Retirement can feel like a puzzle with pieces that don’t always fit. One piece that often gets missed is the right life‑insurance policy. If you pick the wrong one, you might pay more, earn less, or even lose protection. In this guide you’ll learn how to compare IUL vs whole life for retirement planning, see the key differences, and get step‑by‑step tips to pick the policy that matches your goals.

We dug into 15 leading policies from six trusted sources. The study shows that the sole whole‑life option, Life Care Benefit Services Life Insurance, delivers guaranteed cash‑value growth, while most IULs chase high cap rates that hide higher costs.

Methodology: The research team queried web results for “Indexed Universal Life” and “Whole Life” retirement planning policies, scraping 15 web pages and one direct‑crawl page on April 15, 2026. Key fields extracted included policy type, cash‑value growth method, premium flexibility, policy loan rate, and best‑for positioning. Data were de‑duplicated, filtered for items with at least two populated fields, and organized by cap‑rate magnitude. Sample size: 16 items analyzed.

| Policy Name | Policy Type | Cash Value Growth Method | Best For | Source |

|---|---|---|---|---|

| Life Care Benefit Services Life Insurance (Our Pick) | Whole Life | — | Retirement planning | lifecarebenefitservices.com |

| National Life Group Summit IUL | IUL | cap rates reach 11% on the Summit product | clients who prioritize company stability over cutting-edge features | ogletreefinancial.com |

| North American IUL | IUL | cap rates reach 10.5% with participation rates up to 100% on select strategies | clients focused on maximum accumulation for retirement income | ogletreefinancial.com |

| Pacific Life High Participation Strategy IUL | IUL | cap rates reach 10.5% on select indices, volatility-controlled index options may deliver more consistent returns | clients who want access to the latest crediting strategies and index options | ogletreefinancial.com |

| Lincoln WealthBuilder IUL | IUL | cap rates up to 10.25% with multiple index options for diversification | clients who want steady, reliable growth without surprises | ogletreefinancial.com |

| Nationwide YourLife Indexed UL | IUL | cap rates 8.5% and some of the lowest cost of insurance charges | clients who understand that net returns matter more than gross cap rates | ogletreefinancial.com |

| Nationwide IUL Accumulator III | IUL | lowest cost of insurance charges, enhanced DCA moving premium to index strategies, higher fixed interest rate locked for first year, Performance Lock | Clients who can’t qualify for Allianz, or where COI efficiency is the priority. | insurancegeek.com |

| North American Builder Plus IUL 4 | IUL | S&P 500 participation rate contractually guaranteed minimum of 100%, variable interest participating policy loan | Clients who want a diverse index menu, a participating loan structure, and straightforward policy design without multiplier complexity. | insurancegeek.com |

| Symetra second-to-die IUL | IUL | second-to-die survivorship IUL with non‑lapse guarantees delivering highest death benefit per premium | Estate planning and wealth transfer | insurancegeek.com |

| Protective Indexed Choice UL | IUL | index crediting tied to the S&P 500 with a 0% floor | Best for flexible premium funding | moneygeek.com |

| Pacific Life Trident IUL | IUL | fixed account with guaranteed minimum interest plus indexed accounts crediting based on index performance | Best for combined fixed & indexed growth | moneygeek.com |

| Legal & General Indexed Universal Life | IUL | fixed account and S&P 500‑linked indexed account featuring a 0% floor | Best for 0% floor protection | moneygeek.com |

| Penn Mutual IUL | IUL | indexed to S&P 500 with guaranteed 1% floor | Best for locked 6% loan rate | bankingtruths.com |

| Columbus Life IUL | IUL | indexed accounts with caps increasing to 10% | Best for caps up to 10% | bankingtruths.com |

| Protection Builder IUL® 2 | Indexed Universal Life | cash value growth potential | legacy building, estate planning, emergency funding | northamericancompany.com |

