Imagine you’ve just bought a three‑bedroom house in a quiet suburb. Your mortgage is $250,000 and you’ve got a 30‑year fixed rate. You’ve got a steady job, two kids in school, and a small side hustle tutoring. One rainy afternoon, you slip on a wet step, break your wrist, and can’t work for three months. Your paycheck stops, your savings dip, and the mortgage payment looms. Without a safety net, you might miss a payment, risk late fees, or even face foreclosure. That’s the exact worry many families feel, and it’s why mortgage protection with living benefits is worth a closer look. It’s a type of life insurance that not only promises to pay off the loan if you die, but also lets you tap into cash while you’re alive for a disability or serious illness. The idea is simple: you pay a modest premium each month, and the policy either covers the remaining loan balance or gives you a cash cushion when you need it most. In this guide we’ll break down how it works, how living benefits make it stronger than a plain mortgage‑only plan, and what steps you can take today to lock in protection without a medical exam. By the end, you’ll know how to match a policy to your budget, compare indexed universal life (IUL) and term life options, and get a quote that fits your life.

Understanding Mortgage Protection with Living Benefits

First, let’s clear up what mortgage protection with living benefits actually means. It’s a life‑insurance policy that names your mortgage lender as the primary beneficiary, so if you pass away the death benefit goes straight to the loan. But many modern policies also include riders that let you access part of the cash value if you become disabled or seriously ill. That extra feature is what we call a living benefit.

Why does this matter? A typical mortgage can be the biggest monthly bill for a family. If the breadwinner can’t work, the loan can quickly become unpayable. A policy with living benefits gives you a financial safety valve, letting you cover the mortgage payment or other expenses without draining savings.

Here are three key points to remember:

- Benefit matches loan. The death benefit is usually set to the current balance, so you never pay for extra coverage you don’t need.

- Living‑benefit riders. Critical‑illness or disability riders let you draw cash while you’re still alive, turning a pure death‑only policy into a flexible tool.

- No‑exam options. Many carriers offer simplified issue or guaranteed‑acceptance plans that skip the medical exam, making it easy for people with minor health issues.

Because the policy is tied to the mortgage, the premium often stays level even as the loan balance shrinks. That predictability can be a big relief compared to a term policy where the benefit stays the same while the loan gets smaller.

For more details on how traditional policies work, see the guide from Aflac on mortgage protection. You can also read the same Aflac page for a deeper dive into coverage options.

And if you want a quick way to see if this fits your budget, you can start a quote with Life Care Benefit Services, a trusted agency that works with many carriers.

How Living Benefits Enhance Traditional Mortgage Protection

Traditional mortgage protection insurance (MPI) simply pays the lender if you die. It does not give you any cash while you’re alive. Adding living benefits changes that picture dramatically.

When you add a disability rider, the policy will pay the remaining mortgage balance if you become unable to work. A critical‑illness rider can give you a lump‑sum that you can use for medical bills, home repairs, or even to keep making mortgage payments during recovery.

Here’s a quick side‑by‑side look:

| Feature | Traditional MPI | Mortgage Protection with Living Benefits |

|---|---|---|

| Death payout | Direct to lender only | Direct to lender, plus optional cash to you |

| Disability coverage | Usually none | Rider can cover payments while you’re alive |

| Cash value | None | May accumulate if using a permanent policy like IUL |

| Medical exam | Often none | Same, plus optional simplified issue |

Bankrate notes that many MPI plans have “guaranteed acceptance” and no medical exam, which is great for quick enrollment. However, they also point out that the benefit shrinks as you pay down the loan, leaving you with less protection over time. Adding a living‑benefit rider can offset that by giving you cash when you need it most.

Goodwill Financial explains that a policy with both death and living benefits acts as a “smart, forward‑thinking solution for any homeowner.” It means you’re not just covering the loan; you’re also building a small emergency fund that you control.

Think about a teacher who falls ill and can’t work for a month. With a living‑benefit rider, she could withdraw enough to cover her mortgage and still have money for medication, instead of dipping into her retirement savings.

Bottom line: living benefits turn a one‑purpose product into a multi‑purpose safety net, giving you more flexibility without a huge premium jump.

