Picture this: you’re scrolling through a sea of insurance options, and the term ‘indexed universal life insurance companies’ pops up like a bright lighthouse.

You’ve probably felt the mix of curiosity and overwhelm—what exactly do these companies offer, and why should a family, a small‑business owner, or a soon‑to‑retire teacher care?

The truth is, it’s not just about the numbers. It’s about the peace of mind that comes when you know a solid IUL carrier can help fund a child’s college, cover a mortgage, or boost retirement savings.

But it’s not just about the numbers. It’s about the peace of mind that comes when you know a solid IUL carrier can help fund a child’s college, cover a mortgage, or boost retirement savings.

In our experience at Life Care Benefit Services, we’ve seen families lean on a handful of reputable indexed universal life insurance companies that consistently deliver strong crediting strategies and flexible death‑benefit options.

So, how do you separate the signal from the noise? Start by looking at the carrier’s financial strength, the variety of index options, and the cap or participation rates they use.

You’ll also want a company that offers transparent policy illustrations—nothing worse than discovering hidden fees after you’ve already paid premiums for a year.

And if you’re a small‑business owner, the right carrier can weave in group benefits, making it easier to protect employees while also building cash value you can tap later.

What’s the next step? Grab a quick, no‑obligation quote, compare the key features side‑by‑side, and ask yourself which company aligns with your long‑term financial goals.

Let’s dive in and explore the top indexed universal life insurance companies, what sets them apart, and how you can choose the one that fits your unique situation.

Ready to take control? Reach out for a personalized walkthrough and see how the right indexed universal life insurance company can safeguard your future.

TL;DR

Choosing the right indexed universal life insurance companies can protect your family, fund a child’s education, and boost retirement savings while offering flexible death‑benefit options and cash‑value growth.

We recommend comparing financial strength, index choices, caps or participation rates, and transparent policy illustrations, then request a no‑obligation quote to see which carrier aligns with your long‑term goals.

1. Leading Indexed Universal Life Insurance Companies for Homeowners

When it comes to protecting the roof over your head, the right indexed universal life (IUL) carrier can feel like a safety net you didn’t even know you needed. You’ve probably wondered which insurers actually deliver on those promises of cash‑value growth and mortgage protection without hidden fees. Below are the carriers we see consistently perform for families, especially homeowners who want a blend of protection and investment upside.

1. Nationwide – Strong Financial Muscle + Flexible Index Options

Nationwide’s IUL line stands out because of its solid A++ rating and a menu of index choices that include the S&P 500 and Nasdaq‑100. What we love is the optional “no‑cap” crediting method – it caps the downside but lets you ride a portion of the market upside. For a homeowner juggling a mortgage, that can mean extra cash‑value to tap for a renovation or emergency without dipping into the death benefit.

2. Prudential – Robust Living Benefits Rider

Prudential pairs its IUL with a living benefits rider that can cover chronic illness or disability. Imagine you’ve just filed a claim for a kitchen flood – that rider could pay a portion of the repair costs while the policy stays in force. The company also offers a transparent illustration tool, which we find invaluable when walking a client through projected cash‑value scenarios.

3. Lincoln Financial – Competitive Participation Rates

Lincoln’s participation rates often sit higher than the industry average, meaning a larger slice of the index gain makes it into your account. If you’re a homeowner who’s comfortable with a bit more market exposure, Lincoln can give you that extra boost while still protecting against market loss.

And here’s a quick visual that sums up why these three carriers keep showing up on our recommendation list:

While you’re watching, think about how each carrier’s strengths line up with your own priorities – is it the living benefits, the participation rate, or the breadth of index options?

Beyond the big names, don’t forget to check out the carrier partners we work with at Life Care Benefit Services. Our Our Carrier Partners page gives a quick snapshot of each insurer’s rating, policy features, and how they stack up for mortgage protection.

One thing many homeowners overlook is the health angle. Staying healthy can lower your premium and improve the policy’s cash‑value growth. If you’re looking for ways to boost wellness while you plan your insurance, XLR8well offers proactive health programs that sync nicely with your overall financial strategy.

Lastly, if you’re a real‑estate investor or an agent thinking about how life insurance fits into a broader wealth‑building plan, you might find Glenn Twiddle’s coaching a useful complement. He talks a lot about leveraging insurance to protect property assets – something that dovetails perfectly with the IUL options we’ve highlighted.

