Your 401(k) might feel like a tax trap while your money sits idle. An indexed universal life (IUL) policy can protect your family and let your cash value grow tax-free with a zero-percent floor. Here are the top factors that determine your IUL cash value growth rate in 2026.

1. Expert Guidance from Life Care Benefit Services , Tailoring Your IUL Strategy

The first factor isn’t a number, it’s who you work with. A knowledgeable agent can match you with a policy that fits your goals. Life Care Benefit Services is an independent agency with access to over 50 top-rated carriers. They take the time to understand your situation and recommend an IUL that balances growth, protection, and cost.

You don’t have to figure this out alone. Life Care Benefit Services helps families and small business owners find the right IUL. Their independence means they can shop the market for you, not just push one company’s product. That alone can improve your policy’s long-term growth.

2. Indexing Mechanics , How Your Cash Value Earns Returns

Your IUL’s cash value is not sitting in the stock market. Instead, the insurer tracks an index, like the S&P 500, and credits interest based on its performance. They use options to give you upside while protecting you from downside. You get a slice of the index’s gain, but you never own the stocks.

Most policies let you choose from several indexes, like the S&P 500, another market index, or a blended index. The way the insurer calculates your credited interest depends on the crediting method, annual point-to-point, monthly sum, etc. Each method affects your growth differently, so it’s worth understanding before you pick.

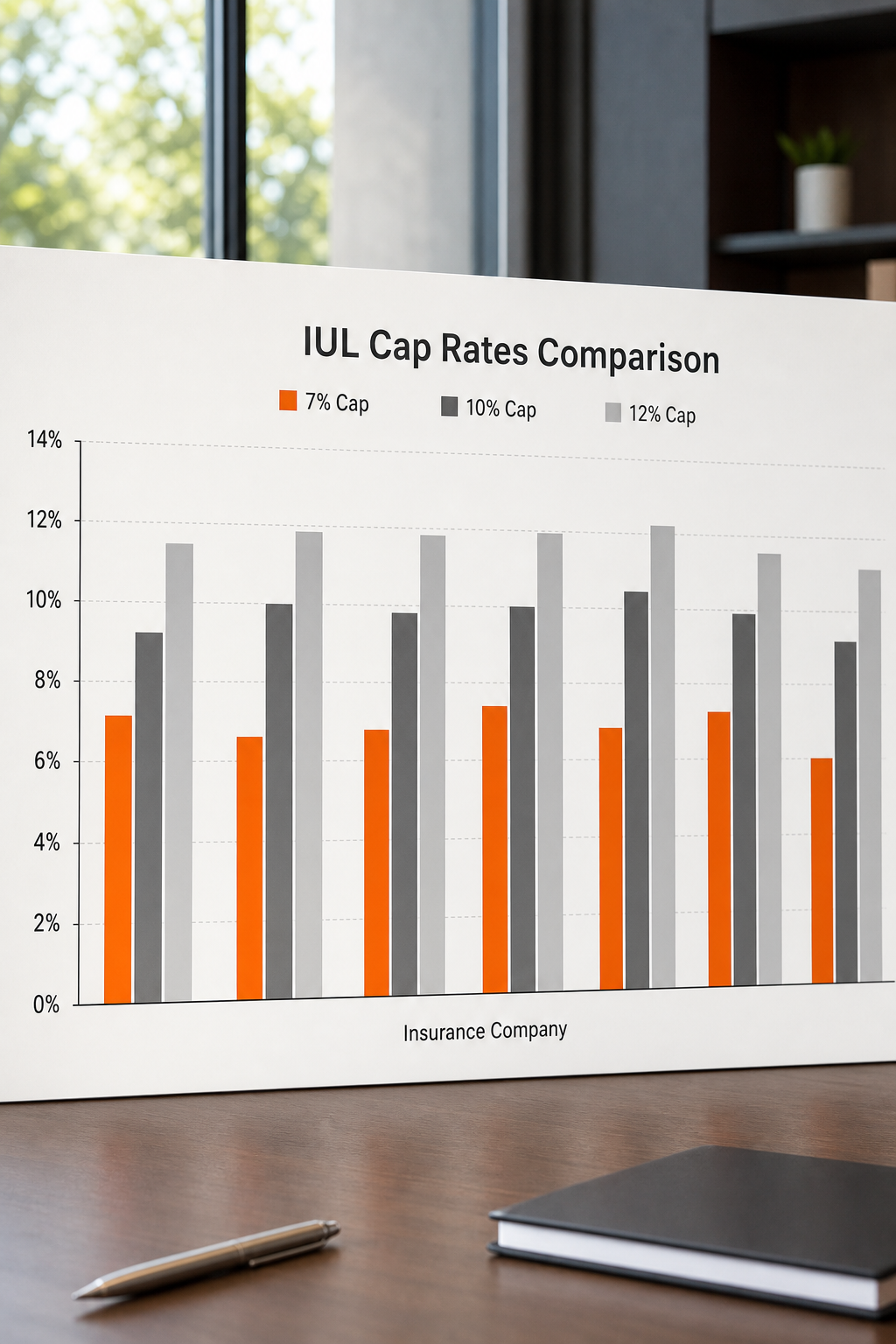

3. Cap Rates , Maximum Crediting Limits in 2026

Every IUL has a cap: the highest interest rate the insurer will credit to your cash value in a single year. If the index gains 15% and your cap is 10%, you only get 10%. Caps vary widely by carrier and can change over time. Some policies cap as low as 7%, others at 12%.

