Ever felt that knot in your stomach when you think about what would happen to your family if the unexpected knocked you off your financial footing?

You’re not alone—most homeowners, teachers, and small‑business owners worry that a mortgage could become a burden for loved ones when life throws a curveball.

That’s where the debate between mortgage protection insurance vs life insurance really matters, because each product frames protection differently and fits distinct life stages.

Mortgage protection insurance is laser‑focused on one thing: paying off your home if you pass away or become disabled, often with a term that matches the length of your loan.

Life insurance, on the other hand, casts a wider net. A term or indexed universal life (IUL) policy can replace lost income, cover college tuition, or even fund a retirement bridge, while still offering the option to clear the mortgage.

But the right choice isn’t about picking a winner; it’s about layering protection so you feel secure no matter what curveball comes your way.

Imagine you’re a teacher with a 20‑year mortgage. A mortgage protection policy could cover the exact balance when you retire, yet a term life policy might give you the flexibility to handle unexpected medical bills or help your kids buy their first home.

So, how do you decide? Start by mapping out your financial goals: Do you need a safety net that mirrors your loan amount, or do you prefer a versatile tool that grows with you?

Next, look at the cost side. Mortgage protection premiums are often tied to the loan balance and age, while life insurance rates depend on health, age, and the amount of coverage you select.

Finally, think about living benefits. Some indexed universal life policies let you tap cash value for emergencies, a feature you won’t find in a pure mortgage protection plan.

Bottom line: blend the two when it makes sense, and let a trusted advisor walk you through the numbers so you can protect both your home and your broader financial future.

TL;DR

Choosing between mortgage protection insurance and life insurance boils down to whether you need a dedicated safety net that clears your loan or a flexible policy that also covers income loss, medical costs, and future goals.

We recommend mapping your financial priorities, comparing premium structures, and considering living‑benefit options like indexed universal life, then consulting a trusted advisor to blend the right coverage for lasting peace of mind.

Understanding Mortgage Protection Insurance

When you first hear the term mortgage protection insurance, the first thing that often pops into your mind is a safety net that kicks in if you can’t make your mortgage payments anymore.

But it’s not just about a blanket promise; it’s a contract that’s usually tied directly to the balance of your loan and the length of your term.

In practice, a typical mortgage protection policy will pay the remaining mortgage balance to your lender if you pass away or become permanently disabled, often without the need for a medical exam.

That sounds simple, right? The simplicity is actually one of its biggest draws for families who want to know exactly how much will be needed to keep the roof over their heads.

Now, let’s dig a little deeper. There are three core components you should understand before you decide whether mortgage protection insurance vs life insurance is the right fit for you.

Coverage Triggers

The policy usually activates on two events: death and total disability. Some carriers also add a “critical illness” rider, but that’s less common than with a traditional life policy.

If you become disabled, the insurer typically requires proof that you can’t work a job that pays at least a certain percentage of your pre‑disability income. That proof can feel a bit bureaucratic, but it’s designed to keep the benefit from being paid out for short‑term injuries.

Premium Structure

Premiums are calculated based on your age, health, and the amount of mortgage you owe. Because the coverage amount drops as you pay down the loan, many policies let the premium decrease over time, which can feel like a built‑in discount.

Contrast that with a term life policy, where the face amount stays the same for the whole term, so the premium stays flat even though your mortgage balance shrinks. That’s why mortgage protection can be cheaper if you only need coverage equal to the loan balance.

If you’re a visual learner, here’s a quick rundown of how a typical mortgage protection policy works.

Notice how the benefit is paid directly to the lender, not to you or your family. That distinction is why some folks pair a mortgage protection policy with a separate life policy that offers cash‑value or living benefits.

Picture a family sitting around the kitchen table, mortgage statements spread out, and a simple chart showing how the policy would wipe out the balance if something happened.

Another key feature to watch for is the “return of premium” option. Some carriers let you get back what you’ve paid if you outlive the policy, turning the coverage into a sort of forced savings plan.

But remember, that extra rider usually bumps the premium up by a few dollars a month. If your main goal is simply to protect the home, you might skip it and keep costs low.

So how does this compare to life insurance? A term life policy can be written for $500,000, which would cover your mortgage and still leave extra cash for emergencies. However, that same policy won’t automatically pay the lender; you’d have to direct the payout yourself.

That’s why many advisors suggest a hybrid approach: keep a mortgage protection policy that matches the loan balance, and layer a term or IUL policy that provides a larger death benefit and living benefits you can tap into while you’re still alive.