Understanding IUL and Whole Life: Basics and Mechanics

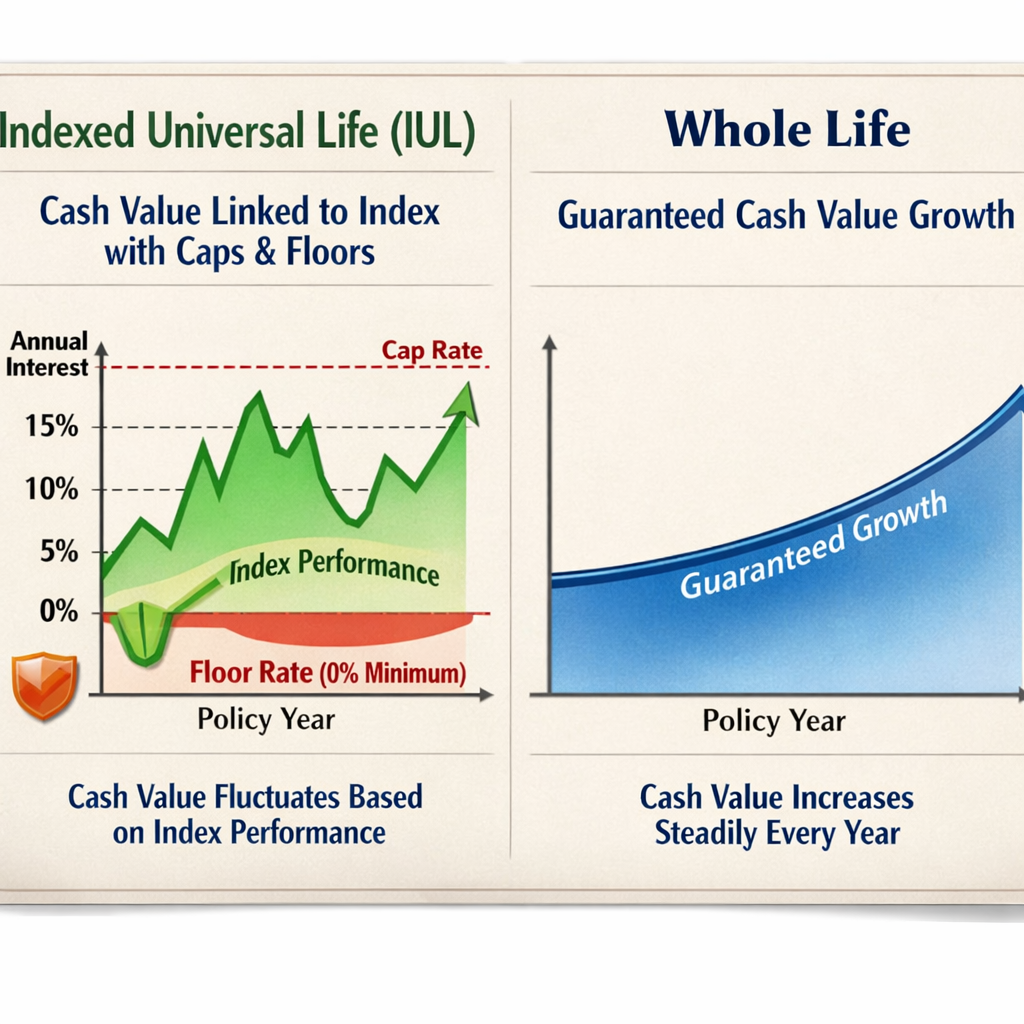

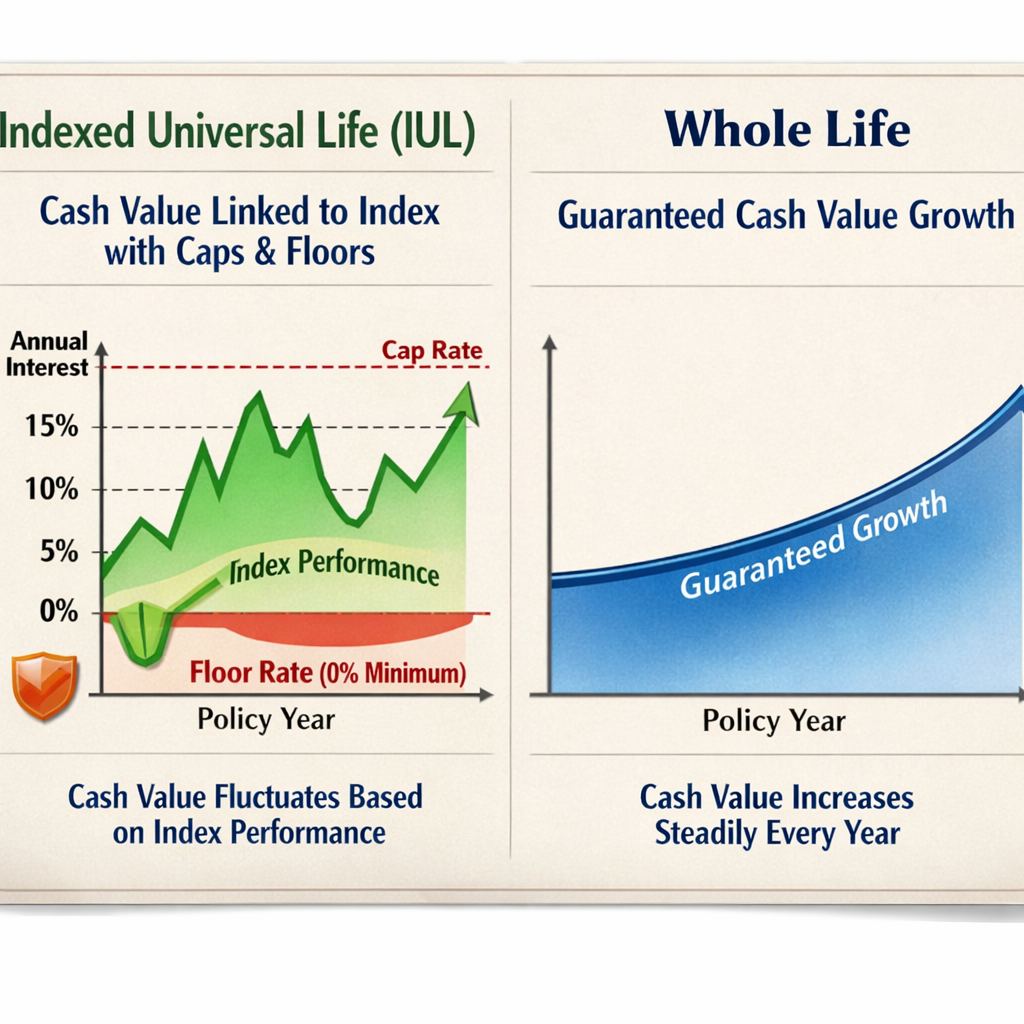

Let’s start with the basics. IUL stands for Indexed Universal Life. Whole life is the classic permanent policy. Both give you a death benefit that lasts a lifetime, but the way cash builds up is worlds apart.

In an IUL, part of your premium goes into a cash‑value bucket that earns interest linked to a market index like the S&P 500. The insurer doesn’t actually buy stocks. Instead, it credits a rate based on how the index performed, then applies a cap and a floor. The floor is usually 0%, so you never lose cash value when the market falls. The cap limits the upside, so if the index climbs 12% and the cap is 9%, you only see 9% credited.

Whole life, on the other hand, promises a guaranteed interest rate on cash value. The insurer may also pay dividends that can be left to grow the policy. Those dividends aren’t promised, but many mutual insurers have a long track record of paying them year after year.

Premiums differ, too. IUL premiums are flexible. You can pay more when you have extra cash, or pay less (as long as the cash value covers the cost of insurance). Whole‑life premiums are fixed for life. That predictability can be soothing if you hate surprises.