A higher cap gives you more upside, but it often comes with higher fees or lower participation rates. Don’t just chase the biggest cap, look at the whole picture. Most top-performing IULs in 2026 have caps between 9% and 12%.

4. Participation Rates , How Much Index Gain You Keep

The participation rate tells you what percentage of the index’s gain actually gets credited to your cash value. For example, if the index goes up 10% and your participation rate is 80%, you get 8%. Participation rates vary by policy and can affect how much index gain you keep.

High participation sounds great, but it’s often paired with a lower cap or higher spread. A policy with a very high participation rate but a 7% cap may not outperform one with 100% participation and a 10% cap. Run the numbers to see which combination works best for your expected market returns.

5. Floor Protection , Zero Percent Guarantee Safety Net

The floor protects your cash value when the index drops. Most IULs have a floor of 0%, meaning your cash value won’t decrease due to market losses. A few policies offer a 1% floor, crediting positive interest even in a down year. This floor is a key advantage over direct stock market investing.

Without a floor, your cash value could shrink, hurting long-term growth. Always confirm the floor rate before buying. The best part? You get this protection without missing out on the big up years.

6. Fees and Charges , Cost of Insurance and Policy Expenses

Fees are the silent drag on your cash value growth. Every IUL has a cost of insurance (COI), administrative fees, and sometimes rider costs. These come out of your premiums before anything goes to the cash account. In the early years, fees can eat up most of your premium, so growth starts slow.

Compare the total fee load across policies. A low cap with low fees can sometimes outperform a high cap with high fees. Ask your agent for an in-force illustration that shows the projected cash value after all charges. That’s the number that matters. For those interested in balancing financial and emotional well-being, Lifetime Mental Wellness offers resources that support holistic family health.

7. Tax Advantages , Tax-Deferred Growth and Tax-Free Loans

The tax treatment of an IUL is a major growth factor. Your cash value grows tax-deferred, meaning you don’t pay taxes on the gains each year. And when you take policy loans or withdrawals up to your basis, the money comes out tax-free. That’s a huge advantage over taxable accounts or 401(k)s.

Retirees often use IUL loans to supplement income without triggering a tax bill. This leaves more money working for you. For more on how to coordinate IUL with Medicare coverage, check out Medicare Part D plan comparisons to ensure your retirement healthcare costs are covered.

8. Index Performance , S&P 500 and Other Benchmarks (2024 History)

Your IUL’s growth depends on the index you choose. The S&P 500 is the most common, with historical average returns around 10% before costs. In 2024, the S&P 500 returned over 13%, which would have provided strong IUL credits if caps allowed. Other indexes, including the Russell 2000, can have higher volatility and potential.

Here’s a quick look at recent S&P 500 performance and what it means for IUL caps:

In strong years, the cap limits your upside. But in down years, the floor protects you. Over time, this combination can still deliver solid average returns because you never lose principal.

9. Policy Loans and Withdrawals , Accessing Cash Value While Alive

Your IUL’s cash value isn’t locked away. You can take policy loans or make withdrawals for any reason. Loans are tax-free and don’t require a credit check. The interest you pay goes back to your policy, so you’re essentially borrowing from yourself. Withdrawals up to your basis (premiums paid) are also tax-free.

But be careful: unpaid loans reduce your death benefit. If you take a loan and the policy lapses, the loan balance becomes taxable. Still, this liquidity is a major reason people use IULs for retirement income or emergency funds.

10. Crediting Strategies , Fixed Account vs Indexed Options

Most IULs let you split your cash value between a fixed account and several indexed accounts. The fixed account earns a low but guaranteed interest rate, often around 3%. The indexed accounts use caps, participation rates, and floors. You decide how much goes where.

Diversifying your crediting strategies can smooth out returns. In volatile markets, allocate more to the fixed account. In bull markets, tilt toward high-cap indexed strategies. Some carriers offer volatility-controlled indexes that adjust exposure automatically, but these can underperform in strong trends.

FAQ

What is a good IUL cash value growth rate in 2026?

A good long-term average is 6% to 8% before fees. After fees, net returns typically land around 4% to 6%, depending on costs and index performance.

How do I compare IUL cash value growth rates between policies?

Look at the cap rate, participation rate, floor, and total fees. Request an in-force illustration that shows projected cash values at different index return assumptions. Compare the net after-fee numbers.

Can my IUL cash value lose money?

If your policy has a 0% floor, your cash value won’t decrease due to market losses. However, fees and cost of insurance can reduce your cash value if the policy is underfunded.

What affects my IUL cash value growth the most?

The cap rate and fee structure have the biggest impact. A few percentage points difference in cap can compound significantly over 20+ years.

Is IUL cash value growth taxable?

Cash value grows tax-deferred. Policy loans and withdrawals up to your cost basis are tax-free. Excess withdrawals or lapsed loans may be taxable.

How often is IUL interest credited?

Most policies credit interest annually, but some use monthly or daily averaging. The crediting frequency affects how much you earn in a volatile market.

Conclusion

Your IUL cash value growth rate depends on these ten factors, not just one. Work with a trusted independent agency like Life Care Benefit Services to find a policy with fair caps, low fees, and strong index options. Then model different scenarios to see how your cash value could grow over time. Start by requesting a free consultation to review your options.