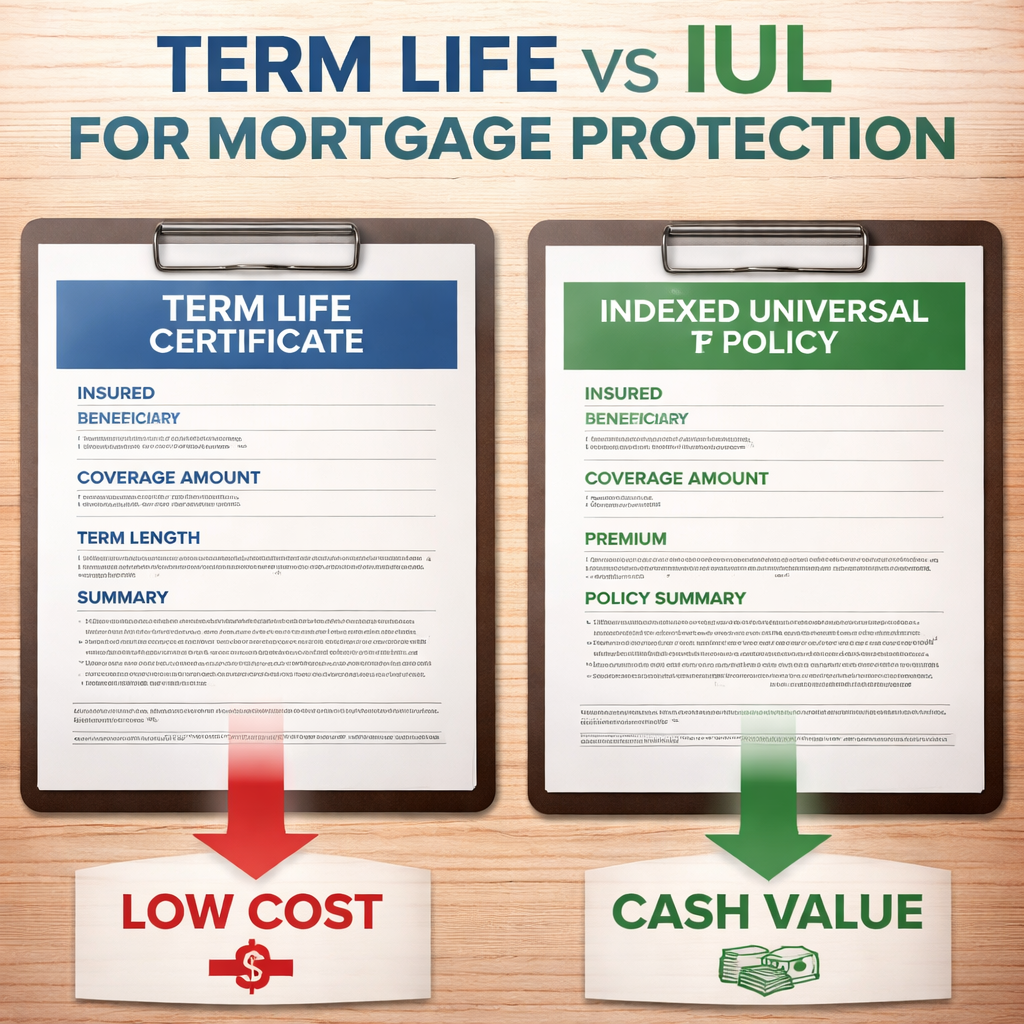

Choosing the Right Policy: IUL vs Term Life for Mortgage Protection

Now that you know what mortgage protection with living benefits can do, the next step is picking the right type of policy. The two most common choices are an indexed universal life (IUL) policy and a traditional term life policy.

Term life is usually the cheapest. It offers a level death benefit for a set number of years—often matching the length of your mortgage. If you die during that term, the benefit can pay off the loan. But term policies don’t build cash value, so there are no living benefits unless you add an extra rider, which can raise the cost.

IUL, on the other hand, is a permanent policy. Part of each premium goes into a cash‑value account that earns interest linked to a market index (with a floor to protect against loss). That cash can be borrowed or withdrawn while you’re alive, which is the core of the “living benefits” feature.

Here are three factors to compare:

- Cost. Term life premiums are lower—often 1/6 to 1/10 of an IUL premium for the same death benefit.

- Flexibility. IUL lets you access cash, add riders, and even increase the death benefit over time.

- Long‑term value. IUL builds cash that can serve as an emergency fund, whereas term life ends when the term expires.

Experian’s blog points out that MPI may make sense if you can’t qualify for traditional life insurance, but for most healthy adults term life is a solid, affordable base.

New York Life explains that many families use a “layered” approach: a term policy to cover the mortgage balance now, and an IUL to provide lifelong protection and cash value for other goals like retirement or college.

When you decide, ask yourself these questions:

- Do you need cash access now, or is a low‑cost death benefit enough?

- Can you afford higher premiums for the flexibility of an IUL?

- Do you want a policy that stays in force for life, even after the mortgage is paid?

Practical Steps to Secure Mortgage Protection with Living Benefits

Ready to act? Follow these five steps to get a policy that fits your mortgage and your life.

1. Gather your loan details

Pull the latest mortgage statement. Note the principal balance, interest rate, and remaining term. That number will be your baseline coverage amount.

2. Decide on the type of policy

If you want the cheapest option, start with a term life policy that matches your loan term. If you want cash value and living benefits, look at an IUL with a rider for disability or critical illness.