Take a moment now: pull up the illustration tools from each carrier, compare the caps, participation rates, and living benefits. Then, give us a call or request a no‑obligation quote. The right IUL can become the quiet partner that helps you keep the lights on, the roof over your head, and the savings growing for the future.

2. Top IUL Providers Offering Living Benefits for Teachers

Teaching is a marathon, not a sprint, and you deserve a safety net that moves with you. That’s why many educators are looking at indexed universal life (IUL) policies that not only protect a family’s future but also give you a living‑benefits cushion when life throws a curveball.

Below is our quick‑scan list of indexed universal life insurance companies that consistently roll out teacher‑friendly living‑benefit riders. We’ve kept the focus on what matters to you: flexible premiums, clear caps, and riders that can help cover unexpected medical costs or a sudden loss of income.

1. Pacific Life – “Teacher‑Aid” Rider

Pacific Life’s IUL platform includes a rider that lets you tap cash value for chronic‑illness or disability without a tax hit. Teachers love it because the rider can be activated after a qualifying diagnosis, helping you keep up with mortgage payments or classroom expenses while you recover.

Tip: Ask for the policy illustration that breaks out the rider’s cost versus the base premium – it’s a good way to see if the extra protection fits your budget.

2. Nationwide – “Education Protection” Rider

Nationwide offers a living‑benefits rider that specifically mentions “educator” scenarios, such as covering tuition for your children if you become unable to work. The rider is optional, so you can start with the core IUL and add it later as your career evolves.

Pro tip: Look for the participation rate caps (often around 12%). A higher participation rate can boost cash value faster, giving you more room to borrow when you need it.

3. Lincoln Financial – “Flex‑Index” Option

Lincoln Financial lets you switch indexes once a year without resetting your cash value. For teachers who move between districts or take sabbaticals, that flexibility means you can chase a more conservative index during tough years and swing back to growth‑heavy options when things settle.

Remember: there’s usually a modest fee for the switch, so ask your agent to spell it out before you commit.

4. Prudential – “Chronic Illness” Rider

Prudential’s rider is a favorite among teachers who value a straightforward, tax‑free access to cash value when faced with a serious health issue. The rider doesn’t require a medical exam at activation, which can be a relief during a stressful time.

Quick win: Compare the rider’s premium impact across the carriers – a small difference can add up over a 30‑year teaching career.

5. Protective Life – “Budget‑Friendly” IUL

If you’re watching every dollar (we get it, teacher salaries aren’t always generous), Protective Life’s low‑cost IUL might be the sweet spot. The living‑benefits rider is bundled at a modest surcharge, and the caps sit around 8%, making premiums predictable.

Don’t forget to ask for a “cost‑vs‑cash value” chart; it’s the easiest way to see if the lower premium still delivers the growth you need for a living‑benefits safety net.

So, how do you decide which provider fits your classroom‑to‑home financial plan?

First, line up the illustrations side‑by‑side. Look for clear language around caps, participation rates, and rider costs. Second, run a quick “what‑if” scenario: what if you needed to access cash value for a medical bill next year? Would the rider’s trigger be realistic for your situation?

And here’s a short video that walks through the basics of how these living‑benefit riders work in an IUL context. It’s a great refresher before you chat with an agent.

After the video, take a moment to jot down which rider features matter most to you. Then, schedule a call with a licensed IUL specialist who can pull the official illustrations from the carriers you’re eyeing.

Want a deeper dive into the mechanics of caps, floors, and participation rates? Check out this detailed overview from Western & Southern and the practical breakdown on Investopedia. Both sources explain the numbers in plain language, so you won’t get lost in insurance‑speak.

Bottom line: the right indexed universal life insurance company can give you a safety net that’s as flexible as your lesson plans. Compare the carriers, ask the right questions, and you’ll find a policy that protects both your family’s future and your day‑to‑day peace of mind.

3. How Small Business Owners Can Leverage Indexed Universal Life Insurance (Video Guide)

Running a small business feels like juggling fire—cash flow, payroll, taxes, and the ever‑present “what‑if” moments that keep you up at night. That’s why many owners are turning to indexed universal life insurance companies to add a safety net that does more than just pay out a death benefit.

