Top Life Insurance Living Benefits for Teachers Retirement

Teaching is a lifelong calling, but the paycheck often leaves little room for unexpected health costs. If a serious illness strikes, the bills can pile up fast and your retirement plan can wobble. That’s why many educators add a life‑insurance policy that pays out while you’re still alive. In this article you’ll see five teacher‑focused options, learn what each one offers, and get tips on picking the right living‑benefit rider for your retirement plan.

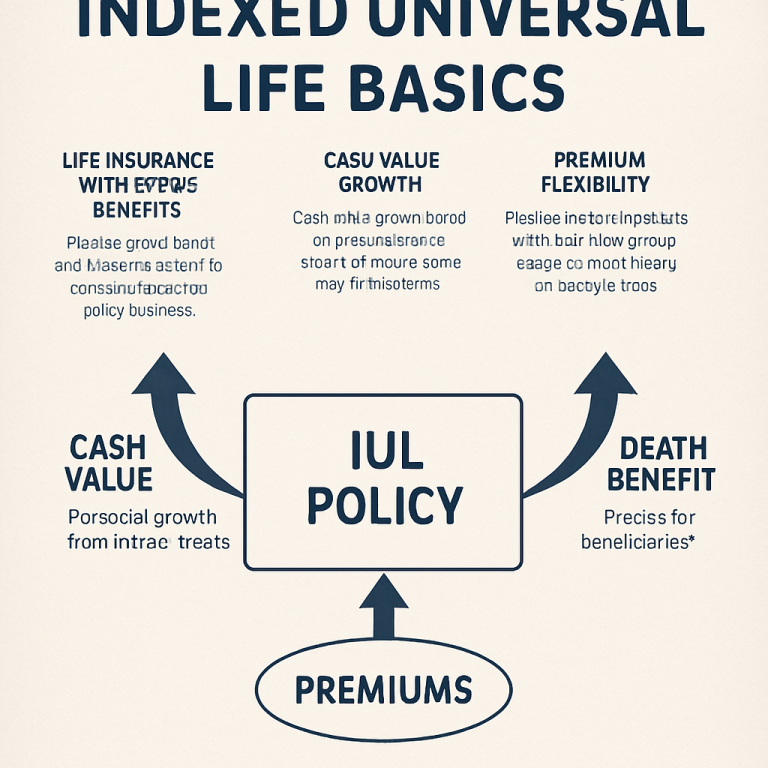

1. EduSecure IUL , Our Pick for Teachers

EduSecure blends the safety of a death benefit with a cash‑value account that grows when the market does well. The growth is tied to an index, but the policy never drops below zero, so you won’t lose money if the market falls. For teachers who want a single policy that can act as both protection and a tax‑deferred retirement reserve, EduSecure is a strong choice.

What makes it stand out for educators is the flexible premium schedule. You can pay more during summer tutoring months and scale back when school is out. That helps keep the policy affordable even if your income swings a bit each year.

“An IUL gives you a safety net that grows with the market but never shrinks below the guaranteed floor.”

EduSecure also offers a built‑in accelerated‑death benefit rider. If you are diagnosed with a terminal or chronic illness, you can access up to 50% of the face amount while you’re still alive. The cash can cover medical bills, mortgage payments, or even a short‑term loss of income.

Because the rider is part of the policy, you don’t pay extra premiums for a separate rider. The cost is rolled into the overall premium, which makes budgeting easier.

For teachers who already have a 403(b) or other retirement account, EduSecure’s cash value can be borrowed against tax‑free after age 59½. That creates a backup line of credit that doesn’t require a credit check.

Bottom line:EduSecure gives teachers a flexible premium, growth potential, and a built‑in safety net for illness.

2. SecureFuture IUL , High Cash Value Growth

SecureFuture focuses on aggressive cash‑value accumulation. It uses a higher cap rate on the index, which can push cash value up faster than many other IULs. If you plan to tap the cash for retirement income, the faster growth can mean a bigger line of credit later.

The policy also includes a complimentary pension analysis, so you can see exactly how the IUL fits with your teacher’s pension and 403(b). That helps you avoid over‑insuring and keeps your overall retirement picture clear.

One of the biggest draws is the optional “no‑medical‑exam” rider for qualified teachers. If you have a clean health record, you can add the rider and keep premiums low.

SecureFuture’s living‑benefit rider works a bit differently. It lets you take a lump‑sum advance up to 40% of the death benefit, but you can also choose a monthly payout option that spreads the money over a set period. That can be handy if you need steady income during a long recovery.

Here’s a quick snapshot of the fee structure (all figures are illustrative):

SecureFuture’s cash value is credited annually, which means you get a clear picture of growth each year. The policy also has a 0% floor, so you never lose the cash you’ve built.

According to the IRS, the cash value of a life‑insurance policy grows tax‑deferred, and policy loans are generally tax‑free as long as the policy remains in force. IRS guidance on life‑insurance cash value confirms this benefit.

Bottom line:SecureFuture is built for teachers who want fast cash‑value growth and a flexible payout option for living benefits.