If you’re wondering where to start, a good first step is to get a quote from a reputable carrier. For a quick, no‑obligation estimate, you can visit the Consumer Watch Mortgage Assurance Society (CWMAS), which offers tools to compare rates and see how a mortgage‑only plan stacks up against a broader life policy.

How Life Insurance with Living Benefits Works

When you hear “life insurance with living benefits” you might picture a complicated, finance‑y product. Honestly, it’s not that scary – it’s just a regular life‑insurance policy that lets you borrow against or withdraw cash while you’re still alive.

Think about it like this: you’ve got a safety net that pays out if you pass, but it also doubles as a little emergency fund you can tap when life throws a curveball. That dual purpose is what makes living benefits so appealing to homeowners, teachers, and small‑business owners who want flexibility.

What exactly are living benefits?

Living benefits are riders or built‑in features that let you access a portion of your policy’s cash value if you become seriously ill, disabled, or need extra cash for a major expense. It’s not a loan from a bank; it’s money your own policy has accumulated.

For example, the NEA’s complimentary life‑insurance program for teachers offers a $1,000 term life benefit that can help cover large obligations like a mortgage or college costs, and the same policy can be upgraded with riders that provide cash payouts for critical illness or disability NEA complimentary life insurance for teachers. That’s a real‑world illustration of a living‑benefit feature in action.

How does the cash‑value component grow?

In a permanent policy such as an Indexed Universal Life (IUL) plan, a portion of each premium goes into a cash‑value account. The cash value is tied to a stock‑market index (like the S‑P 500) but never loses money when the index drops – the policy guarantees a zero‑floor.

What’s cool is that the cash‑value can earn higher, index‑linked returns while still enjoying a guaranteed minimum interest rate. That means your money can grow faster than a traditional whole‑life policy, giving you more to draw on later Indexed Universal Life (IUL) policies offer living benefits. You can think of it as a hybrid between a savings account and a safety net.

When should you actually use a living benefit?

Picture this: you’re a small‑business owner who just hit an unexpected equipment repair bill, or a teacher who needs to cover a sudden surgery cost. Instead of scrambling for a high‑interest personal loan, you can request a policy loan or withdrawal. The loan is tax‑free, and you only pay interest to the insurer – often lower than a credit‑card rate.

But there’s a catch: any unpaid loan reduces the death benefit for your beneficiaries. So it’s wise to treat a policy loan like a last‑resort option, and only pull cash when you’ve exhausted other low‑cost alternatives.

Choosing the right rider or policy

Not every life‑insurance plan comes with built‑in living benefits. Look for riders labeled “critical‑illness,” “accelerated death benefit,” or “disability income.” These riders usually cost a few extra dollars a month, but they can be a game‑changer if you ever need that cash.

Ask yourself:

- Do I want a policy that grows cash value over time (IUL) or one that stays level (term with a rider)?

- How much extra premium can I comfortably afford?

- Will I need the cash for a specific future event, like college tuition or a home renovation?

Answering those questions helps you pick a product that feels like a true financial partner, not just a death‑benefit check‑box.

Quick checklist to make living benefits work for you

1. Review your current coverage – does it already have an accelerated‑benefit rider?

2. Compare the cost of adding a rider versus buying a separate IUL policy.

3. Calculate how much cash value you’d need for a realistic “what‑if” scenario (e.g., $10,000 for a medical emergency).

4. Talk to an independent agent at Life Care Benefit Services – they can run side‑by‑side illustrations showing premium, cash‑value growth, and impact on death benefit.

5. Keep track of any loans you take; set a repayment plan to preserve the death benefit for your loved ones.

Bottom line: life insurance with living benefits isn’t a gimmick; it’s a flexible tool that lets you protect your family’s future while giving you a financial safety valve today. By understanding how the cash value builds, when to tap it, and which riders make sense for your life stage, you can turn a traditional life‑insurance policy into a multi‑purpose asset that works as hard as you do.

Video: Key Differences Between Mortgage Protection and Life Insurance

We just watched that 30‑second clip, right? If you hit pause, you probably noticed three things that stuck out: the payout destination, the underwriting hassle, and whether the policy can grow cash value. Let’s unpack those moments one by one.

Where does the money go?

Mortgage protection insurance (MPI) is a “pay‑off‑the‑loan” tool. The beneficiary is the lender, so the check goes straight to the bank and your family never has to scramble for cash to keep the roof over their heads. Life insurance, whether term or indexed universal life (IUL), names your loved ones as the beneficiaries. That gives you the freedom to use the lump sum for anything—college tuition, a new car, or even a second mortgage.