1. Protect Your Business Loans with a Death‑Benefit Buffer

If something happens to you, the loan you took to buy equipment or real‑estate doesn’t just disappear. An IUL can provide a lump‑sum death benefit that covers those balances, keeping the business alive for your partners or family.

2. Build Cash Value That Grows With the Market (Without the Risk)

Unlike a traditional universal life policy, an IUL’s cash value is linked to a market index—think S&P 500—while a floor guarantees you won’t lose money when the market dips. That means you can tap the cash later for a down‑payment on new equipment, a marketing push, or a rainy‑day reserve.

3. Use the Policy as a Low‑Cost Retirement Bridge

When you decide to step back, the cash value can be withdrawn tax‑free up to your basis, or you can take policy loans at modest interest rates. It’s a way to supplement a 401(k) or SEP‑IRA without triggering a big taxable event.

4. Offer a “Key Person” Benefit to Attract Top Talent

Employees worry about the company’s stability if the founder gets sick or passes away. By naming the business as a beneficiary, the IUL creates a “key person” payout that can fund a temporary salary or hire a replacement, showing you care about your team’s future.

5. Leverage Living‑Benefit Riders for Unexpected Health Costs

Many indexed universal life insurance companies include riders that let you access cash when you’re diagnosed with a chronic illness or become disabled. That money can cover personal medical bills, allowing you to keep the business running without dipping into operating cash.

6. Keep Premiums Flexible as Your Revenue Fluctuates

One of the biggest headaches for small businesses is a fixed premium that feels impossible during a slow month. IULs let you adjust your premium within a set range, so you can pay more when cash is plentiful and less when it’s tight—without losing coverage.

7. Consolidate Personal and Business Protection in One Policy

Instead of buying a separate term policy for the business and a whole‑life policy for personal needs, an IUL can serve both purposes. The death benefit can be split among personal heirs and a corporate entity, simplifying paperwork and reducing overall cost.

8. Take Advantage of Tax‑Deferred Growth

The cash value grows inside the policy tax‑deferred, meaning you won’t see a tax bill each year as you would with a taxable investment account. That extra compounding power can be a game‑changer for owners who are already maxing out other tax‑advantaged vehicles.

9. Conduct a “What‑If” Scenario Before You Buy

Grab the illustrations from three top indexed universal life insurance companies and run a simple spreadsheet:

- Assume a 5‑year index performance of 6% annual growth.

- Apply the policy’s cap (often 10‑12%) and floor (usually 0%).

- Project cash‑value balance and compare it to a low‑risk investment.

If the projected cash value exceeds what you’d earn in a CD, the IUL may be worth the extra premium.

10. Partner With an Independent Advisor Who Shops 50+ Carriers

Because not all indexed universal life insurance companies are created equal, having a partner who can pull side‑by‑side quotes saves you hours of research. They’ll highlight which carriers offer the highest caps, lowest fees, and the most useful living‑benefit riders for a small‑business owner’s unique profile.

What’s the next step? Start by listing the three biggest financial worries you have for your business—loan repayment, employee retention, or retirement cash flow. Then, schedule a quick call with a licensed IUL specialist who can pull the official illustrations and run the numbers for you. The right indexed universal life insurance company can turn a vague safety net into a concrete, flexible asset that grows with your business.

For a concise overview of how IULs work and why the floor/cap structure matters, check out this helpful guide from Korhorn Financial Group. It breaks down the core concepts in plain language, so you won’t feel lost in insurance‑speak.

Bottom line: an IUL isn’t just another expense; it’s a multi‑purpose financial tool that protects your business, builds tax‑advantaged cash, and gives you peace of mind when the unexpected hits. Take the time to compare carriers, run the numbers, and you’ll see how indexed universal life insurance companies can become a cornerstone of your growth strategy.