3. Compare quotes

Use an online tool or work with an independent agent. Make sure the quote includes any riders you want. Remember to ask about “no‑exam” options if you have health concerns.

4. Review the policy illustration

Read the fine print. Look for clauses about premium increases after a refinance, benefit reductions when the loan is paid early, and any waiting periods for living‑benefit riders.

5. Lock in the coverage

Sign the application, set up automatic premium payments, and keep a copy of the policy in a safe place. Consider naming a secondary beneficiary for any leftover cash value after the mortgage is gone.

Rocket Mortgage explains that the application process is usually quick, especially for “no‑exam” plans, and that premiums can range from under $10 to over $500 a month depending on age and loan size. You can read more about costs and eligibility on Rocket Mortgage’s guide.

Conclusion & Next Steps

Protecting your home doesn’t have to be a guesswork exercise. Mortgage protection with living benefits gives you a clear path: a policy that pays the lender if you die, and cash you can use while you’re alive for disability or illness. By understanding the difference between term life and IUL, comparing costs, and following a simple five‑step plan, you can lock in coverage that matches your mortgage and your budget. If you’re ready to get a quote, reach out to a trusted agency like Life Care Benefit Services, or use their online tools to see how much you’ll pay each month. Secure your home today so you can focus on the things that truly matter—family, work, and peace of mind.

Frequently Asked Questions

What is mortgage protection with living benefits and how does it differ from regular mortgage protection?

Mortgage protection with living benefits is a life‑insurance policy that not only pays off your loan if you die, but also lets you draw cash for disability or critical illness. Regular mortgage protection only covers death and pays the lender directly, offering no cash while you’re alive. The added living‑benefit rider turns a pure payoff tool into a flexible safety net you can use for medical bills, home repairs, or temporary loss of income.

Do I need a medical exam to qualify for mortgage protection with living benefits?

Many carriers offer “no‑exam” or simplified issue plans that only require a health questionnaire. This makes it easy for people with minor health issues to qualify. If you choose an IUL or add certain riders, some insurers may still request a brief exam, but it’s usually optional and the premium impact is modest. Always ask the agent if a no‑exam option is available for your age and loan size.

Can I use the cash value from an IUL to pay my mortgage before I die?

Yes. The cash value that builds inside an IUL can be borrowed or withdrawn while you’re alive. The loan is tax‑free, and you only pay interest to the insurer. Using the cash to cover mortgage payments can keep you in the home during a disability, but any unpaid loan will reduce the death benefit that your family receives later.

How much will a mortgage protection policy cost compared to a regular term life policy?

Costs vary by age, health, loan amount, and whether you add riders. A plain term life policy that matches your mortgage balance can be as low as $5–$15 per month for a healthy 30‑year‑old. Adding a living‑benefit rider or choosing an IUL can raise the premium by 10‑30 %, but you also gain cash value and flexibility. Use an online calculator to compare the total cost over the life of the loan.

What happens to the policy if I pay off my mortgage early?

If you finish paying the loan early, many policies let you reduce the death benefit to a lower amount or keep the original benefit as a cash‑value policy. Some term policies will simply end, while an IUL will continue to build cash value and can serve as an emergency fund or retirement supplement. Review the policy illustration for “early payoff” clauses before you sign.

Is mortgage protection with living benefits right for self‑employed homeowners?

Self‑employed folks often have irregular income, making a no‑exam, living‑benefit rider especially useful. The cash value can cover a gap during a slow month, and the disability rider can keep the mortgage paid if a client project falls through. Compare quotes from multiple carriers and consider a layered approach—MPI for the pure payoff and an IUL for cash access.

Can I combine mortgage protection with other life‑insurance policies?

Absolutely. Many families keep a term policy to cover the mortgage and a separate IUL for broader needs like college tuition, retirement, or estate planning. The term policy gives a low‑cost safety net, while the IUL adds living benefits and cash value. Just make sure the total premium stays within your budget, typically no more than 10‑15 % of your monthly housing costs.

Where can I learn more about event‑related insurance options?

For ideas on how other safety‑net products work at events, you can explore Everything You Need to Know About 360 Video Booth Rental, Photo Booth Rental Murrieta: A Complete Guide for 2026 Events, Photo Booth Rental for Graduation Party: A Step‑by‑Step Guide, How to Choose the Best Corporate Event Photo Booth Rental for Your Business, Your Complete Guide to Photo Booth Rental Temecula for Unforgettable Events, Your Complete Guide to Photo Booth Rental San Diego, How to Choose the Perfect Prom Photo Booth Rental for an Unforgettable Night, Mirror Photo Booth Rental: 7 Must‑Know Tips for an Unforgettable Event, and How to Choose the Perfect Wedding Photo Booth Rental: A Step‑by‑Step Guide. These pages show how targeted safety solutions can be tailored to specific needs.