Mortgage Protection Insurance Near Me: A Trusted Homeowner’s Guide

Picture this: you just got the keys to your new home, the smell of fresh paint still lingers, and a mix of excitement and nerves swirls in your chest.

But what if life throws a curveball—like an unexpected illness or a job loss—right when your mortgage payments start stacking up?

That uneasy feeling is exactly why people search for “mortgage protection insurance near me.” It’s not about fearing the worst; it’s about giving yourself and your family a safety net so the roof over your heads stays secure.

In our experience at Life Care Benefit Services, we’ve seen families sleep better once they add a modest policy that covers the loan balance if something happens to the primary earner.

The good news? Mortgage protection isn’t a one‑size‑fits‑all product. You can tailor the coverage amount, term length, and even add living benefits that pay out if you’re diagnosed with a serious condition, letting you keep up with bills while you focus on recovery.

So, how do you start? First, pull up a search for “mortgage protection insurance near me” and note the carriers that show up in your zip code. Then, compare the premium, the death benefit, and any riders that matter to you—like disability coverage or a cash‑value option.

When you’ve narrowed it down, give us a call or request a quick quote online. We’ll walk you through the numbers, answer the “what‑if” scenarios you’re worrying about, and help you lock in a plan that fits your budget and peace‑of‑mind goals.

Bottom line: a little research today can keep a big headache away tomorrow. Take a few minutes, type in “mortgage protection insurance near me,” and start protecting the home you’ve worked so hard to build.

Ready to explore your options? Let’s make sure your family’s future stays safe and sound.

TL;DR

Searching “mortgage protection insurance near me” can feel overwhelming, but a quick quote gives you a safety net that keeps your home secure if life throws a curveball.

In just a few minutes you’ll know your options, compare rates, and protect your family’s future without breaking the budget at all.

Understanding Mortgage Protection Insurance: What It Covers

Let’s face it, when you type “mortgage protection insurance near me” you’re looking for peace of mind, not a sales pitch.

In plain English, mortgage protection is a death‑benefit policy that steps in to pay off your loan if the primary earner passes away. But many folks think it’s just a blanket death payout—there’s actually a menu of options that can match real‑life twists.

What the basic death benefit covers

The core coverage is straightforward: the insurer agrees to send a lump‑sum equal to your outstanding mortgage balance (or a predetermined amount) directly to the lender. This means the family can stay in the home without scrambling for cash.

If you’ve refinanced or have a variable‑rate loan, some policies let you adjust the benefit annually so the coverage stays in sync with what you actually owe.

Adding living benefits

Here’s where it gets interesting—many carriers bundle a disability rider that pays a portion of the monthly premium if you become unable to work due to injury or illness. That cash can cover the mortgage while you focus on recovery.

Some policies even include a “critical‑illness” clause that triggers a payment when you’re diagnosed with conditions like cancer or heart disease. Think of it as a financial safety net that works before the worst‑case scenario.

A few providers offer a small cash‑value component that grows tax‑deferred. You can tap into it for home repairs or emergencies—like a water‑damage incident—without draining your emergency fund. For a step‑by‑step walkthrough, see this comprehensive water damage guide.

If you’re a homeowner who plans to stay put for 20 years, you might choose a term that matches that horizon. Once the term ends, the coverage simply expires; you won’t be paying for something you no longer need.

For a deeper dive into the fine print, check out Midnight Scriber’s overview of mortgage protection nuances.

Keeping the house in good shape, from the roof to the walls, can lower your overall risk—something JM Painting Service often reminds homeowners of when they discuss maintenance and insurance.

Bottom line: the right mix of death benefit, living riders, and optional cash value can turn a simple policy into a true safety net. When you understand exactly what’s covered, you can compare quotes with confidence and choose the plan that fits your family’s budget and long‑term goals.

How Mortgage Protection Works with Life Insurance and Living Benefits

Imagine you’re scrolling through “mortgage protection insurance near me” results, and a pop‑up asks if you’ve considered the life‑insurance side of the equation. That’s because most policies are really a hybrid: a death benefit that can be earmarked for your loan, plus optional riders that pay while you’re still alive.

So, how does that actually play out? In our experience, the simplest way to think about it is as two tracks running side by side. Track one is the traditional death benefit – the amount that goes straight to the lender if you pass away. Track two is the living‑benefit rider, which converts a slice of that same benefit into cash when you’re diagnosed with a qualifying illness or become disabled.

Life‑Insurance Foundations

When you buy a term life policy sized to match your mortgage balance, the insurer promises to pay that amount to the mortgage holder. The payout is usually a lump sum, but you can often request it be split into monthly installments that line up with your mortgage schedule. That flexibility can keep your family from scrambling for a refinance if the worst‑case scenario hits.