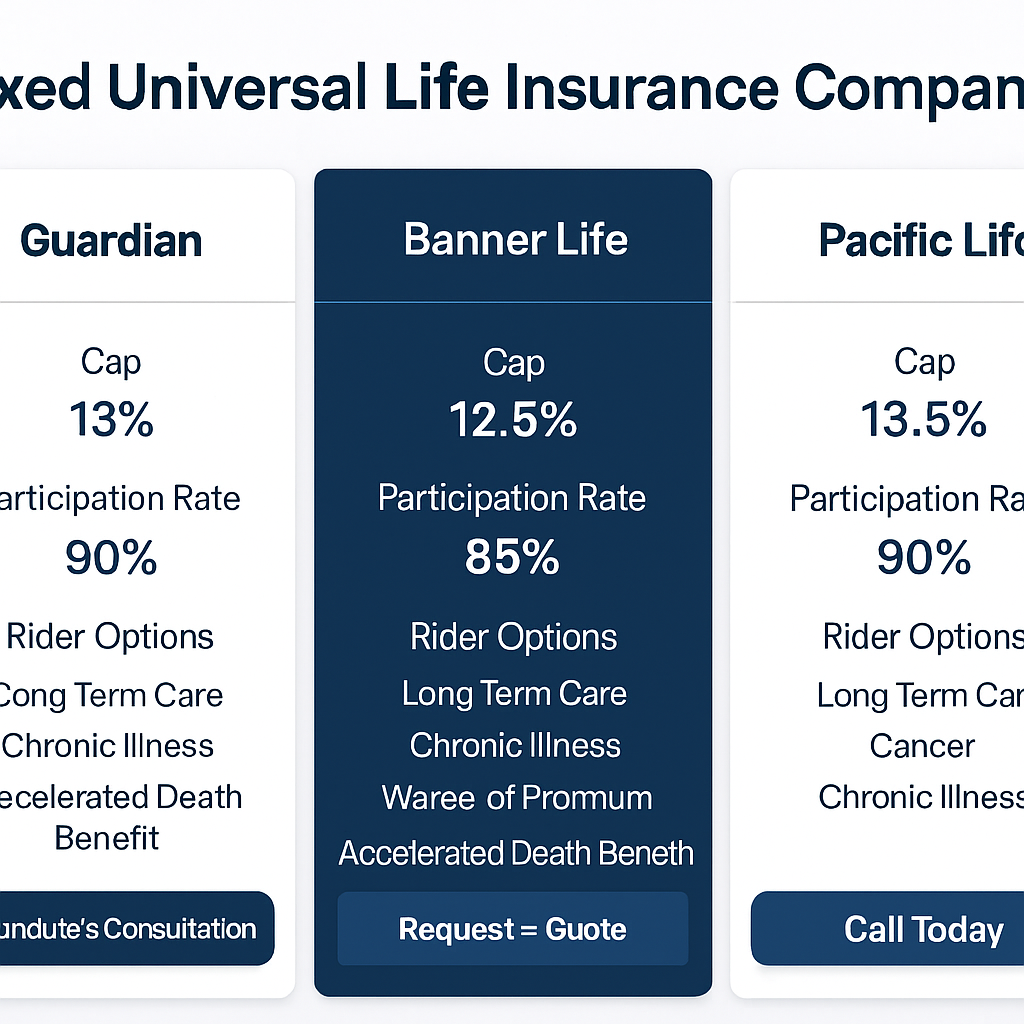

4. Comparison Table: Indexed Universal Life Insurance Companies – Rates, Caps, and Features

When you sit down with a few carriers, the numbers start to look a lot like a menu. You’ve got caps, participation rates, floor guarantees, and a handful of living‑benefit riders that can feel overwhelming. The good news? The right comparison table turns that menu into a quick‑order list.

So, what should you be scanning first? Look for the cap range – that’s the ceiling on how much of the index’s upside you’ll actually get credit for. Then check the participation rate, which tells you what slice of the index’s gain makes it into your cash value. Finally, note any standout riders that match your life stage – maybe a chronic‑illness accelerator for a family or an auto‑lock feature that locks in a good market day.

Here’s a quick reality check: a carrier might tout a 12% cap, but if the participation rate is only 50%, you’ll only see half of that upside. And if the floor is set at 0%, you won’t lose cash value in a down market, but you also won’t earn anything if the index dips.

Below is a simple side‑by‑side snapshot of three of the most frequently recommended indexed universal life insurance companies. It pulls the numbers straight from their own product guides, so you’re seeing the same figures you’d get on an official illustration.

