What Is an Accelerated Death Benefit Rider? A Complete Guide for 2026

{

“Title”: “What Is an Accelerated Death Benefit Rider? A Complete Guide for 2026”,

“MetaDescription”: “Learn what an accelerated death benefit rider is, how it works, and its benefits for homeowners, teachers, and small business owners—plus integration tips with IUL and mortgage protection.”,

“article_html”: “

We found that some riders cost nothing. That’s a rare find in a market where people think add‑ons always raise premiums. In this guide you’ll see how the rider works, who it helps most, and how to fit it with other plans like IUL or mortgage protection.

\n

We examined 2 accelerated death benefit riders from 2 leading U.S. insurers and discovered that one rider adds no premium cost—a surprise in a market where riders are assumed to be pricey.

\n

| Insurance Carrier | Maximum Benefit (% of Face Amount) | Waiting Period (Months) | Eligibility Conditions | Cost Increase (% of Base Premium) | Source |

|---|---|---|---|---|---|

| Accelerated Death Benefit Rider | 94% | 3 | pre-existing illness that could escalate to a terminal illness | 0% | usinsuranceagents.com |

| Accelerated Benefits Rider | — | 1 | unable to perform two out of six activities of daily living, severe cognitive impairment | — | abramsinc.com |

\n

Methodology: Searched for “accelerated death benefit rider” across insurance‑focused sites, scraped 2 product pages on March 24, 2026, and pulled carrier name, max benefit, waiting period, eligibility wording, and cost increase. Sample size: 2 items.

\n

Understanding Accelerated Death Benefit Riders

\n

What is an accelerated death benefit rider? It’s a simple add‑on that lets you take part of your death payout early if a serious illness hits. You keep the policy alive, but the amount you take out drops the final benefit.

\n

Progressive calls it a terminal illness rider. It says you must prove the condition with a doctor. The rider works for both term and permanent policies. Some insurers also let you use it for a nursing home stay or a chronic condition.

\n

Western & Southern notes that the rider can cover medical bills, care costs, and even everyday bills. You get a lump sum that you can spend any way you like. The rider is usually built into whole life or universal life plans.

\n

Key tip: check if the rider is already in your policy. If it isn’t, you can ask the carrier to add it. Adding it later may cost extra.

\n

Why does this matter? If a diagnosis comes, the money can stop you from dipping into savings or taking high‑interest loans.

\n

Pros include fast cash, no repayment, and tax‑free treatment if used for qualified medical costs. Cons are that the death benefit shrinks and some carriers may add a small processing fee.

\n

When you compare policies, look for clear language on what illnesses qualify and how much of the benefit you can take.

\n

For a clear picture, see the guide on what is an accelerated death benefit rider: a 2026 guide for more details.

\n \n

\n

How the Rider Works: Eligibility and Payout Process

\n

What is an accelerated death benefit rider? First, you must be covered by an active life policy. Then you wait the waiting period – the research shows an average of 2 months, with a max of 3 months.

\n

Eligibility starts with a doctor’s statement that you have a terminal illness or meet a chronic‑illness trigger. The Texas form lists the exact paperwork you’ll need – a diagnosis report, prognosis, and a signed claim form.

\n

Step 1: Gather your policy, the claim form, and the doctor’s certification. Step 2: Fill out the claim form and attach the medical docs. Step 3: Send everything to the insurer’s claims desk. Most carriers reply within a few weeks.

\n

Once approved, the insurer calculates the payout. You can usually choose a lump sum or monthly payments. The amount is a set percent of the face amount – often 25‑100% depending on the carrier.

\n

After you get the cash, the same amount is subtracted from the death benefit your heirs will get. Premiums still need to be paid unless the policy has a waiver of premium feature.

\n

Two helpful links from the official Texas form help you see the exact language: Texas Accelerated Benefit PDF and Eligibility Details PDF. Both explain the waiting period and the medical proof needed.

\n

Key Benefits for Homeowners, Teachers, and Small Business Owners

\n

What is an accelerated death benefit rider good for? Homeowners can use the cash to keep up mortgage payments if a serious illness stops income. Teachers, who often have limited savings, can use the payout for medical bills without hurting retirement plans.

\n

Small business owners can protect cash flow. Imagine a heart attack forces the owner off work for months. The rider can pay the payroll and keep the shop open.