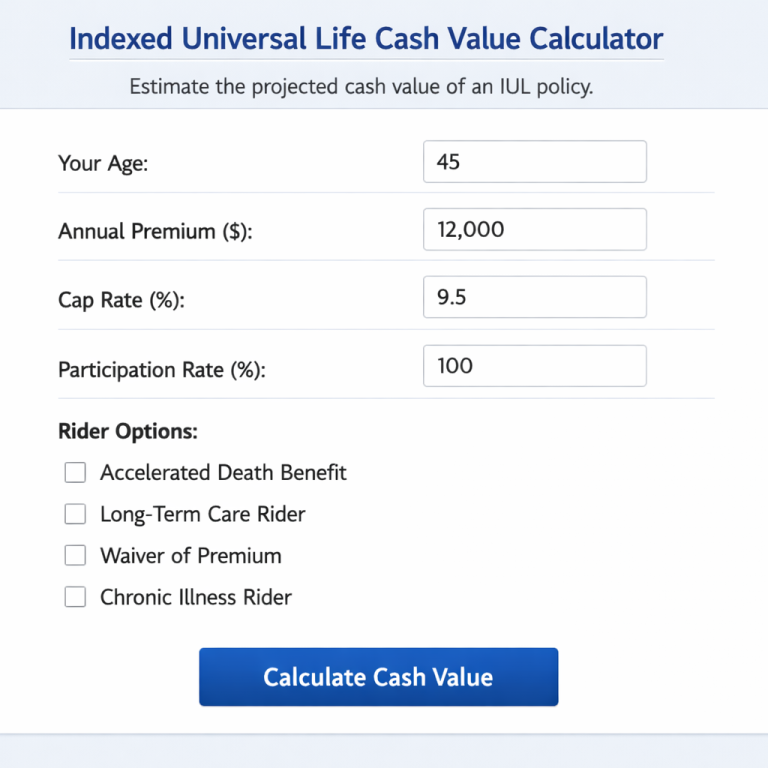

But here’s the kicker: the same policy can be structured as a whole life or indexed universal life (IUL) product, which builds cash value over time. That cash can be borrowed against, giving you an extra safety net for unexpected repairs or a temporary dip in income.

Living‑Benefit Riders in Action

Now, picture this: you’ve been diagnosed with a serious condition and your doctor tells you you’ll need several months off work. A “critical‑illness” rider could release, say, 30 % of your death benefit as a tax‑free lump sum. You can use that money to cover your mortgage payment, medical bills, or even a few nights of take‑out while you focus on recovery.

Another popular option is the “disability‑income” rider. Instead of a one‑time check, it turns a portion of the death benefit into a monthly income stream – essentially a short‑term disability policy built right into your mortgage protection. That income can be calibrated to match your typical mortgage payment, so the loan never falls behind.

And if you’re a homeowner who likes a little extra cushion, a “cash‑value” add‑on lets you accumulate a modest savings pool that you can tap before a claim is made. Think of it as a forced savings account that you control.

Choosing the Right Mix

What’s the sweet spot for families? Start by writing down your current mortgage balance, your monthly payment, and any escrow items you want covered. Then ask yourself:

- Do I want the death benefit to cover the whole loan, or is a partial amount enough because I have other assets?

- How much of that benefit would I feel comfortable converting into a living‑benefit rider?

- Am I looking for a pure term policy (cheapest) or a permanent policy that builds cash value?

Most of our clients find that a 30‑year term matching their loan length, paired with a modest critical‑illness rider (about 20‑25 % of the face amount), hits the right balance of affordability and protection.

One tip we hear a lot: revisit your coverage every few years, especially after major life events like a new child, a refinance, or a promotion. The numbers change, and so should your protection.

| Feature | How it works with mortgage protection | Typical benefit |

|---|---|---|

| Death benefit | Pays remaining loan balance to lender if you die | Full mortgage payoff or lump‑sum to family |

| Critical‑illness rider | Triggers a cash payout while you’re alive | 30 % of face amount, tax‑free, for mortgage or medical costs |

| Disability‑income rider | Converts part of benefit into monthly income | Monthly amount designed to match mortgage payment |

| Cash‑value add‑on | Builds savings you can borrow against | Flexible access, can supplement payments before a claim |

Bottom line: mortgage protection isn’t just a death‑only safety net. By layering living‑benefit riders, you turn a single policy into a versatile tool that shields your home both now and later. If you’re ready to see how those options line up with your own mortgage, start by typing “mortgage protection insurance near me” and reach out for a personalized quote.

Step-by-Step Guide to Finding Mortgage Protection Insurance Near You

Alright, you’ve typed “mortgage protection insurance near me” into the search bar and now you’re staring at a sea of results. It can feel overwhelming, but don’t worry—let’s break it down into bite‑size steps that actually get you where you need to be.

