Imagine you’re a third‑grade teacher named Maya. She just bought a modest two‑bedroom house, her husband just got a promotion, and she’s planning a summer trip with the class. Then, out of the blue, Maya’s father is diagnosed with a serious illness, and the medical bills start to pile up. Maya worries: if something happens to her, who will pay the mortgage? Who will cover the kids’ college fund? This is the exact spot where life insurance for teachers steps in. It gives Maya a safety net that protects her family today and tomorrow, while also offering cash options she can tap while she’s still alive. In this guide we’ll walk through the biggest pieces of that puzzle—what teachers need, how living benefits work, why indexed universal life (IUL) can be a smart fit, what group plans look like, and how to blend mortgage protection with retirement planning. By the end you’ll have a clear roadmap and a few next‑step actions you can take right now.

Understanding Life Insurance Needs for Teachers

Life insurance for teachers isn’t a one‑size‑fits‑all product. Teachers often start their careers with modest salaries, student loans, and a desire to give back to the community. That mix means they need coverage that balances affordability with enough protection to cover a mortgage, a child’s education, and any unexpected expenses.

First, look at the “what if” scenarios. What if you’re hit by a car on the way to school? What if you need to take a leave of absence for a chronic condition? What if you decide to retire early and want to lock in a cash reserve? Each of these moments can drain savings fast, and a well‑structured policy can keep you from dipping into your emergency fund.

Teachers also have a built‑in advantage: many unions and associations negotiate group rates that are lower than the public market. For example, the Canadian fraternal insurer Teachers Life has offered members simple, exam‑free policies with a 30‑day money‑back guarantee (Teachers Life official site). This makes it easier for a teacher to get coverage without a medical exam, which can be a big plus for busy educators.

Here are three actionable tips to size up your need:

- Calculate your total debt. Add up mortgage, student loans, and any other long‑term obligations. Multiply that number by 1.5 to get a rough coverage target.

- Factor in future expenses. Project tuition costs for each child and add a buffer for potential health care costs.

- Review your employment benefits. Check whether your district offers a group term life plan that can serve as a base layer.

Real‑world example: Ms. Patel, a fifth‑grade teacher in Ontario, used the Teachers Life calculator to find that a $250,000 policy would cover her mortgage, a $30,000 student loan, and leave enough for a college fund for her two kids. She applied online, got approved without a medical exam, and saved $15 a month compared to a standard term policy.

When you start your search, keep an eye on these three things: premium cost, coverage amount, and any built‑in riders that add living benefits. And remember, the right amount of life insurance for teachers can grow with you as your career and family evolve.

Living Benefits: Protecting Your Health and Finances While You’re Alive

Living benefits let you turn a death benefit into a cash resource while you’re still breathing. This is a game‑changer for teachers who might face a sudden illness or injury that stops them from working for months.

The NEA offers a complimentary $1,000 term life plan to eligible members, plus up to $5,000 of accidental death and dismemberment coverage (NEA Complimentary Life Insurance). While the amount seems small, it shows how even modest policies can include living‑benefit riders that pay out for critical illnesses or severe injuries.

Virginia’s VRS Group Life program adds a twist: it doubles your creditable compensation as a natural death benefit and adds an equal amount for accidental death (VRS Group Life details). Plus, it lets you withdraw part of the benefit if you’re diagnosed with a terminal condition, giving you cash to cover medical bills or mortgage payments.

Here’s how a living‑benefit rider typically works:

- Trigger event occurs (e.g., diagnosis of a chronic illness).

- Policyholder files a claim and receives a percentage of the death benefit, often 25‑50%.

- The payout reduces the eventual death benefit dollar‑for‑dollar.

Why does this matter for teachers? Because many districts now charge higher health‑insurance premiums. In Palm Beach County, teachers will see an $18 increase per pay period in 2026 (WPTV health‑cost report). Having a living‑benefit rider can offset those extra costs if a health event reduces income.

Actionable checklist for teachers:

- Ask your insurer if an accelerated death benefit rider is included at no extra cost.

- Confirm the trigger conditions—some policies require a life expectancy under 12 months, while others cover specific critical illnesses.

- Run a “what‑if” scenario: if you need $20,000 for a surgery, how much of your policy would be left for your family?

