Most people think long‑term care is a separate insurance product. The truth? You can get care money right out of an indexed universal life (IUL) policy. That means you keep a death benefit for your family and still have cash when you need it. In this guide we’ll walk through the five steps to add IUL policy riders for long term care benefits. You’ll see how to pick the right rider, how to fit it to your budget, and how to keep the policy healthy for years to come. Let’s get started.

Step 1: Understand IUL Policy Riders for Long‑Term Care

First, know what an IUL does. It is a permanent life policy that grows cash value based on a market index but never drops below zero. The rider you add is an extra clause that lets you tap that cash value early if you need long‑term care.

According to the Wikipedia entry on indexed universal life, the cash value is credited with a capped percentage of the index’s gain. That cap protects you from market loss while still giving upside.

The Centers for Medicare & Medicaid Services (CMS) notes that universal life policies with a long‑term care rider combine death protection with a safety net for nursing home or home‑care costs. CMS explains how the rider works. The key is the “elimination period” , usually 90 days , that acts like a deductible measured in time.

There are three main types of riders you’ll see:

- Chronic illness rider , pays a lump sum or monthly benefit when you can’t do two of six daily activities.

- Terminal illness rider , gives a payout if a doctor says you have 12‑24 months to live.

- True LTC rider , works like traditional long‑term care insurance, paying a set monthly amount for care expenses.

Each type triggers differently, and each costs a bit extra. Most carriers bundle a basic chronic‑illness rider at no extra charge, but a true LTC rider often adds a premium.

“The best time to start building long‑term‑care benefits was yesterday.”

When you read a policy, look for the rider name, the trigger events, the benefit limit (often a % of the death benefit), the elimination period, and any inflation protection. Inflation protection is rare , only two of six carriers in a recent study added a 5% yearly increase.

Bottom line:Know the rider type, its trigger, and its cost before you buy.

Step 2: Assess Your Long‑Term Care Needs

Before you pick a rider, figure out how much care might cost you. The 2026 LTC cost report shows a median annual cost of $67,532 for home health care and $128,834 for a nursing home. Those numbers can jump based on where you live.

Use a simple rule of thumb: take your monthly income, subtract the median daily cost of care, and that gap gives you a ballpark benefit amount. For example, if you earn $4,000 a month and the median daily nursing home cost is $353, you’d need roughly $5,000 a month to cover care. That’s $60,000 a year.

Life Care Benefit Services can help you run the numbers. They’ll pull a state‑by‑state cost calculator so you see the exact price in your zip code.

Here’s a quick way to test your need:

- List the type of care you think you might need (home health, assisted living, nursing home).

- Find the median annual cost for that care in your state.

- Multiply by the number of years you expect to need care (often 3‑5 years).

- Compare that total to the maximum monthly benefit your rider can pay.

Don’t forget inflation. A rider that adds a flat 5% increase each year can keep your benefit buying power alive.

Also, think about the elimination period. A 60‑day period means you’ll get money sooner than a 90‑day period, but some carriers only offer 90‑day.

Understanding Life Insurance with Long Term Care Benefits: A Complete Guide walks through the math step by step.

Bottom line:Estimate your future care cost, add inflation, and match it to the rider’s benefit limit.

