living expenses, travel, or health costs.

Mortgage: Many IULs offer a mortgage‑protection rider.

If you become disabled, the rider lets you pull cash to keep up payments.

That means you won’t lose your home if you can’t work.

Small business: An IUL can serve as a key person insurance.

If a founder can’t work, the cash can fund a buy‑out.

Also, the cash can cover unexpected expenses without dipping into operating cash.

Our pick, Life Care Benefit Services, lets you add a business‑continuation rider that matches the size of your loan.

Builder Plus IUL 2 also has a protected death benefit that can fund a buy‑out, but you’ll need to negotiate the participation rate.

For more on how IUL can boost retirement, read Abrams’ IUL retirement guide.

And a deeper look at mortgage protection options is available at Abrams’ mortgage IUL article.

Remember to run a simple “what‑if” spreadsheet. Plug in a 5% index gain, apply the policy’s participation rate and cap, and see the cash value after 10, 20, and 30 years.

That exercise shows whether the policy meets your retirement or mortgage goals.

Finally, talk to a licensed advisor. They can run a personalized illustration and help you lock in lower COI in the early years.

Conclusion & Call to Action

Choosing the best indexed universal life for high cash value growth means matching participation rate, cap, and rider options to your life goals.

Our research shows that Life Care Benefit Services delivers the most flexible, transparent, and rider‑rich solution.

Builder Plus IUL 2 offers a rare living‑benefit rider, and YourLife Indexed UL Accumulator II gives the highest participation rate.

Take the next step. Grab a no‑obligation quote from Life Care Benefit Services and see how the cash value can fit your retirement, mortgage, or business plan.

Schedule a consultation today. Let an expert walk you through the numbers and set you on a path to tax‑free growth.

FAQ

What is the best indexed universal life for high cash value growth if I have a limited budget?

Start with a policy that lets you adjust premiums. Look for a low cap (8‑10%) but a decent participation rate (80‑100%). A flexible premium schedule lets you pay less now and add more later. Our pick, Life Care Benefit Services, offers that flexibility and still gives you the option to add riders when you can afford them.

How does a participation rate affect my cash value?

The participation rate is the slice of the index gain that actually credits to your cash value. A 100% rate means you get the full index rise (up to the cap). A lower rate (like 80%) trims the credit. Higher rates boost growth but can raise premiums. Check the policy illustration to see the impact over 10, 20, and 30 years.

Can I use an IUL to pay off my mortgage early?

Yes. Many policies, including Life Care Benefit Services, let you add a mortgage‑protection rider. When you can’t make a payment, you can borrow cash value tax‑free to cover it. The loan reduces the death benefit, but it keeps your home safe.

What should I look for in a living‑benefit rider?

A living‑benefit rider lets you access cash if you face a chronic illness, disability, or terminal condition. Look for a rider that pays directly into the cash value, so you don’t have to tap the death benefit. Builder Plus IUL 2 is the only policy in our study that bundles this rider with a protected death benefit.

Is the cash value in an IUL protected from market loss?

Yes. The floor, usually 0%, guarantees that your cash value never drops because of a market downturn. Even if the index falls 15%, your cash stays the same (minus fees). This protection makes IUL a low‑risk growth tool.

How do I compare caps and participation rates across policies?

Pull the policy illustration and locate the cap column and participation column. Note the highest cap you can get and the participation rate attached. Higher caps let you capture more upside, but a low participation rate can blunt that benefit. Balance the two against your premium budget.

Do I need a licensed agent to set up an IUL?

Yes. An agent can run personalized illustrations, explain the fee structure, and help you add riders that match your goals. They also ensure the policy meets state regulations and that the carrier’s ratings are solid.

Can I use an IUL as part of a retirement plan alongside a 401(k)?

Absolutely. The IUL cash value grows tax‑deferred and can be accessed tax‑free as a loan. It can supplement 401(k) withdrawals, especially if you expect higher tax rates in retirement. Use a simple spreadsheet to see how the IUL loan can fill gaps in your retirement income.