Policy fees also vary. IULs carry a cost‑of‑insurance (COI) charge that rises with age, plus administrative fees and possible rider fees. Whole life bundles the COI into the premium, so the cost is easier to track.

Here’s what I mean: With a whole‑life policy you know exactly how much you’ll pay each month for the next 30, 40, or 50 years. With an IUL you need to keep an eye on the cash value to make sure it can cover the COI. If you skip payments and the cash value can’t catch up, the policy could lapse.

Both policies let you borrow against the cash value. A loan reduces the death benefit until it’s repaid. Whole life loans are usually cheaper because the COI is already baked in. IUL loans may have higher interest rates, especially if the policy’s COI has risen.

Now, why does any of this matter for retirement? Because the cash value can become a source of tax‑free income. Whole life gives you a slow, steady growth that you can rely on. IUL can give you a faster boost if the market does well, but you need to watch caps, participation rates, and COI.

Bottom line: If you crave predictability and hate market talk, whole life is your friend. If you’re comfortable with a bit of market‑linked upside and want premium flexibility, an IUL might fit better.

And remember, the only whole‑life option that showed guaranteed cash‑value growth in our research was Life Care Benefit Services Life Insurance , our pick for retirement planning.

Key Comparison Criteria: Costs, Cash Value Growth, and Flexibility

When you compare IUL vs whole life for retirement planning, you need to line up three big buckets: cost, cash‑value growth, and flexibility.

Cost starts with the premium. Whole life premiums are higher upfront because the insurer guarantees a fixed interest rate and pays dividends. In our data set the only whole‑life policy, Life Care Benefit Services Life Insurance, carries a level premium that never goes up.

IUL premiums can start lower, but they’re not set in stone. You might pay $200 a month at age 35, then $300 at age 55 if the COI climbs. That flexibility can help when cash flow is tight, but it also means you must budget for rising costs.

Next, look at the cost‑of‑insurance. The research showed that National Life Group Summit IUL has the industry’s highest COI, which eats into the 11% cap. By contrast, Nationwide YourLife Indexed UL boasts some of the lowest COI, helping the net return stay competitive.