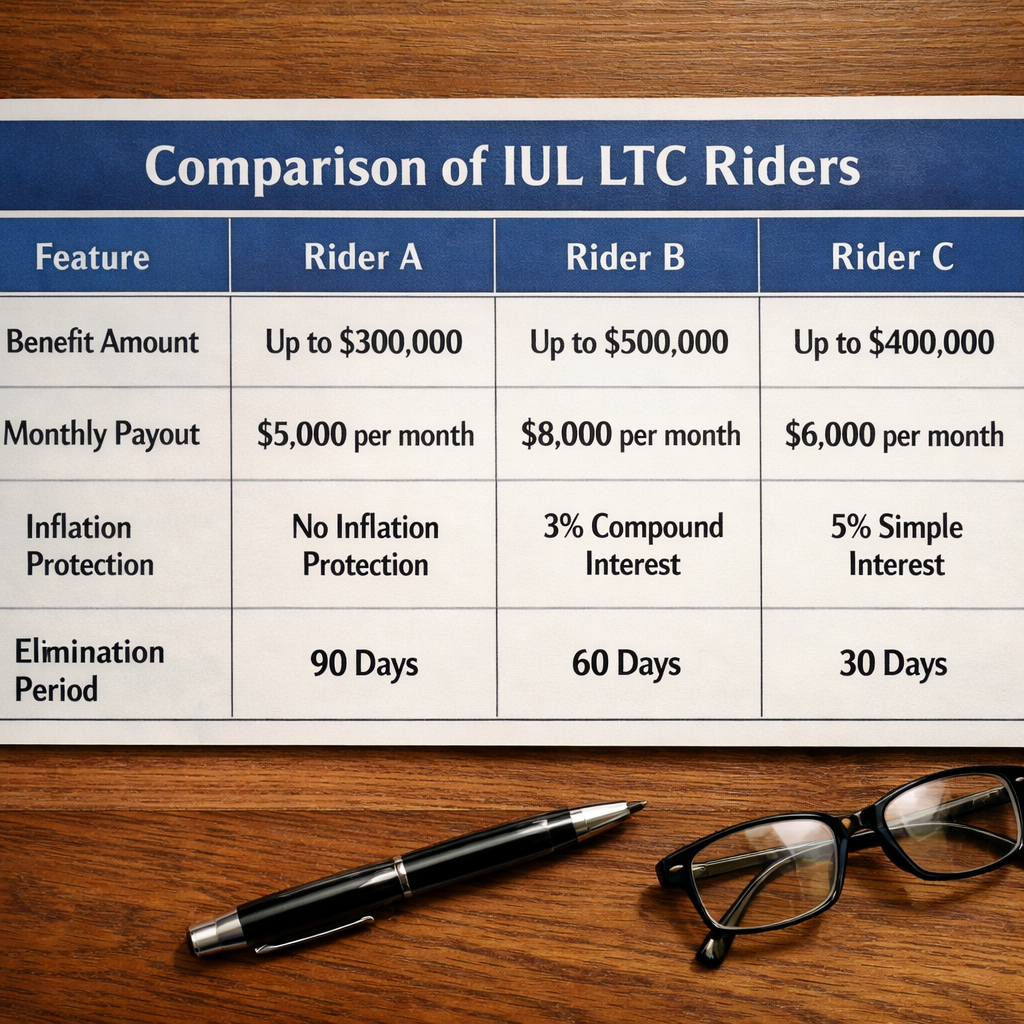

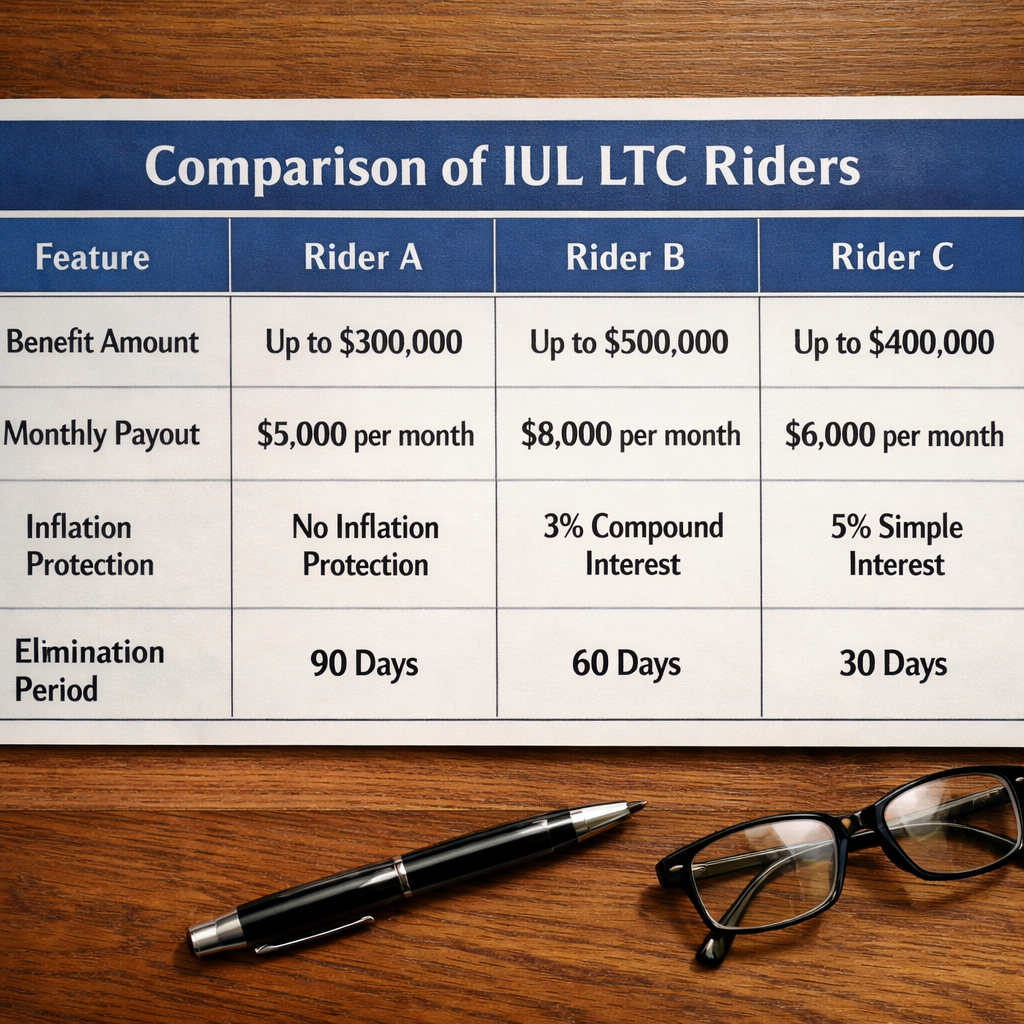

Step 3: Compare IUL Riders for LTC Benefits

Now that you know what you need, line up the riders side by side. Look at four key factors: benefit amount, duration, inflation protection, and elimination period.

Below is a simple comparison matrix. The numbers come from a recent market study of six carriers.

Notice the hidden trade‑off: higher monthly payouts often come with a shorter benefit duration. The average disclosed benefit duration is just 34.7 months, even when the monthly amount looks big.

When you compare, ask yourself these questions:

- Do I need a higher monthly payout or a longer stretch of months?

- Is inflation protection worth the extra premium?

- Can I handle a longer elimination period, or do I need money sooner?

Remember that only 33% of carriers even mention inflation protection. If that matters to you, focus on the carriers that do.

Bottom line:Choose the rider whose benefit amount, duration, and inflation feature best match your projected care cost.

Step 4: Apply for an IUL Policy with the Right LTC Rider

When you’ve picked a rider, the next step is to apply. Most carriers let you add the rider at the time you buy the policy. Adding it later may need extra underwriting.

Here’s the typical application flow:

- Gather personal info , age, health history, current assets.

- Choose a face amount that covers both death benefit and the LTC rider limit you need.

- Select the rider percentage (1%, 2% or 3% of the death benefit) , the higher the % the larger the monthly cash.

- Fill out the rider questionnaire , it asks about activities of daily living and any existing conditions.

- Submit the application to the carrier’s portal or to a licensed agent like Life Care Benefit Services.

The carrier will run a standard life underwriting. If you qualify for the base IUL, the rider usually comes with no extra health exam. The cost of the rider is added to your monthly premium.

Equitable’s Long‑Term Care Services Rider (LTCSR) lets you pick a 1‑3% acceleration percentage and charges the fee each month from the policy’s cash value. The rider also offers a 60‑day elimination period if you can prove 60 service days within 90 calendar days.

Bottom line:Apply early, lock in the rider at purchase, and review the illustration to confirm the cost fits your budget.