Because of that difference, MPI feels like a single‑purpose safety net, while a life‑insurance policy is more of a financial Swiss army knife.

How hard is it to get covered?

Most MPI plans boast “no medical exam” and guaranteed acceptance as long as you qualify for the underlying mortgage. That’s a huge relief if you have a pre‑existing condition. The VA’s own whole‑life offering, VALife, works the same way: it guarantees acceptance for eligible veterans without demanding a health exam — a good illustration of how “no‑exam” products can simplify protection VA guaranteed‑acceptance whole life.

Traditional life insurance, on the other hand, usually asks for a medical questionnaire, sometimes a lab draw, and can adjust rates based on your health profile. If you’re in great shape, the premiums can be lower than MPI, but the underwriting step adds time and uncertainty.

Does the policy grow?

MPI premiums stay level (or sometimes rise a bit each year) but the death benefit shrinks as you pay down the mortgage. There’s no cash value to tap if you hit a rough patch.

With an IUL or whole‑life policy, a portion of each premium feeds a cash‑value account that can earn interest tied to a market index, with a zero‑floor guarantee. That cash can be borrowed tax‑free or used for an accelerated death benefit, giving you a living‑benefit safety valve that MPI simply can’t match.

Even a plain term life policy, while not building cash, still leaves the face amount intact for the full term—so you can still pay off the mortgage and have leftover funds for other goals.

What does this mean for you?

Ask yourself: “Do I need a laser‑focused guarantee that the house will be paid off, or do I want a policy that can double‑duty as an emergency fund?” If you’re a first‑time homeowner with a modest loan and a clean bill of health, MPI might be the cheapest, simplest route.

If you’re juggling a mortgage, a growing family, and maybe a side hustle, a life‑insurance policy with a living‑benefit rider could give you that extra cushion. The Texas Department of Insurance notes that many life‑insurance policies also offer “accelerated benefits” while you’re still alive Texas life‑insurance guide, which is exactly the kind of flexibility we’re talking about.

Quick cheat sheet

- MPI: Direct to lender, no medical exam, no cash value.

- Term life: Beneficiaries decide use, may need medical underwriting, no cash value.

- IUL/Whole life: Beneficiaries decide use, builds cash value, can borrow or accelerate benefits, underwriting required.

Bottom line: the video nails the three core contrasts—payout destination, underwriting, and cash‑value potential. Use those lenses to decide which piece fits your financial puzzle. If you’re still on the fence, grab a free quote from Life Care Benefit Services and let a trusted advisor walk you through the numbers.