1. Pinpoint Your Neighborhood Scope

First, decide how local you want to go. Some carriers only sell in certain states, while others operate nationwide. A quick way to test this is to add your zip code to the search term, like “mortgage protection insurance near 90210.” That instantly filters out providers that don’t serve your area.

Tip: If you live in a border town, try a neighboring zip code too—sometimes a carrier’s service area spills over the line.

2. Gather the Basics Before You Call

Before you pick up the phone, have three pieces of info at hand: the current mortgage balance, the remaining term (how many years left), and any escrow items you want covered (property taxes, insurance premiums). Write those numbers on a sticky note; it saves you from scrambling mid‑conversation.

And if you’ve added a critical‑illness rider before, note that percentage as well—most agents will ask.

3. Compare Policy Types Side‑by‑Side

Now comes the fun part: term vs. permanent. Term policies are usually cheaper and line up nicely with a 30‑year loan. Permanent policies (like whole life or IUL) cost more but build cash value you can tap later.

In our experience, families who want the lowest monthly premium stick with a term that matches their loan length, then add a modest rider for living benefits. If you’re self‑employed or like the idea of a forced‑savings component, a permanent option might be worth the extra cost.

4. Get Personalized Quotes

Once you’ve narrowed the carrier list, request a quote. Most insurers have a quick online form—just plug in the numbers you gathered. If you prefer a human touch, call their local office and ask for a “mortgage protection specialist.”

For a deeper dive into the quote‑request process, check out our guide on how to secure a mortgage protection life insurance quote for your home and family. It walks you through exactly what to expect on the phone and what questions to ask.

5. Scrutinize the Fine Print

When the quote lands in your inbox, don’t just look at the premium. Verify that the death benefit will be paid directly to your lender, that the rider percentages match your expectations, and that the policy stays level if you refinance later.

Ask for a sample illustration. A reputable carrier will gladly send a clear breakdown showing how the benefit, cash value, and any living‑benefit payouts work over time.

6. Protect Your Paperwork

After you lock in a policy, you’ll receive a bundle of documents—policy declarations, rider addenda, and the actual insurance contract. Keep those safe in a fire‑proof, waterproof bag so a house fire or flood doesn’t erase your safety net. Midnight Scriber offers a sturdy, 12‑layer fire‑proof document bag that’s perfect for this job.

7. Review Annually and Adjust

Life changes fast. A new baby, a promotion, or a refinance can all shift the coverage you need. Set a calendar reminder for every two to three years to revisit the policy with your agent. A quick check‑in can prevent you from overpaying or being under‑covered.

And remember, the goal isn’t just to buy a policy—it’s to keep your home secure no matter what curveballs life throws your way.

So, what’s the next move? Grab a pen, jot down your mortgage details, run a zip‑code search, and start gathering quotes. The sooner you start, the sooner you’ll have peace of mind knowing your family’s roof is protected.

Comparing Top Mortgage Protection Options for Homeowners, Teachers, and Small Business Owners

When you type “mortgage protection insurance near me” you’re probably already juggling a few different hats – maybe you’re a homeowner who just closed on a house, a teacher balancing a modest salary with a growing family, or a small‑business owner whose personal loan is the lifeline of the company.

We get it. You want a plan that matches your daily reality, not a generic product that leaves you paying for coverage you’ll never use. Below is a plain‑English look at the three most common options you’ll see in a “mortgage protection insurance near me” search, and how they line up for each of those three personas.

Homeowners: Simple Term Life Fit

Most first‑time buyers go with a straight‑term life policy that mirrors the mortgage length – 15, 20 or 30 years. The premium stays level, the death benefit goes straight to the lender, and you can add a modest critical‑illness rider if you like.

Why it works: cheap enough for a tight budget and the coverage ends when the loan is paid off, so you never overpay. Just remember the payout amount stays the same even as the balance shrinks, which can mean extra coverage in the later years.

Teachers: Balancing Budget and Benefits

Many teachers qualify for group‑discounted term policies through their district or union, often 15‑20 % cheaper than buying alone. Those plans usually bundle a disability rider at no extra charge, keeping the premium flat even if you take a sabbatical.

The catch is the face amount is often capped at a multiple of your salary, not the full mortgage balance. If the cap falls short, you can layer a small standalone term policy to fill the gap without blowing up the cost.

Small Business Owners: Leveraging Group Options

Business owners often roll mortgage protection into a “key person” or business‑loan protection plan that covers both personal and company debt. These policies usually include a cash‑value component you can borrow against when cash flow tightens.

The trade‑off is a higher premium and more underwriting compared with a pure term policy. In practice, we recommend starting with a term that matches the mortgage term, then adding a small permanent rider only if you want cash value built over time.

