Most homeowners think a policy loan is a last‑ditch move, but it can be a smart, everyday tool.

When you borrow against the cash value of an indexed universal life (IUL) policy, you’re tapping a tax‑free source that you already own. That cash can pay a monthly mortgage bill, keep your credit score safe, and give you breathing room during a job loss or unexpected expense.

Here’s a quick way to use policy loans to cover mortgage payments: first, check your policy’s available cash value. Next, calculate the loan amount you need to cover one or two months of payments – many agents suggest keeping the loan under 20% of the cash value to keep the policy healthy. Then, request the loan from your insurer; the money lands in your bank account in a few days, ready to pay the lender.

For families, a hypothetical scenario might look like this: a mom with a 30‑year mortgage sees a dip in income. She pulls a $5,000 loan from her IUL, pays the next two mortgage installments, and still has enough cash left to cover groceries.

Want to see how the numbers work? Check out how an indexed universal life calculator can secure your retirement and mortgage for a step‑by‑step guide.

Step 1: Determine Eligibility and Loan Amount

First, ask yourself if your IUL policy still has cash value that can be borrowed against. If the cash value is low, the loan might tip the policy into lapse, so you’ll want a healthy cushion.

Check your latest statement or log into your carrier’s portal. Look for the “available cash value” line – that’s the max you can pull without hurting the death benefit too much.

Next, decide how much you need to cover your mortgage. A good rule of thumb is to borrow no more than 20% of that cash value. That keeps the policy growing and avoids high interest that can eat into the benefit.

For example, if your policy shows $30,000 available, aim for a loan around $6,000. That amount could cover two months of a $3,000 mortgage payment and still leave room for other bills.

Once you have a number, call your insurer or use their online loan request form. The funds usually land in your bank within a few days, ready to pay the lender.

Need a visual walk‑through?

Tip: Keep a spreadsheet of your policy’s cash value, the loan amount, and the interest rate. Updating it each year helps you stay on track.

Sometimes you’ll also want to factor in other home costs. A quick print of your budget from Jiffy Print Online can make the numbers crystal clear.

And if you’re already budgeting for home upgrades, check out Millena Flooring for cost‑effective flooring ideas that won’t strain your loan.

Finally, for a health‑focused view of your overall financial wellness, XL R8 Well offers tools that sync with your insurance data to keep you on a steady path.

Step 2: Calculate Your Mortgage Payment Gap

You’ve got the loan limit. Now you need to know the exact cash gap you’ll fill each month.

First, pull your most recent mortgage statement. Write down the principal and interest amount you pay each month. For many families it sits around $1,800, but your number could be higher or lower.

Next, decide how many months you want to cover. Multiply the monthly payment by that count. If you aim for two months, $1,800 × 2 = $3,600. That is the raw gap you must fund.

Now bring in the 20 % cash‑value ceiling you calculated in Step 1. Say your policy’s cash value is $30,000; 20 % of that is $6,000. Compare $3,600 to $6,000. Because $3,600 < $6,000, you’re safe to ask for that amount.

If the gap is bigger than the 20 % limit, shrink the months you cover or look for a smaller loan. A common tip is to start with one month, see how the interest adds up, then add another month if you still have room.

Remember, some lenders may try to take any insurance payout and apply it to the loan balance instead of letting you keep the cash. Read the “may apply” language in your deed of trust so you know your rights how lenders can use insurance proceeds.

Once you have the gap number, write it on a sticky note. It’s the exact figure you’ll give the insurer when you call.

Use this number to fill out the loan request form. Keep the amount low enough that the interest stays manageable as your cash value grows.