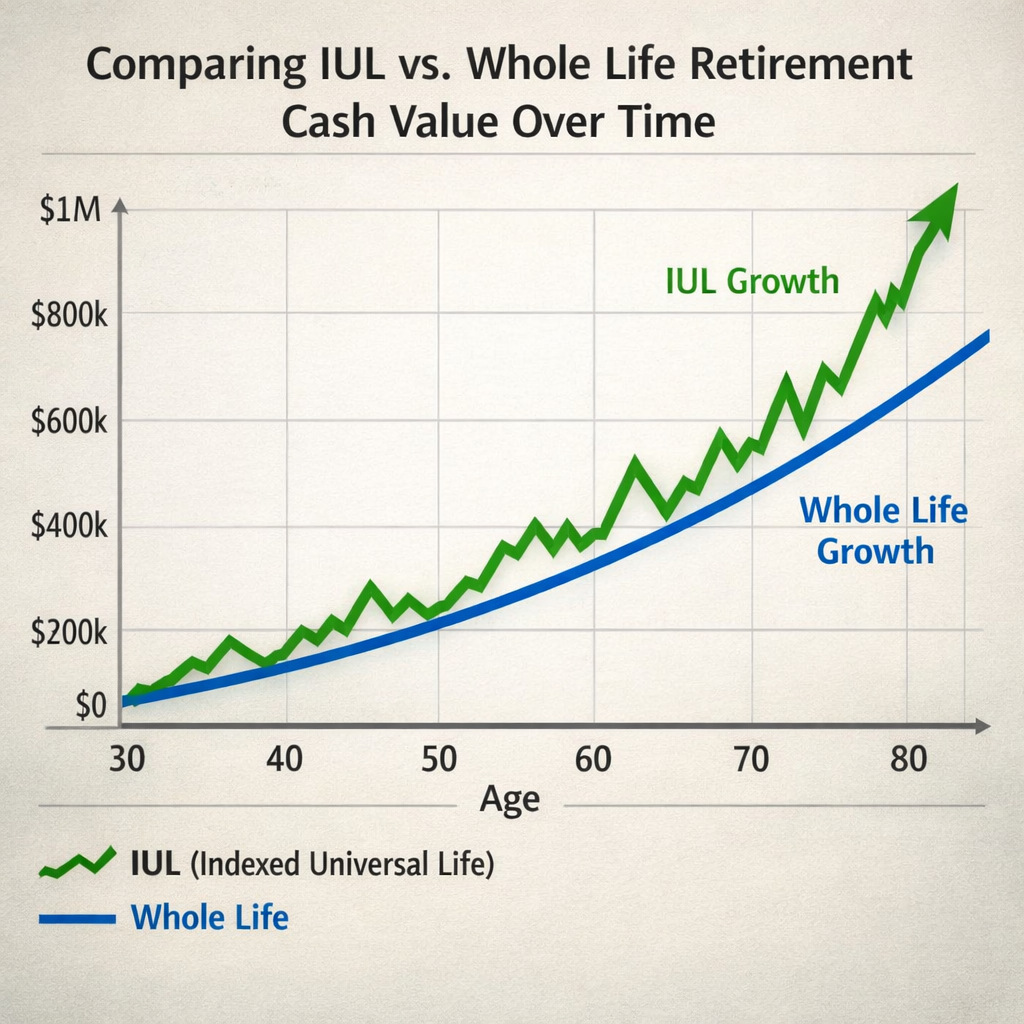

Cash‑value growth is where the rubber meets the road. Whole life offers a guaranteed rate, often around 2‑3% plus possible dividends. That growth is slow but steady. IUL growth depends on the index performance, the participation rate, and the cap. Lincoln WealthBuilder IUL, for example, caps at 10.25% but offers multiple indexes for diversification.

Imagine you have a 10‑year horizon. A whole‑life policy might give you a 2.5% annual increase, turning $100,000 cash value into roughly $128,000. An IUL with a 9% cap and 70% participation could, in a bullish market, push the same $100,000 to $150,000. But if the market stalls, the IUL could stay flat because of the floor.

Flexibility covers premium payments, death‑benefit adjustments, and policy loans. Only four of the 14 IULs in our study mention premium flexibility, Protective Indexed Choice UL, Pacific Life Trident IUL, Legal & General IUL, and Protection Builder IUL® 2. Whole life has none; the premium is locked.

Death‑benefit flexibility also matters. IULs can let the death benefit increase as cash value grows, which can be handy if you want a larger legacy later. Whole life usually keeps the death benefit fixed, unless you use dividends to purchase paid‑up additions.

Policy‑loan transparency is another clue. Only Penn Mutual IUL and North American Builder Plus IUL 4 disclose loan rates (6% locked for life and a variable capped at 5%). Whole life typically offers competitive loan rates without the need for a disclosure table.

So, how do you weigh these? Start by writing down your budget, then map each policy’s premium trajectory against your expected retirement cash‑flow needs. Add a column for projected cash value using both guaranteed and capped scenarios. That side‑by‑side view will show you whether the higher upside of an IUL outweighs its cost volatility.

In practice, many retirees prefer the certainty of whole life when they already have enough market‑linked assets. Those who still have room for growth often blend a modest IUL with other retirement accounts.

Bottom line: If you value cost stability and guaranteed growth, the whole‑life pick from Life Care Benefit Services wins. If you can tolerate some uncertainty for higher upside, look at Lincoln WealthBuilder IUL or Nationwide YourLife Indexed UL.

For a deeper dive on premium flexibility, check out Western & Southern’s guide on IUL vs whole life. It walks you through the key questions to ask your agent.