Real‑world scenario: Jenna, a high‑school science teacher, added a chronic‑illness rider to her policy. When her husband faced a heart attack, the rider paid $15,000 toward specialist visits, allowing Jenna to keep teaching without financial stress.

Living benefits give you a safety net that can keep your classroom focus sharp, even when life throws a curveball.

Remember, the key is to match the rider size to your likely expenses. Too small, and you won’t cover the bill; too large, and you’ll cut down the death benefit more than needed.

Indexed Universal Life (IUL) Explained for Educators

Indexed universal life insurance blends a death benefit with a cash‑value account that grows based on a market index, but without the risk of losing principal. For teachers who want a long‑term safety net and a tax‑free source of retirement cash, an IUL can be a solid fit.

According to Abrams Inc., an IUL provides a death benefit plus a cash value that isn’t exposed to market downturns because it has a floor, usually 0% (Abrams IUL overview). The cash can be borrowed tax‑free after age 59½, or even earlier if you’re willing to pay surrender charges.

Why does the floor matter? Imagine you have $100,000 in a regular brokerage account and the market drops 15%. Your balance falls to $85,000. With an IUL, the cash value stays at $100,000 (minus fees) because the floor protects you from loss. In a year when the index climbs 15%, the cash value can rise to about $115,000, capped at a set participation rate.

Teachers often have irregular cash flow—summer breaks, extra tutoring gigs, or sabbaticals. IULs let you adjust premium payments to match those fluctuations. You can pump more in during a busy tutoring season and pull back when school is out.

Here are three steps to evaluate an IUL:

- Check the cap and participation rate. A higher cap (e.g., 12%) and participation rate (e.g., 100%) give you more upside.

- Look at the floor. Most IULs have a 0% floor, which means you won’t lose cash value in a down market.

- Review policy fees. IULs have higher initial costs, but many carriers front‑load fees that drop after 5‑10 years.

Real‑world example: Mark, a high‑school teacher nearing 60, maxed out his 403(b). He took an IUL quote with a $150 monthly premium, 4% participation on the Nasdaq‑100, and a 7% cap. By age 65 the policy projected $80,000 cash value, which he could withdraw $5,000‑$6,000 per year tax‑free to top up his modest pension.

When you talk to an agent, ask for a side‑by‑side illustration that shows:

| Feature | IUL Example | Traditional 401(k) |

|---|---|---|

| Growth potential | Indexed with cap/floor | Market‑linked, no floor |

| Tax treatment | Tax‑deferred, loans tax‑free | Tax‑deferred, withdrawals taxable |

| Liquidity | Policy loans anytime | Withdrawals after age 59½ |

For teachers who want a policy that lasts a lifetime and can act as a supplemental retirement account, an IUL often makes sense. Just be sure to compare carriers, caps, and fees before you lock in.

Group Benefits and Small Business Options for Teachers

Many teachers work part‑time, run tutoring businesses, or help out with after‑school programs. Group life plans can cover both full‑time staff and these side‑gig workers, giving them a consistent safety net.

The NEA Group Term Life Insurance Plan offers flexible coverage from $25,000 to $500,000, with the ability to change coverage any time (NEA Group Term Life). Premiums can be waived if you lose your job or become disabled, which is a huge plus for teachers who face contract uncertainties.

In Palm Beach County, the new health‑insurance deal will increase teacher contributions by $18 per pay period in 2026 (WPTV health‑cost report). Adding a group life rider can offset those higher health costs by providing a cash payout if a serious illness strikes.

Small‑business owners who employ teachers (e.g., private tutoring centers) can also tap group benefits. A typical setup looks like this:

- Choose a carrier that offers both health and life insurance under a single contract.

- Select a base death benefit (e.g., $100,000) and add a living‑benefit rider for chronic illness.

- Pay premiums through payroll deductions, making it tax‑deductible for the business.

Actionable tips for educators who run a side business:

- Ask your insurance broker about “group term life with living‑benefit riders.”

- Set the rider amount to 10‑15% of the base coverage to match average debt loads.

- Review the policy annually—especially after hiring new staff or changing your business model.

Real‑world scenario: Sarah, a part‑time teacher who runs an online tutoring service, added a $50,000 group term policy with a chronic‑illness rider. When she broke her ankle and couldn’t teach for six weeks, the rider paid $10,000, covering her mortgage and allowing her to keep her business afloat.