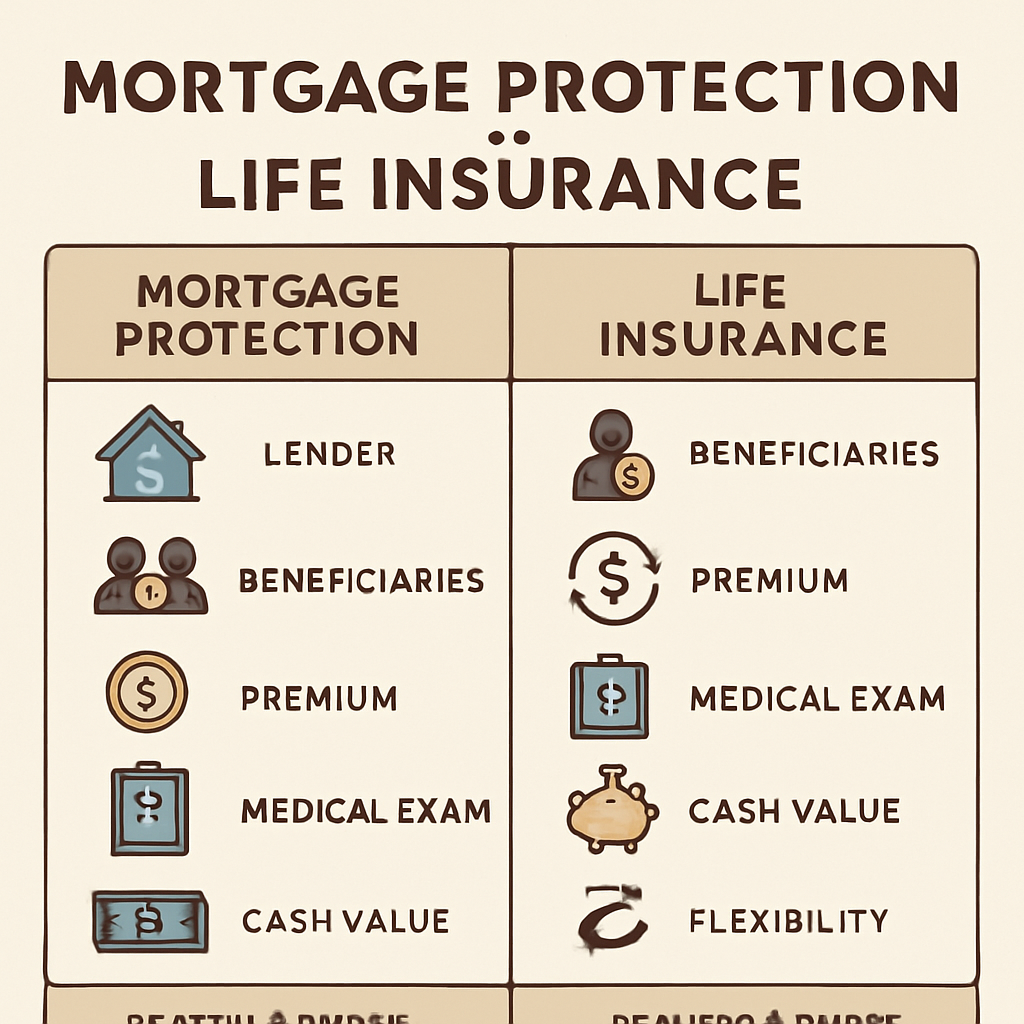

Comparing Mortgage Protection vs Life Insurance: A Side‑by‑Side Table

Okay, you’ve already seen how mortgage protection (MPI) zeroes in on the loan, and how a life‑insurance policy can do a lot more. But when you’re staring at two quotes, the details can get blurry. Let’s lay it out in plain English so you can see the trade‑offs at a glance.

What actually gets paid out?

With MPI, the benefit is tied to the balance you still owe. If you owe $180,000 today, the policy will pay $180,000 straight to the lender if you die or become disabled.

Traditional term or permanent life insurance, on the other hand, names your beneficiaries. The same $180,000 could go to your family, pay off the mortgage, fund college, or even be left as a legacy.

So, does the money go to the bank or to your loved ones? That’s the first line in the decision matrix.

Cost and premium structure

Mortgage protection premiums are often level for the life of the loan, but the benefit shrinks as you pay down principal. That means you might be paying the same amount when the loan is $50,000 as you were when it was $250,000.Life‑insurance premiums are based on the face amount you choose, your age, health, and the type of policy. A level‑face‑amount term stays the same for the whole term, and permanent policies can even build cash value over time.

Think about it like this: Do you want a predictable monthly bill that may become less efficient over time, or a premium that reflects the protection you truly need?

Underwriting and eligibility

Most MPI plans are “no‑exam” – you fill out a short form, and if you qualify for the mortgage, you’re in. That’s a lifesaver if you have a pre‑existing condition that would trip up a traditional insurer.

Life insurance usually asks for a medical questionnaire, sometimes a lab draw. If you’re healthy, you’ll probably get lower rates; if not, you might pay more or be declined.

Bottom line: MPI is the quick‑and‑easy route, while life insurance gives you room to shop around based on health.

Flexibility and living benefits

Mortgage protection does one thing and does it well: it pays the loan. No cash value, no policy loans, no accelerated death benefits.

Many modern life‑insurance policies offer living benefits – you can borrow against cash value, or trigger an accelerated death benefit if you’re diagnosed with a serious illness. That can act as an emergency fund without a high‑interest credit‑card debt.

According to the NC Department of Insurance, life‑insurance policies can include cash‑value growth and accelerated benefits, giving policyholders financial flexibility while they’re still alive.

Does having a safety net you can tap today matter to you? If yes, a life‑insurance policy with a rider might be the smarter play.

How to choose the right mix

Step 1: Write down your current mortgage balance and how many years are left. That’s your “minimum protection” number.

Step 2: List other financial goals – college, retirement, a rainy‑day fund. Estimate the lump sum you’d need for each.

Step 3: Get quotes for both MPI (often a quick online form) and a term life policy that covers at least your mortgage amount plus your extra goals.

Step 4: Compare the total cost over the life of the loan. Multiply the MPI monthly premium by the remaining years and see how it stacks up against the term‑life premium.