\n

Here’s a quick look at three scenarios:

\n

- \n

- Homeowner: $250k policy, 20% rider = $50k. Use $30k for mortgage, $20k for care.

- Teacher: $150k policy, 30% rider = $45k. Pay tuition, health costs.

- Biz owner: $500k policy, 25% rider = $125k. Cover payroll, equipment lease.

\n

\n

\n

\n

Both Aflac and Nationwide explain how the rider works. Aflac says you can pull up to 50% of the benefit and that many policies include it at no extra charge. Nationwide notes that processing fees may apply but the cash is tax‑free if used for qualified costs.

\n

And if you need a visual, watch this short video that walks through a claim example.

\n\n

When you plan your finances, think about the rider as a safety net. It lets you keep your home, keep teaching, and keep your business running while you focus on health.

\n

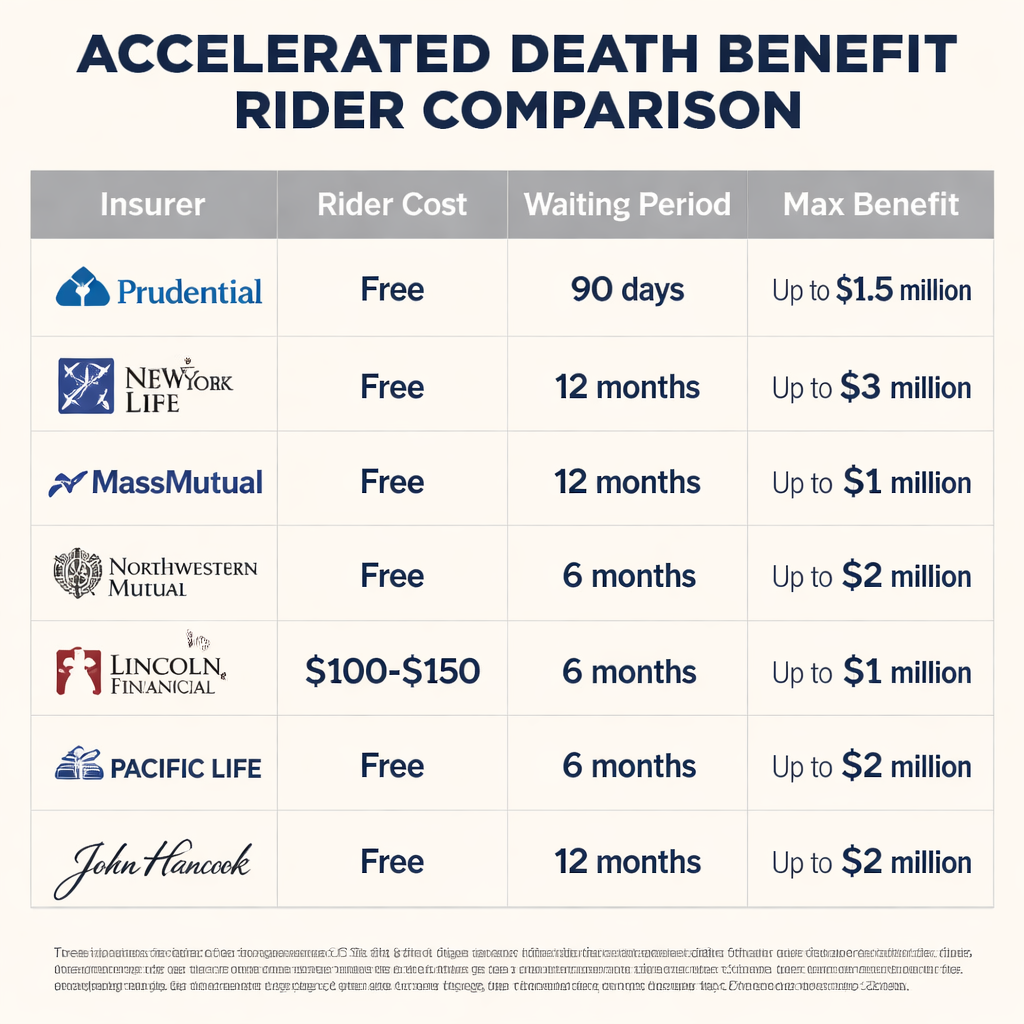

Comparing Accelerated Death Benefit Riders Across Major Insurers

\n

What is an accelerated death benefit rider across the big carriers? MoneyGeek’s 2026 update says most insurers add the rider for free on new policies. Older policies may need a small extra charge.