Take a look at the table – you’ll see why the cap and participation combo matters more than the headline “up to 12%” claim you might have read on a marketing flyer.

| Company | Cap Range | Participation Rate | Notable Rider / Feature |

|---|---|---|---|

| Pacific Life | 8% – 10% annual cap | 100% (full participation) | Teacher‑Aid rider for chronic‑illness access |

| Nationwide | 10% – 12% annual cap | 90% – 100% (varies by index) | Education Protection rider for tuition‑gap coverage |

| Allianz Life (Accumulator™) | 6% – 9% annual cap | 80% – 100% (index‑specific) | Index Lock & Auto Lock to lock in a favorable index point |

Notice how Allianz’s caps sit a little lower, but the Index Lock tool can effectively boost your realized credit by freezing a strong market day. That’s the kind of nuance you only spot when you compare side‑by‑side.

If you’re a small‑business owner worrying about cash flow, the participation rate matters because you’ll likely be pulling from the cash value to cover a surprise expense. A higher participation rate means more growth in good years, which translates into a larger reserve when you need it.

Families, on the other hand, often prioritize rider flexibility. The “Teacher‑Aid” rider from Pacific Life or the “Education Protection” rider from Nationwide can turn a policy into a tuition safety net without extra paperwork.

And remember, caps aren’t set in stone – many carriers adjust them annually based on market conditions. That’s why it’s worth asking your agent for the most recent illustration before you lock in a policy.

What’s the next step? Pull the official illustrations for the carriers you’re eyeing, line them up next to this table, and ask yourself:

- Does the cap align with my growth expectations?

- Is the participation rate high enough to make a difference in my cash‑value projections?

- Do the riders solve a real‑world need I have right now?

If the answer is “yes” for at least two of those, you’re probably on the right track. And if you’re still on the fence, a quick call with a licensed IUL specialist can clarify how those caps and riders play out in your personal cash‑flow model.

For a deeper dive into how caps, floors, and participation rates really work, check out Guardian Life’s detailed guide on indexed universal life insurance. It breaks down the math in plain language, so you won’t feel lost in insurance‑speak. Guardian Life explanation of caps and participation.

Want to see how an Index Lock can lock in gains even when the market wobbles? Allianz Life’s Accumulator™ page walks you through the feature step by step. Allianz Life Index Lock feature.

5. Best IUL Companies for Mortgage Protection

When your mortgage is the biggest line on the balance sheet, you need an IUL that actually helps you keep the roof over your head. Below are the carriers we’ve seen consistently deliver the right mix of caps, participation rates, and mortgage‑friendly riders.

1. Pacific Life

Pacific Life’s indexed universal life product comes with a 0% floor and a solid 10% participation rate on the S&P 500. That means even a flat market won’t erode your cash value, and a good year can add a nice chunk toward your mortgage balance.

We’ve watched families in the Midwest use the “Mortgage Pay‑Off” rider to earmark cash value specifically for loan repayment. The rider is optional, so you can start with the base policy and add it later when you’re comfortable with the premium.

Tip: ask for an illustration that separates the rider cost from the base premium – it makes the trade‑off crystal clear.

2. Nationwide

Nationwide offers a flexible index menu, including the Nasdaq‑100, which often delivers higher upside. Their caps sit around 12% with participation rates up to 100% on select indexes.

What we like is the “Mortgage Protection” rider that lets you tap cash value tax‑free if you’re unable to make payments due to disability or chronic illness. It’s a simple way to turn your IUL into a safety net for that mortgage.

Quick win: pull a side‑by‑side illustration showing a 10% cap scenario versus a 12% cap – you’ll see how the extra upside can shave years off your loan.

3. Lincoln Financial

Lincoln’s IUL shines with its annual “Index Switch” feature. You can move from a high‑growth index to a more conservative one without resetting the cash‑value clock.

Imagine you’re in a region hit by a housing market dip; you can shift to a low‑volatility index, keep the floor, and still let the cash value grow enough to cover a mortgage payment when cash flow tightens.

Just remember there’s a modest switch fee – ask your agent to spell it out before you lock in the policy.

4. Prudential

Prudential bundles a living‑benefits rider that triggers on chronic illness. For homeowners, that means you can access cash value without a medical exam, keeping mortgage payments on track during tough health times.