Group benefits give you flexibility and can be a cost‑effective way to protect both your family and your side business.

[VIDEO: Placeholder for an educational video about group benefits for teachers – actual video embed not required per guidelines.]

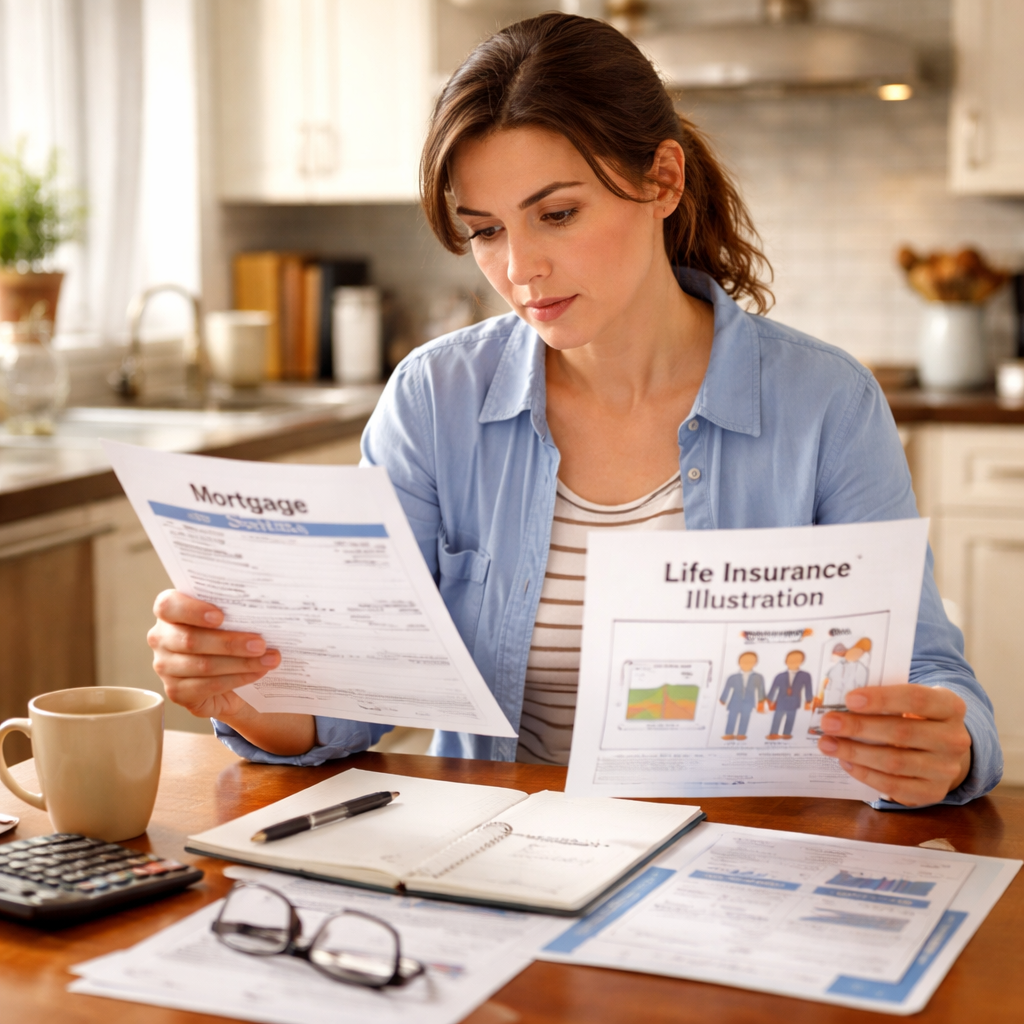

Mortgage Protection and Retirement Planning Strategies

When you buy a house, the mortgage becomes one of your biggest monthly bills. If you’re a teacher, a sudden loss of income can put that payment at risk. Mortgage protection insurance can act as a bridge, while a well‑structured life insurance policy can also serve as a retirement supplement.

Horace Mann designs life policies with special educator rates, emphasizing early purchase for flexibility (Horace Mann educator rates). The death benefit can be directed to pay off the mortgage if you pass away, ensuring your family stays in the home.

Equitable highlights the power of a 403(b) plan for teachers, noting that many educators use it alongside life insurance to build a retirement nest egg (Equitable 403(b) guide). By pairing a 403(b) with an IUL, you get both tax‑deferred growth and a death benefit that can fund mortgage payoff or legacy goals.