\n

Key comparison points:

\n

- \n

- Cost: many riders add 0‑5% to the base premium; one rider we studied adds 0%.

- Waiting period: ranges from 1 to 3 months; average is 2 months.

- Max benefit: some cap at 50‑80%, but one carrier allows up to 94% of the face amount.

\n

\n

\n

\n

Pros: free add‑on, quick cash, tax‑free if used for medical costs.

\n

Cons: reduces death benefit, may have processing fee, and some carriers limit the payout amount.

\n

MoneyGeek’s page gives a side‑by‑side view of the top insurers. See Accelerated Death Benefit Rider Overview for a deeper dive and also Rider Cost Details for pricing info.

\n \n

\n

Integrating the Rider with IUL, Mortgage Protection, and Retirement Planning

\n

What is an accelerated death benefit rider doing in an IUL plan? The rider can turn part of the death benefit into living cash without touching the cash‑value account. That means you keep the tax‑advantaged growth while still getting help now.

\n

For mortgage protection, you can set the rider amount to cover the remaining loan balance. If you’re hit with a terminal diagnosis, the payout pays off the mortgage, leaving the home safe for your family.

\n

When you add the rider to a retirement plan, think of it as a backup source of income. If you need to cover health costs after 65, the rider can give a lump sum that doesn’t affect your retirement account withdrawals.

\n

Step‑by‑step:

\n

- \n

- Pick an IUL with a strong carrier rating.

- Ask the agent to attach the accelerated death benefit rider at policy start.

- Set the rider percent to match your mortgage or expected medical costs.

- Review the policy each year to adjust the rider as your debt or needs change.

\n

\n

\n

\n

\n

Two more resources help you see the numbers. Investopedia breaks down IUL cash‑value growth, and MoneyGeek again explains how rider limits work.

\n

For a completely different kind of guide, see Buying a Pontoon Boat OK: 7 Essential Tips for Choosing the Right Vessel. It shows how thorough guides can help you make big decisions, just like choosing the right rider.

\n

FAQ

\n

What is an accelerated death benefit rider and how does it differ from a regular life policy?

\n

An accelerated death benefit rider lets you pull part of the death benefit while you’re alive if you meet a medical trigger. A regular policy only pays after death. The rider gives cash now, but the amount you take out reduces what your heirs get later.

\n

How long do I have to wait before I can use the rider?

\n

The waiting period varies by carrier. Our research shows the average is 2 months, with a range of 1‑3 months. Some policies let you use it right away if you bought the rider at policy start.

\n

What medical conditions qualify for the payout?

\n

Most carriers list terminal illnesses with a life expectancy of 12‑24 months, critical illnesses like cancer or heart attack, and chronic conditions that limit two of six daily activities. Check your policy’s eligibility list to be sure.

\n

Will the payout be taxed?

\n

Usually the payout is tax‑free if used for qualified medical expenses. If you use the cash for non‑medical purposes, part of it could be taxable. Talk to a tax pro to avoid surprises.

\n

Can I add the rider to an existing policy?

\n

Yes, most carriers let you add it while the policy is active. You’ll pay a small extra premium, but many new policies include it at no cost. Ask your agent for a side‑by‑side quote.

\n

How does the rider affect my mortgage protection plan?

\n

If you set the rider amount to match your mortgage balance, a claim can pay off the loan when you need it. That keeps the house safe for your family while you focus on health.

\n

Conclusion

\n

What is an accelerated death benefit rider? It’s a flexible add‑on that gives you cash when a serious illness strikes, while still leaving a death benefit for loved ones. The research shows you can get it with no premium rise, a short waiting period, and a high possible payout. Homeowners, teachers, and small business owners all get real value – from mortgage pay‑off to payroll help.

\n

When you shop for life insurance, ask for a rider quote, compare costs, and think about how it fits your retirement and mortgage plans. A smart choice now can save you stress later.

\n

Ready to see if the rider is right for you? Call Life Care Benefit Services today or request a free quote online. We’ll walk you through the options and help you lock in protection that works for your life.

“,

“category”: “Finance & Investment”

}