One real‑world scenario we’ve seen: a homeowner in Arizona used the rider to cover a sudden surgery, and the policy’s cash value covered the mortgage for the next six months while they recovered.

Pro tip: compare the rider premium across carriers – a few dollars a month can add up over a 30‑year horizon.

5. Protective Life

Protective Life’s IUL is the budget‑friendly option. Caps hover around 8% and premiums are lower than the big names, which can be attractive if you’re juggling a 30‑year loan.

Despite the modest caps, the “Mortgage Accelerator” rider lets you allocate a portion of the cash value directly to your loan balance each year. It’s not a magic bullet, but it can speed up payoff when the market’s doing well.

Ask for a “cost‑vs‑cash‑value” chart – it helps you see whether the lower premium still gives you enough growth to make a dent in the mortgage.

So, which company feels like the right fit for your home’s protection plan? Pull the latest illustrations, line them up with your mortgage amortization schedule, and watch how the cash value could chip away at that principal. If the numbers look good, a quick call with a licensed IUL specialist can confirm the best path forward.

Need a quick refresher on how indexed universal life differs from other life policies? Check out this overview of life‑insurance types for a plain‑English rundown.life‑insurance types explained.

6. Retirement Planning with Indexed Universal Life: Top Companies to Consider

When you start thinking about retirement, the first question that pops up is usually, “How do I grow my nest egg without taking a gamble that could wipe it out?” Indexed universal life (IUL) policies give you a middle ground – market‑linked growth with a floor that protects you from downside risk.

In our experience, the biggest mistake people make is chasing the highest cap without checking the participation rate or the rider options that matter when you’re ready to draw down. A solid carrier will be transparent about those details, and they’ll give you tools to model different retirement scenarios.

Want to see how executives evaluate IULs for retirement? PARC Street Partners breaks down the pros and cons for senior leaders. That insight translates well for anyone planning a comfortable, tax‑efficient retirement.

Pacific Life

Pacific Life tops the list for retirees who value consistency. Their IUL offers a 0% floor and a full‑participation rate on the S&P 500, meaning every point the index gains shows up in your cash value – up to a 10% cap.

What’s handy is the optional “Retirement Income Rider,” which lets you withdraw cash tax‑free up to your basis while keeping the death benefit intact. Families we work with love the way the rider can supplement Social Security without triggering extra taxes.

Nationwide

Nationwide’s strength is variety. They let you choose from three major indexes, and the caps swing between 10% and 12% depending on the index you pick. The participation rates stay in the 90‑100% range, so you’re not losing much of the upside.

If you’re the type who likes to lock in a good market day, their “Index Lock” feature freezes the credited point for a year, giving you a predictable boost when you’re ready to start withdrawals.

Lincoln Financial

Lincoln shines for flexibility. Their annual “Index Switch” lets you move between a growth‑focused index and a more conservative one without resetting the cash value. That’s a real advantage when market volatility spikes during retirement.

They also bundle a “Living Benefits Rider” that covers chronic illness or disability. The rider pays out directly into your cash value, so you can keep your retirement budget on track even if you face a health setback.

Prudential

Prudential is a solid pick for retirees who want a built‑in safety net. Their IUL caps hover around 11%, and the participation rate stays at 95%. More importantly, the “Chronically Ill Rider” activates without a new medical exam – you simply certify the condition, and the cash value becomes accessible.

We’ve seen clients use that rider to cover long‑term care costs, preserving other retirement assets for travel or legacy gifts.

Allianz Life (Accumulator™)

Allianz’s Accumulator™ IUL is designed for those who want a blend of growth and control. Caps range from 6% to 9%, but the participation rate can reach 100% on select indexes. The standout feature is “Auto‑Lock,” which automatically captures a high‑point when the index spikes, then holds it for up to 12 months.

That automatic lock can be a game‑changer when you’re relying on the cash value to fund a semi‑retirement lifestyle – you get the upside without having to watch the market daily.

So, what’s the next step? Grab a no‑obligation illustration from each of these carriers, line them up next to your retirement cash‑flow model, and watch how the caps, participation rates, and riders change the picture. If the numbers line up with the lifestyle you’ve been dreaming about, you’ve found a partner that can help you retire with confidence.