Step 5: Decide if you want any living‑benefit riders. If you have a stable health history, a term policy with an accelerated‑benefit rider can give you that extra cushion for a modest price.

And remember: you don’t have to pick one or the other. A hybrid approach – MPI for the core mortgage protection plus a modest term policy for everything else – often gives the best of both worlds.

| Feature | Mortgage Protection Insurance (MPI) | Life Insurance (Term or Permanent) |

|---|---|---|

| Primary Payout Destination | Directly to lender, pays off loan balance | Beneficiaries choose – mortgage payoff, savings, or other needs |

| Underwriting | No medical exam, guaranteed acceptance with qualifying mortgage | Medical questionnaire, possible lab work; rates vary with health |

| Cash Value / Living Benefits | None – pure death/disable benefit | Possible cash value (permanent) and accelerated death benefits (riders) |

| Premium Trend | Level premium, but benefit declines as loan is paid down | Level face amount; premiums stay level for term, can increase for permanent |

| Flexibility for Other Goals | Limited to mortgage only | Can fund college, retirement, emergency expenses, or any need |

Take a minute now to pull your mortgage statement and jot down the exact balance. Then fire off a quick quote for MPI and a term life policy that matches that number. Seeing the numbers side by side will make the decision feel a lot less abstract.

Ready to protect the roof over your head and keep your family’s financial future on track? The right combo is just a few clicks away.

Integrating Insurance Choices into Retirement and Small‑Business Planning

So you’ve mapped out whether mortgage protection insurance vs life insurance makes more sense for the roof over your head. The next question most people skip is: how does either choice fit into the bigger picture of retirement and running a small business? If you’re feeling that tug of uncertainty, you’re not alone.

Imagine you’re a teacher‑turned‑part‑time consultant. You’ve got a 20‑year mortgage, a fledgling side‑hustle, and a retirement account that’s still finding its footing. One policy can protect the house, another can keep the cash flowing when the business hits a slow month. The trick is weaving them together so they don’t compete for the same dollars.

Step 1 – Anchor your retirement horizon

First, write down the age you’d like to retire and the income gap you’ll need to fill. If you plan to retire at 65 and expect a $60,000 shortfall, that number becomes your “minimum protection” floor. A term life policy that covers the mortgage plus that shortfall gives you a two‑for‑one safety net.

But what if you’re self‑employed and your cash flow swings wildly? That’s where a permanent policy with living benefits – like an Indexed Universal Life (IUL) – shines. The cash‑value can be tapped in a pinch, acting like a low‑interest line of credit for business expenses or unexpected medical bills.

Step 2 – Layer mortgage protection as a dedicated floor

Mortgage protection insurance works like a floor under your financial house. It guarantees that, no matter what, the lender gets paid and your family stays housed. Because the benefit shrinks as the loan amortizes, the cost is predictable – a nice contrast to the variable cash‑value growth of an IUL.

Real‑world example: Carla runs a boutique bakery. She took out a 15‑year loan for her storefront. She added MPI with a benefit equal to her current balance. When a kitchen fire forced a temporary closure, the MPI premium stayed flat, and the policy’s death benefit would have cleared the loan if she hadn’t recovered. Meanwhile, her IUL’s cash value covered the repair costs without pulling from her emergency fund.

Step 3 – Use the life policy’s flexibility for retirement buckets

Life insurance isn’t just a death benefit; it can be a retirement bucket. With a term policy, the payout can be earmarked for a 401(k) catch‑up contribution or a Roth conversion once you’re past the mortgage.

Take Jeff, a small‑business owner who bought a $400,000 house at 35. He purchased a 30‑year term policy for $500,000. When he turned 55, the mortgage was almost paid off, and he used the term’s death benefit projection to fund a “bridge” IRA, allowing him to keep working part‑time while his retirement assets grew tax‑deferred.

Step 4 – Run the numbers, then schedule a check‑in

Grab a spreadsheet and plug in these four rows: mortgage balance, MPI premium, life‑policy premium, projected cash‑value growth. Multiply each premium by the years you expect to keep the policy, then compare that total cost to the lump‑sum you’d need to retire comfortably.

Here’s a quick cheat‑sheet:

- Mortgage balance + 5‑year buffer = minimum MPI benefit.

- Retirement income gap = life‑policy face amount.

- Check if the combined monthly premium stays under 10 % of your take‑home pay.

- Revisit every 3‑5 years or after a major life event (new hire, new child, big sale).

Need a concrete walkthrough? Our step‑by‑step guide to reviewing life‑insurance policies walks you through the exact calculations and shows how to align coverage with retirement goals.