Here’s a step‑by‑step plan to blend mortgage protection and retirement:

- Determine your mortgage balance. Write down the current principal and the remaining term.

- Choose a death benefit that covers the balance. For example, a $300,000 policy on a $250,000 mortgage leaves a $50,000 buffer.

- Add an accelerated death benefit rider. This lets you tap a portion of the death benefit if you’re diagnosed with a chronic illness.

- Allocate a portion of your premium to cash value. In an IUL, the cash can grow tax‑free and be borrowed against for retirement income.

- Review annually. As you pay down the mortgage, you can lower the death benefit or shift more cash into the retirement side.

Actionable tip list:

- Use a mortgage calculator to see how a $150,000 life insurance payout would cover your loan after 10 years.

- Ask for a policy illustration that shows the cash‑value growth at different cap rates (e.g., 8% vs. 12%).

- Set up automatic premium payments to avoid lapse during summer breaks.

Real‑world example: Mrs. Lopez, a second‑grade teacher, bought a $200,000 IUL when she purchased her starter home. Ten years later, the cash value hit $40,000. When she needed to cover a missed mortgage payment due to a temporary disability, she borrowed $5,000 against the cash value, keeping her home secure without tapping savings.

Combining mortgage protection with an IUL gives you a dual purpose: a safety net for the house and a tax‑advantaged retirement supplement.

Conclusion

Life insurance for teachers isn’t just about a payout after you’re gone. It’s a flexible tool that can protect your family’s home, give you cash when illness strikes, and even boost your retirement savings. We’ve covered the basics of how to size up your need, the power of living‑benefit riders, why an indexed universal life (IUL) can serve as a long‑term cash engine, the value of group plans for side‑business teachers, and a step‑by‑step way to mix mortgage protection with retirement goals. Take the next step: schedule a free consultation with Life Care Benefit Services today. A quick call can help you compare quotes, run “what‑if” scenarios, and lock in a policy that fits your budget and future plans.

FAQ

What amount of life insurance for teachers is generally recommended?

Most experts suggest a coverage amount that equals 1.5 times your total debt—mortgage, student loans, and any other long‑term obligations. For a teacher with a $200,000 mortgage and $30,000 in loans, a $345,000 policy would provide a solid buffer while also leaving room for future expenses.

How do living‑benefit riders affect my premiums?

Riders usually add a small percentage to your base premium—often 5‑10 %. The exact cost depends on the trigger events covered and the payout percentage. While the extra cost raises your monthly payment, the ability to access cash during a critical illness can prevent you from dipping into savings.

Can I adjust my IUL premiums if my income changes?

Yes. One of the strengths of an IUL is flexible premium options. You can increase payments during a busy tutoring season and lower them during summer breaks. Just be aware that dropping premiums too low for several years may affect the cash‑value growth and could trigger a policy lapse if the cash balance can’t cover the cost of insurance.

Are group term life plans portable if I change schools?

Many group plans let you convert the coverage to an individual policy and keep the same rates by paying the premiums yourself. This portability ensures you don’t lose protection when you move to a new district or start a private tutoring business.

How does an IUL compare to a 403(b) for retirement?

An IUL offers tax‑deferred cash growth plus a death benefit, while a 403(b) is a tax‑deferred investment account with contribution limits. An IUL can provide tax‑free loans for retirement income, which a 403(b) cannot. However, IULs have higher fees, so many teachers use both: a 403(b) for regular savings and an IUL for a lifelong safety net.

What should I look for in a mortgage‑protection rider?

Key points include the trigger (e.g., disability or critical illness), the payout percentage (often 25‑50 % of the death benefit), and whether the rider reduces the death benefit dollar‑for‑dollar. Also check if the rider can be added without a medical exam, which can save time and cost.

Where can I learn more about AI tools for SEO?

You can explore related ideas at How to Choose and Use an AI SEO Audit Tool in 2026. This guide walks you through selecting, setting up, and getting the most out of AI‑driven SEO audits.

How do I choose the right photo booth for school events?

For event ideas, see Photo Booth Rental Murrieta: A Complete Guide for 2026 Events. It covers pricing, setup tips, and top providers that can make school functions memorable.