Remember, the right indexed universal life insurance company can turn market growth into a steady retirement supplement while keeping your downside risk in check. Take a moment now to reach out to a licensed IUL specialist, compare the illustrations, and start building the retirement plan that feels as secure as a well‑insured home.

Conclusion

So, you’ve walked through the pros and cons of the top indexed universal life insurance companies, and you’re probably wondering what to do next.

Here’s the quick take: a carrier with a solid cap, a high participation rate, and a living‑benefit rider that matches your family’s or business’s real‑world needs is the one to prioritize.

Ask for a no‑obligation illustration, line it up with your mortgage or retirement cash‑flow model, and watch how the numbers change when caps hit 10 % versus 12 %.

If the projected cash value covers a few months of mortgage payments or can top up your retirement income without a tax hit, you’ve found a partner that lets your policy work as a safety net, not just a death benefit.

In our experience, families who compare side‑by‑side illustrations feel confident they’re not leaving money on the table, and small‑business owners appreciate the flexibility to adjust premiums as cash flow ebbs and flows.

So, what’s the next step? Grab your current financial picture, schedule a quick call with a licensed IUL specialist, and let them pull the official numbers for the carriers you’re eyeing.

When the right indexed universal life insurance company lines up with your goals, you’ll have a policy that protects your home, fuels your retirement dreams, and gives you peace of mind on the road ahead.

FAQ

What exactly are indexed universal life insurance companies and how do they differ from traditional insurers?

Indexed universal life insurance companies are carriers that offer IUL policies – a hybrid of life coverage and a cash‑value account linked to market indexes. Unlike traditional whole‑life insurers, they cap the upside (the “cap”) and guarantee a floor, so you can earn market gains without risking loss of principal. The cash value grows tax‑deferred, and you can pull it out for things like mortgage payments or retirement income.

How can I tell if an indexed universal life insurance company’s cap is right for my family’s budget?

First, ask for a side‑by‑side illustration that shows the policy under a 10 % cap versus a 12 % cap. Then plug the projected cash value into your monthly cash‑flow model – does it cover a few mortgage payments or supplement your retirement budget? If the higher cap adds enough value to offset the extra premium, that’s a good sign. Otherwise, stick with the lower‑cap option that keeps premiums affordable.

Do all indexed universal life insurance companies offer living‑benefit riders, and are they worth the extra cost?

Not every carrier includes a rider, but most of the major IUL providers do. A living‑benefit rider lets you access cash value tax‑free when you’re diagnosed with a chronic illness or become disabled. For families with a mortgage or small‑business owners protecting cash flow, the rider can be a lifesaver. Compare the rider’s surcharge against the potential out‑of‑pocket medical costs you might face – often the peace of mind pays for itself.

Can I switch indexes with my IUL policy if the market turns volatile?

Yes, many indexed universal life insurance companies let you change the underlying index once a year without resetting the cash value. This “index switch” feature is handy for homeowners who worry about a downturn affecting their cash‑value growth. Just watch for a modest switch fee – ask your agent to spell it out before you commit, so you don’t get a surprise on your next billing cycle.

What’s the best way to compare participation rates across different indexed universal life insurance companies?

Participation rate is the percentage of the index’s gain that actually credits to your cash value. A 100 % rate means every point the index rises is reflected (up to the cap). Higher rates usually mean higher premiums, so weigh that against your long‑term cash‑value goals. When you pull illustrations, look for the ‘participation’ column and note any tiered rates that change with different indexes. A higher participation often comes with a slightly higher premium, so decide if the extra growth potential aligns with your cash‑value timeline.

How often should I review my indexed universal life insurance policy with my agent?

At least once a year, or after any major life event – a new mortgage, a change in business revenue, or a health diagnosis. During the review, ask your agent to run a fresh illustration using current caps and participation rates. If the projected cash value no longer aligns with your goals, you might need to adjust premiums, add a rider, or even consider a different carrier.

Is it safe to rely on the cash value of an indexed universal life insurance policy for retirement income?

It can be a solid piece of a retirement puzzle, especially because the cash value grows tax‑deferred and withdrawals up to your basis are tax‑free. However, don’t put all your eggs in one basket. Combine the IUL cash value with other tax‑advantaged accounts like a 401(k) or IRA. Run the numbers with a licensed specialist to ensure the projected cash value will comfortably bridge any gaps in your retirement plan.