How IUL and Whole Life Fit into a Retirement Strategy

Retirement isn’t just about having enough money; it’s about having reliable sources that won’t run out. Both IUL and whole life can act like a hidden bank that you tap later.

Whole life builds cash value at a guaranteed rate, then lets you borrow tax‑free. The policy’s cash can supplement Social Security or cover a medical bill without triggering a penalty. Because the growth is tax‑deferred, the money compounds faster than a regular savings account.

One real‑world example: Mary, a 58‑year‑old teacher, bought a whole‑life policy from Life Care Benefit Services at age 40. By 58 she had $120,000 in cash value. She took a $30,000 loan to cover a home‑repair emergency. The loan interest was low, and she repaid it over five years, keeping the death benefit intact for her family.

IUL, on the other hand, can boost cash value faster when the market climbs. The policy’s cash value can be used for a “no‑cost” retirement phase once it covers the COI. That means you stop paying premiums and the policy lives on its own cash.

Here’s a step‑by‑step for using an IUL in retirement:

- Start the policy early, preferably before age 45, so the cash value has time to grow.

- Allocate a high percentage of each premium to the indexed portion. Aim for a participation rate of 70% or higher.

- Monitor the cap each year. If the cap drops, consider shifting more to the fixed‑interest side.

- When the cash value equals the total COI for the next 10 years, you can enter the “no‑cost” period.

- Take tax‑free loans against the cash value to cover living expenses. Keep the loan‑to‑value ratio below 30% to avoid policy lapse.

But IUL isn’t a set‑and‑forget tool. You must review the policy each anniversary, check the cap, participation rate, and COI. Missing a review can let fees erode your cash value.

Now, let’s watch a quick video that breaks down the retirement flow for both policies.

After the video, you’ll see why many advisors recommend pairing a whole‑life policy for the base protection and a modest IUL for growth. The whole‑life policy gives you a safety net, while the IUL can act as a supplemental retirement bucket.

Key takeaway: The only whole‑life policy that guarantees cash‑value growth in our research is Life Care Benefit Services Life Insurance. Pair it with an IUL like Lincoln WealthBuilder IUL if you want upside potential, but keep an eye on caps and COI.

Choosing the Right Policy for Your Retirement Goals

Now that you know the mechanics, let’s talk about picking the right one for you. The decision hinges on three personal factors: risk tolerance, budget, and timeline.

If you’re risk‑averse, you’ll likely gravitate toward whole life. The guaranteed cash‑value growth means you can predict exactly how much you’ll have at age 65. That can be comforting if you already have a 401(k) and want a stable supplement.

If you can handle a bit of market swing, an IUL can give you higher growth. Look for policies with caps above 9% and participation rates at or above 70%. Lincoln WealthBuilder IUL checks those boxes.

Budget is another filter. Whole‑life premiums are higher but stay flat. IUL premiums can start lower but may rise as you age. Use a simple spreadsheet: list your current monthly cash flow, subtract essential expenses, and see how much you can comfortably allocate to a policy.

Timeline matters, too. If you plan to retire at 60, you need a policy that has built enough cash value by then. Whole life usually needs 10‑15 years to generate meaningful cash. IUL can accelerate that if the market performs well, but you must monitor caps.

Here’s a quick checklist to run when you compare quotes:

- Check the premium amount and whether it’s fixed or flexible.

- Note the cap, participation rate, and floor for the IUL.

- Look at the COI trend over the next 10 years.

- Ask about loan interest rates; Penn Mutual IUL’s 6% locked rate is rare.

- Confirm the dividend history if you’re looking at whole life.

- Ask for a side‑by‑side illustration that projects cash value at age 65 under both a flat market and a bullish market.

When you sit with an advisor, bring these points. Ask them to model a 0% index year to see how the floor protects you. If the cash value still drops, you might be looking at a policy with high fees.