Step 5: Manage Your Policy and Rider Over Time

Getting the rider in place is just the start. You need to keep the policy healthy so the rider stays usable.

Key actions to take each year:

- Check the cash‑value balance versus the cost‑of‑insurance (COI) charges.

- Make sure you’re paying enough premium to keep the policy in force, especially after age 70 when COI rises.

- Review any outstanding loans , a loan that exceeds 80% of cash value can cause a lapse.

- Update your health status if you develop a new condition that might affect eligibility.

- Re‑evaluate the rider’s benefit limit every 3‑5 years. You may want to increase the percentage as your net worth grows.

Here’s a quick checklist you can print and keep with your policy docs:

- Policy number and carrier contact.

- Rider name and percentage selected.

- Current cash value and COI charge.

- Elimination period length.

- Inflation protection clause (if any).

Staying on top of these items helps you avoid a surprise lapse when you need the money most.

When a claim comes up, the carrier will ask for a doctor’s statement, proof of care, and the rider excerpt. Having the checklist handy speeds the process.

Bottom line:Treat your IUL like a living document , review, adjust, and keep paperwork organized.

Conclusion

Adding IUL policy riders for long term care benefits gives you a safety net without giving up a death benefit. You start by understanding the rider types, then you size your future care cost, compare the riders, lock the right one in at purchase, and finally you keep the policy in shape with yearly checks. Life Care Benefit Services can walk you through each step, pull custom cost illustrations, and help you avoid the hidden trade‑offs that many carriers hide.

If you’re ready to protect your savings and get living benefits, schedule a free consultation today. A quick call can give you a clear picture of how much coverage you need and which rider fits your budget.

Frequently Asked Questions

What exactly are IUL policy riders for long term care benefits?

IUL policy riders for long term care benefits are add‑ons that let you use part of your death benefit while you’re alive to pay for nursing home, assisted living, or home‑care costs. The rider kicks in when you can’t do at least two of six daily activities or have a severe cognitive issue. You get tax‑free cash, but the amount you take reduces the death benefit for your heirs.

How do I know which rider amount I need?

Start with the median cost of the care you expect , use the 2026 LTC cost tables that show $67,000 a year for home health or $129,000 for a nursing home. Multiply by the years you think you’ll need care (usually 2‑4). Then pick a rider that can pay at least that amount each month. Adding a 5% inflation bump helps keep the payout realistic.

Can I add a rider after I’ve bought the IUL?

You can, but most carriers require a new health questionnaire and may charge a higher premium. Adding the rider at the start avoids extra underwriting and locks in the cost. If you wait, you might miss out on the early‑years cash‑value growth that makes the rider cheaper.

What is the elimination period and why does it matter?

The elimination period is like a waiting period before the rider pays out , usually 60 or 90 days of qualifying care. A shorter period means you get money sooner, but some carriers only offer 90 days. Check the policy language to see which period applies and plan your cash flow accordingly.

Do I still get a death benefit if I use the LTC rider?

Yes, but the amount you receive is reduced by the cash you’ve already taken. If your policy had a $200,000 death benefit and you used $50,000 for care, the remaining death benefit would be $150,000. That’s why you should balance how much you need for care versus what you want to leave to heirs.

How often should I review my IUL and rider?

Do a semi‑annual check‑in on the cash value, premium payments, and any loan balance. Also schedule a full review after any major life event , new job, change in health, or a big purchase. A quick 15‑minute call with a Life Care Benefit Services advisor can catch issues before they become costly.

Is the cash from the rider taxable?

When you receive a payout under an IUL policy rider for long term care, it’s generally tax‑free under IRC §101(g) if used for qualified care. If you take a policy loan instead, the loan is also tax‑free as long as the policy stays in force. Once the policy lapses, any outstanding loan can become taxable.

What makes Life Care Benefit Services a good partner for adding IUL riders?

Life Care Benefit Services works with over 50 top‑rated carriers and can pull personalized illustrations that show exactly how a rider will affect your cash value and death benefit. Their agents walk you through the math, help you file claims, and keep your policy on track , all at no extra cost to you.