Actionable checklist for today

1. Write down your mortgage balance and years left.

2. Calculate the retirement income gap you anticipate.

3. Get a quote for MPI and a term/IUL policy that covers both numbers.

4. Compare total costs over the life of each policy.

5. Set a reminder to review the mix in 12 months.

And remember, the best plan isn’t static – it evolves as your business grows, your kids go to college, and you inch closer to retirement.

By layering a mortgage‑specific policy with a flexible life‑insurance product, you protect the roof, the business, and the future you’ve been dreaming about.

Looking for a healthier balance in life and finances? Fitness and wellness starts here – because a strong body often leads to sharper financial decisions.

FAQ

What is the main difference between mortgage protection insurance and life insurance?

Mortgage protection insurance (MPI) is laser‑focused on one thing: paying off your loan if you die or become disabled. The benefit goes straight to the lender, so your family never has to scramble for cash to keep the house. Traditional life insurance, on the other hand, names your loved ones as beneficiaries, letting them decide whether the payout covers the mortgage, college tuition, or any other need.

Do I need a medical exam for mortgage protection insurance?

Most MPI plans are “no‑exam” – you fill out a short health questionnaire, and if you qualify for the mortgage, you’re in. That’s a lifesaver if you have a pre‑existing condition that might trip up a regular life‑insurance underwriting process. By contrast, term or permanent life policies usually ask for a medical questionnaire and sometimes a lab draw, which can raise premiums or lead to a denial.

Can I combine mortgage protection with a life‑insurance policy?

Absolutely. Think of MPI as the floor that guarantees the house stays paid, while a term or indexed universal life (IUL) policy sits on top, covering the mortgage plus everything else – retirement gaps, kids’ education, or an emergency fund. You’ll pay two premiums, but the combined cost often stays under 10 % of your take‑home pay if you size the policies to your actual needs.

How do premiums compare over time?

MPI premiums are usually level for the life of the loan, even though the death benefit shrinks as you pay down principal. That can feel inefficient toward the end of a 30‑year mortgage. Life‑insurance premiums are based on the face amount you choose, your age, and health. A level‑face‑amount term policy keeps the same premium for the whole term, while a permanent policy may grow but also builds cash value you can tap later.

What are “living benefits” and do they apply to mortgage protection?

Living benefits are riders that let you access part of the death benefit while you’re still alive – typically for serious illness, disability, or a major expense. MPI generally doesn’t offer these features; its payout is purely death or disability to the lender. A permanent life policy like an IUL often includes accelerated death‑benefit riders or cash‑value loans, giving you a financial safety valve before the final payout.

Which option is better for a small‑business owner?

If you run a business and your cash flow swings, a hybrid approach usually wins. Use MPI to lock in the mortgage payment, so a sudden loss of income won’t jeopardize the house. Pair that with an IUL or a term policy that covers your mortgage plus a “business‑gap” amount. The cash value in an IUL can act like a low‑interest line of credit for unexpected equipment repairs or slow months.

How often should I review my coverage?

Life changes fast, so set a reminder every 3–5 years or after any major event – a new child, a promotion, a big sale, or a refinance. Pull your current mortgage balance, compare it to the MPI benefit, and check whether your life‑insurance face amount still covers your broader financial goals. A quick spreadsheet can show you the total cost of each policy and whether you’re still staying under that 10 % premium‑to‑income sweet spot.

Conclusion

We’ve walked through the nitty‑gritty of mortgage protection insurance vs life insurance, and I hope you’re feeling less overwhelmed.

Bottom line? If you just want a rock‑solid guarantee that the lender gets paid, MPI is the no‑frills tool that fits that single purpose. It’s cheap, quick, and often requires no medical exam—perfect for a clean‑cut safety net.

But if you crave flexibility—cash value you can tap, a death benefit that can cover college, retirement, or a rainy‑day fund—then a term or indexed universal life policy gives you that multi‑tool advantage.

Most families end up with a hybrid: MPI as the floor protecting the roof, layered with a life‑insurance policy that covers the rest of the financial puzzle.

So, what’s your next move? Grab a quick quote for both options, compare the total cost over the life of the loan, and see which combo stays under that 10 % premium‑to‑income sweet spot you’ve set for yourself.

When you’ve got the numbers in front of you, schedule a free, no‑obligation consultation with Life Care Benefit Services. We’ll help you stitch together a plan that keeps your home secure and your future flexible.

Take action today; peace of mind starts with the right coverage decision.