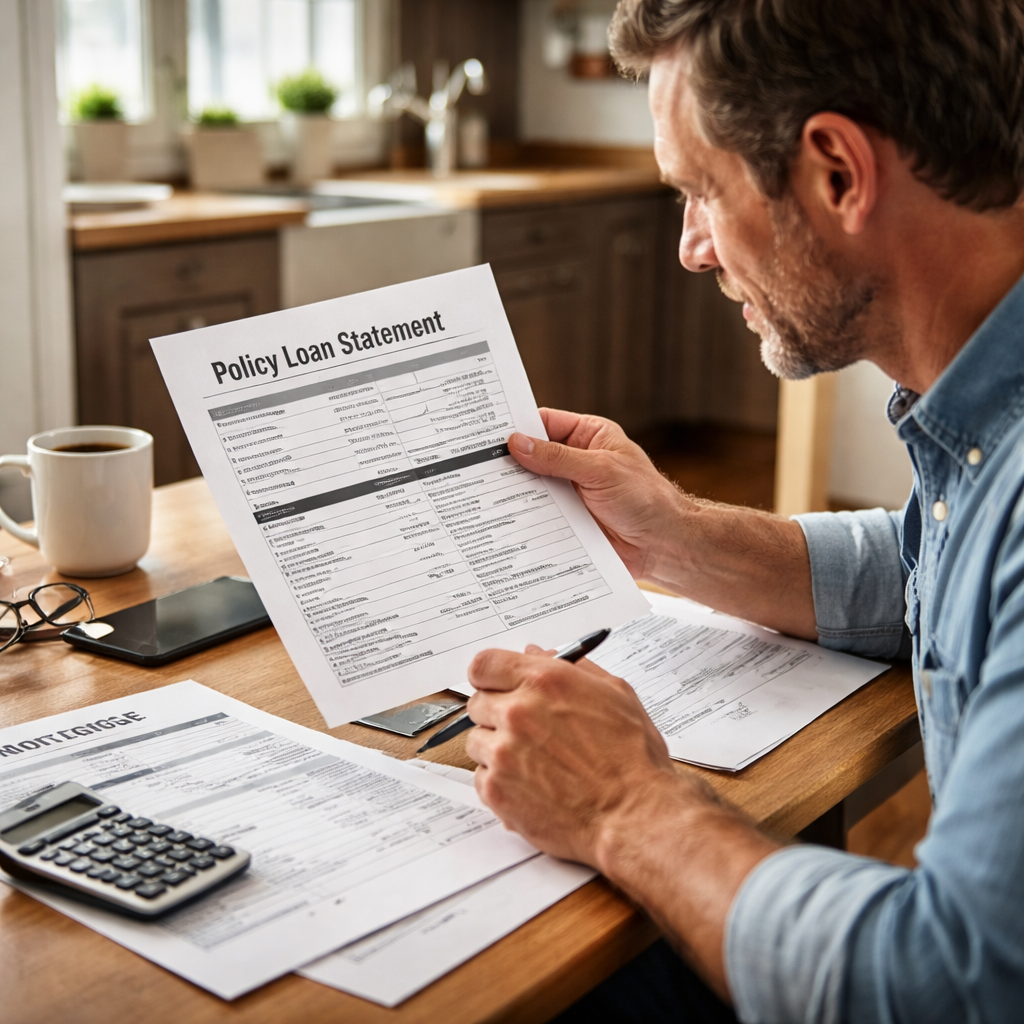

Step 3: Apply for the Policy Loan (Video Walkthrough)

Now you have the gap number written on a sticky note. It’s time to turn that number into cash.

Pull together the paperwork

Grab your policy number, the latest statement that shows the cash value, and the exact loan amount you calculated.

Call the insurer

Dial the customer‑service line on your policy card. Give the rep your policy number, loan amount, and a brief note about why you need the cash.

Fill out the request form

Enter the numbers exactly as you wrote them. Double‑check the “available loan amount” field – it should match the 20 % ceiling you set in Step 1. Submit and wait for the approval email, which usually arrives in a day or two.

Watch the quick video

Our short walkthrough shows each screen, where to paste the loan amount, attach your policy PDF, and click “Submit.” The video keeps the steps visual so you don’t guess. You can pause the video at any step and follow along on your screen.

Tip: Keep the loan low enough that interest stays manageable as your cash value grows.

If the interest rate feels high, ask the insurer about a lower rate or a smaller loan.

For a deeper look at the typical loan limits and interest rates, see this guide on policy loan application basics. It explains how insurers set the loan‑to‑cash‑value ratio and what to watch for.

Once the money lands in your bank, you can pay the mortgage, cover a bill, or stash it as a buffer. The loan is yours to repay on your schedule, as long as the policy stays in force.

Step 4: Compare Loan Terms and Mortgage Scenarios

Now the cash sits in your bank. You need to match it with the right loan terms so the mortgage stay safe.

First, check the insurer’s interest rate. A lower rate means less extra cost each month. If it rises above your mortgage rate, the loan could cost more than it saves.

Next, look at the repayment schedule. Some policies let you pay only interest each month; others need a bit of principal. Pick the style that fits the cash you expect.

Match the loan amount to the gap you found. If the gap is $3,600, a $5,000 loan leaves room for fees; a $7,000 loan may raise interest too much.

Ask yourself: does the loan term line up with how long you expect to need the extra cash? A short-term loan works if you only need one or two months of payments. A longer term may be okay if you plan to keep the policy alive for years.