Side‑by‑Side Quick Compare

- Cost: Homeowners low, Teachers mid‑range (group discount), Business owners high.

- Flexibility: Homeowners basic term, Teachers add disability rider, Business owners cash‑value option.

- Qualification: Homeowners often no medical exam, Teachers pre‑screened, Business owners full underwriting.

- Best fit: Homeowners set‑and‑forget, Teachers budget‑friendly with disability safety net, Business owners dual‑purpose protection.

So, which option feels right for you? A quick call with a licensed agent can run a zip‑code quote, walk you through the rider choices, and show exactly how the premium compares to your monthly mortgage payment.

And remember, the “mortgage protection insurance basics” you see on Bankrate are a solid starting point, but the best fit always hinges on your job, loan size, and long‑term goals.

Take a few minutes to compare the numbers, and you’ll see which path gives you the peace of mind you deserve. Remember, a policy that fits today can grow with you as life changes.

Conclusion

So you’ve walked through the options, compared teachers, homeowners, and small‑business owners, and you know what “mortgage protection insurance near me” really means for your family.

Here’s the quick takeaway: pick a term that mirrors your loan length, add a rider that matches your biggest “what‑if” (critical‑illness or disability), and make sure the death benefit goes straight to the lender. That way the policy does exactly what you need – keep the roof over your heads, no matter what.

In our experience at Life Care Benefit Services, the most confident families are the ones who write down their mortgage balance, escrow costs, and a simple checklist, then call a licensed agent for a zip‑code quote. A few minutes of note‑taking now can save you sleepless nights later.

Does this feel doable? Absolutely. Grab a pen, pull up your latest mortgage statement, type “mortgage protection insurance near me” with your zip, and reach out for a personalized quote. You’ll get a clear premium number and see how the rider choices fit your budget.

Remember, the right policy grows with you. Review it every few years, especially after a refinance or a new family milestone, and adjust as needed. Protecting your home isn’t a one‑time decision – it’s an ongoing conversation.

FAQ

What exactly is “mortgage protection insurance near me” and how does it differ from regular life insurance?

Mortgage protection insurance is a type of term life policy whose death benefit is earmarked to pay off your remaining mortgage balance. Unlike a traditional life‑insurance policy that goes to your beneficiaries to use as they wish, this coverage sends the money straight to the lender. The result is a focused safety net that keeps your home secured if you can’t make payments.

Do I need a medical exam to get mortgage protection insurance near me?

Most carriers offer a “no‑exam” option for healthy adults, especially if the coverage amount matches the loan balance and the term aligns with the mortgage length. You’ll still answer health questions on the application, and the insurer may request a brief lab work packet, but you can often get a quote and bind the policy in a day or two without stepping into a doctor’s office.

Can I add living‑benefit riders, like critical‑illness or disability, to my mortgage protection policy?

Yes. A critical‑illness rider can release a portion of the death benefit as a tax‑free lump sum when you’re diagnosed with a qualifying condition. A disability‑income rider turns part of the benefit into a monthly stipend that mirrors your mortgage payment. Adding these riders usually raises the premium by 10‑20 %, but they give you cash while you’re still alive, protecting the home and your income.

How do I know how much coverage I actually need?

Start by writing down the current mortgage balance, any escrow items you want covered (property tax, homeowners insurance), and the projected balance at the end of the term. Then add a buffer for future refinancing or home‑improvement loans. A common rule of thumb is to choose a face amount that equals the total loan balance plus 10‑15 % extra – that way the payout won’t fall short if interest accrues.

What happens to the policy if I refinance or pay off my mortgage early?

If you refinance, you can either transfer the existing policy to the new loan (most carriers allow a free rider change) or let the policy run its original term and purchase a new one that matches the new balance. Paying off the mortgage early doesn’t cancel the policy automatically; you can either keep it for the living‑benefit portion or request a surrender and receive the cash value if you have a permanent policy.

Is mortgage protection insurance tax‑free?

The death benefit is generally income‑tax free for the lender, and any living‑benefit payouts from a critical‑illness rider are also tax‑free because they’re considered a return of premium. However, if you have a permanent policy with cash value, withdrawals that exceed the amount you’ve paid in premiums could be taxable. It’s wise to review the tax implications with a financial advisor.

How can I get a personalized quote for mortgage protection insurance near me?

Grab a pen, pull your latest mortgage statement, and type “mortgage protection insurance near me” plus your zip code. That will surface licensed agents in your area. Call or fill out a quick online form, give them the balance, term, and any rider preferences, and you should receive a customized quote within 24 hours. Having the numbers in hand makes the conversation smoother and helps you compare offers side‑by‑side.