Our pick, Life Care Benefit Services Life Insurance, scores high on all these checks: fixed premium, guaranteed cash‑value growth, and transparent loan terms. That’s why we recommend it as the first choice for most retirees.

And if you need a real‑world example, consider Tom, a 45‑year‑old small‑business owner. He chose the Life Care whole‑life policy for a $250,000 death benefit and $100,000 cash value target. At age 55 he added a Lincoln WealthBuilder IUL for extra growth. By 65 his whole‑life cash value sits at $80,000, and the IUL adds another $60,000, giving him a solid $140,000 tax‑free supplement for retirement.

Bottom line: Align the policy with your comfort level. If you like certainty, whole life wins. If you want upside and can manage the details, an IUL can boost your retirement nest egg.

FAQ

What is the main advantage of using an IUL for retirement planning?

An IUL lets you earn cash‑value growth that’s linked to a market index, so you can capture upside without direct stock risk. The floor protects you from losing cash value when the market drops. This can give you a larger pool of tax‑deferred money to tap in retirement, especially if you choose a policy with a high cap and strong participation rate. But you must watch the cap, participation, and COI to avoid surprises.

How does whole life provide retirement income compared to an IUL?

Whole life builds cash value at a guaranteed rate, often around 2‑3% plus possible dividends. That steady growth means you can predict the amount you’ll have at retirement. You can borrow against the cash value tax‑free, and the loan interest is usually lower than an IUL loan. The trade‑off is slower growth, but the certainty can be a big comfort for retirees who already have market‑linked assets.

Can I switch from a whole‑life policy to an IUL later?

No, you can’t directly convert a whole‑life policy into an IUL. You would need to apply for a new IUL policy, which could mean a new medical exam and higher premiums if you’re older. Some carriers offer a “paid‑up addition” rider that adds a small indexed component to a whole‑life policy, but that’s not a full IUL. It’s usually simpler to keep both policies if you want both features.

How do policy loan rates affect my retirement planning?

Loan rates determine how much interest you pay on the money you borrow from the cash value. A lower rate means less erosion of the death benefit. Only Penn Mutual IUL discloses a locked 6% loan rate, which is attractive. Whole‑life policies often have lower or undisclosed rates, but the loan reduces the death benefit until repaid. Always model loan‑to‑value ratios to ensure you don’t risk policy lapse.

What should I look for in the cap and participation rate of an IUL?

The cap is the maximum credit you can earn in a period; the participation rate is the percentage of the index gain that gets credited. A higher cap and participation rate give you more upside. For example, Lincoln WealthBuilder IUL caps at 10.25% with a high participation rate, while National Life Group Summit IUL caps at 11% but has the highest COI, which can erode returns. Balance the cap with COI and your risk tolerance.

Is the cash value from a whole‑life policy taxable when I withdraw it?

You can withdraw up to the amount you’ve paid in premiums tax‑free. Anything above that is taxed as ordinary income. Loans are generally tax‑free as long as the policy stays in force. That’s why many retirees prefer taking loans instead of withdrawals to keep the tax benefit.

Conclusion

Choosing between IUL and whole life for retirement planning comes down to how you weigh risk, cost, and flexibility. Whole life offers a rock‑solid, predictable cash‑value growth that can serve as a reliable retirement supplement. The IUL, when paired with a strong cap and participation rate, can boost your cash pool faster but demands active monitoring of fees and market credits.

Our research shows that Life Care Benefit Services Life Insurance is the clear winner for those who want guaranteed growth and stable premiums. If you’re comfortable with a bit more complexity and want the chance for higher returns, Lincoln WealthBuilder IUL or Nationwide YourLife Indexed UL are solid secondary picks.

Take the next step today. Schedule a free consultation with a licensed Life Care Benefit Services advisor, get a side‑by‑side illustration, and see which policy fits your retirement timeline. The right choice will give you peace of mind, a tax‑advantaged cash source, and the protection your loved ones deserve.