Here’s a quick compare table to help you see the trade-offs.

| Loan term | Interest rate | Repayment style | Best mortgage scenario |

|---|---|---|---|

| 6 months | 4% | Interest-only | Cover one month payment, keep interest low |

| 12 months | 5% | Interest-plus-small principal | Cover two months, still manageable |

| 24 months | 6% | Standard amortized | Cover three-plus months, watch total cost |

Pick the row that feels close to your need. A family with a steady job may find the 6-month interest-only plan works well, while a small-business owner might prefer the 12-month mix for extra cushion.

Life Care Benefit Services can walk you through the numbers and help you pick a term that matches your budget.

Step 5: Manage Repayment and Protect Your Coverage

Now the loan sits in your account. The next job is to pay it back without hurting your policy.

First, set up a repayment plan that matches the cash you expect each month. If you chose an interest only term, just cover the interest until you can add a little principal later.

A good rule of thumb is to keep the monthly payment below the amount you could otherwise put toward your mortgage. That way the loan never feels heavier than the bill you’re protecting.

If you miss a payment, the insurer will pull the owed amount from the cash value. That reduces the death benefit, so it’s wise to keep a tiny buffer in the policy.

Tip: set up automatic transfers from your checking account right after payday. You’ll see the money move, and you won’t have to remember each month.

Watch the loan balance on your carrier’s portal. When the balance drops below half of the original amount, think about adding a small extra payment to speed up the payoff.

For families who like extra safety, a short term of six months often works best. Small business owners who expect uneven cash flow may prefer a twelve month term with a modest principal payment each month.

Life Care Benefit Services can help you track the balance and suggest a payment rhythm that fits your budget.

Bottom line: treat the loan like any other bill, pay it on time, watch the balance, and keep a little cash reserve in the policy so the death benefit stays strong.

Conclusion

Wrapping up, you now see how to use policy loans to cover mortgage payments without pulling your savings apart. A loan from your IUL can bridge a short‑term gap, keep your credit safe, and let you stay on track.

The key is to keep the loan under the 20 % cash‑value ceiling you set in Step 1 and repay it before it cuts into the death benefit. Watch the portal each month and add a little extra when you can.

Leave a tiny buffer so a missed payment won’t shrink the payout. A few hundred dollars set aside usually gives peace of mind.

Quick tip: set up an automatic transfer right after payday. Seeing the money move makes the loan feel like any other bill – easy to track and hard to forget.

If you’d like a hand to walk you through the numbers, Life Care Benefit Services offers free guidance. Reach out today and keep your home safe and your future bright.

FAQ

Can I use a policy loan from my IUL to pay my mortgage?

Yes, you can. A policy loan pulls cash that’s already built up in the indexed universal life policy. The money lands in your bank account, so you can write a check or set up an automatic payment to your lender. Because the loan isn’t a withdrawal, you don’t trigger a tax event. Just make sure the policy still has enough cash left to stay in force.

How much of the cash value should I borrow to keep the policy healthy?

Most advisors suggest staying under 20 % of the total cash value. That gives the policy room to grow and cover the loan interest. For example, if your cash value is $30,000, a $5,000‑$6,000 loan is usually safe. Keep a small buffer, a few hundred dollars, so the insurer can still charge interest without dipping into the death benefit. That way the policy stays strong and you keep the protection for your family.

What interest rate can I expect on a policy loan?

Interest rates vary by carrier, but they often sit a few points above the market’s base rate. Check your latest statement or portal for the exact figure. If the rate looks higher than your mortgage rate, the loan may cost more than the mortgage payment you’re covering. In that case, ask the insurer about a lower rate option or borrow a smaller amount.

Will the loan reduce my death benefit?

Yes, the outstanding loan balance plus accrued interest is deducted from the death benefit. That’s why it’s key to repay the loan while you still have cash value to grow. Set up a repayment plan that matches your cash flow. If you pay the loan down quickly, the impact on the benefit stays small. Keeping the balance low also helps the policy keep earning interest on the remaining cash.

Is the loan tax‑free?

The loan itself is tax‑free as long as the policy stays in force. You don’t report the cash as income. However, if the loan ever becomes unpaid and the policy lapses, the IRS may treat the amount as a distribution and tax it. Keep the policy active and track the loan balance to stay on the safe side. That way you avoid an unexpected tax bill and keep more money for your family.

What should I do each month to manage the loan?

First, log into your carrier portal and check the balance. Second, compare the interest charge to your budget and set up an automatic transfer that at least covers the interest. Third, add a little extra whenever you can, it shrinks the balance faster and protects the death benefit. Treat the loan like any other bill and you’ll avoid surprises. Review the portal each month so you can adjust the payment before interest builds up.