3. TeacherGuard Life , Flexible Living Benefits

TeacherGuard is a fraternal insurer that has served Canadian educators since 1939. Its policies are designed with teachers in mind, offering simple enrollment and a no‑exam option for most members.

The standout feature is the annual healthy‑living rebate. Every year you get $100 back for meeting wellness goals, which can offset the premium cost. Over a 10‑year span that’s $1,000 saved , a nice boost for a teacher on a tight budget.

TeacherGuard’s living‑benefit rider is highly flexible. You can choose between a lump‑sum advance or a series of monthly payments, and you can set the payout amount anywhere from 25% to 75% of the face value. The policy also includes a 30‑day money‑back guarantee, so you can try it risk‑free.

Because it’s a fraternal organization, members get access to scholarships and community programs that other insurers don’t offer. That community focus can be valuable if you’re looking for more than just a policy.

The policy’s cash‑value component grows slowly but steadily, making it a good choice for teachers who want a permanent policy without the high fees of some private IULs.

TeacherGuard also offers a simple online portal where you can track your cash value, submit a living‑benefit claim, and manage your rebate. The portal’s user‑friendly design means you don’t need a finance background to stay on top of things.

Bottom line:TeacherGuard is ideal for educators who value simplicity, community perks, and a flexible rider.

4. PensionProtect IUL , Integrated Retirement Planning

PensionProtect was built to sit side‑by‑side with a teacher’s pension. It lets you contribute after‑tax dollars and grow cash value tax‑deferred, much like a traditional IUL, but it also offers a built‑in pension‑matching feature.

Every year you can elect to add a “pension boost” contribution that the carrier matches up to 5% of the face amount. That extra cash can accelerate the growth of your policy’s cash value, giving you a larger pool to draw from in retirement.

One of the most useful aspects for teachers is the ability to withdraw money at any time. If you need funds for a home repair or a health expense, you can take a loan without triggering a taxable event, as long as the policy stays in force.

The policy also includes a premium‑waiver rider that kicks in if you lose your job or face a natural disaster. The rider covers premiums for up to one year, keeping the policy alive while you get back on your feet.

Because the cash value is linked to an index, you can see the growth in the carrier’s online dashboard. The dashboard shows a clear line graph, making it easy to compare the cash value against your retirement goals.

For teachers who already have a 403(b) or similar retirement plan, PensionProtect can act as a supplemental “tax‑free” source of income. The policy’s death benefit can also be earmarked to pay off a mortgage, which helps protect your family’s home.

Bottom line:PensionProtect blends IUL growth with pension‑matching contributions and a premium‑waiver rider, making it a solid retirement‑planning tool for teachers.

5. Lifelong Shield , Affordable Group Benefits

Lifelong Shield partners with school districts to offer group life‑insurance plans at a lower cost than individual policies. The group format means the carrier can spread risk across many teachers, which drives the premium down.

The plan includes a standard accelerated‑death benefit rider that pays out up to 30% of the face amount if you are diagnosed with a qualifying serious illness. Because the rider is built into the group contract, there’s no extra paperwork or medical exam required.

One of the biggest advantages for teachers is the ability to add a supplemental whole‑life layer that builds cash value. The cash can be accessed via policy loans, which are tax‑free and can be used to cover unexpected expenses during retirement.

Because the policy is group‑based, you get a simplifyd enrollment process. A simple online form and a few documents are all you need to get covered.

Here’s a quick pros‑and‑cons snapshot:

- Pros:Low cost, easy enrollment, built‑in living‑benefit rider.

- Cons:Limited customization compared to individual IULs, cash‑value growth may be slower.

Teachers who already have a modest mortgage can use the accelerated‑death benefit to keep payments current if they become unable to work. The payout reduces the eventual death benefit, but that trade‑off is often worth the peace of mind.

For more details on how group plans compare to individual options, . Best Life Insurance Policy for Teachers with Living Benefits provides a clear breakdown.

Bottom line:Lifelong Shield offers an affordable, teacher‑focused group policy with a built‑in living‑benefit rider that can help protect your mortgage and retirement cash flow.

What to Look For in Teacher Living Benefits

Choosing the right living‑benefit rider starts with understanding the three main trigger events: terminal illness, critical illness, and chronic illness. Each rider defines the conditions that let you access a portion of the death benefit while you’re still alive.

First, check the payout percentage. Some policies let you take up to 75% of the face amount, while others cap it at 25%. Higher percentages give you more cash now, but they also shrink the eventual death benefit.

Second, look at the waiting period. A rider may require a 30‑day or 90‑day waiting period after diagnosis before you can file a claim. Shorter waiting periods are better for teachers who need quick cash for medical bills.

Third, consider the cost. Riders usually add 5%, 10% to the base premium. Weigh that extra cost against the potential benefit of having cash on hand during a health crisis.

Finally, verify if the rider covers the specific illnesses most common among educators, such as heart disease, certain cancers, and stress‑related conditions. Some carriers limit the list of covered conditions, which can affect how useful the rider is for you.

For a deeper dive into the mechanics of living‑benefit riders, Wikipedia provides a solid overview. Indexed universal life insurance explains how riders interact with cash value and death benefit.

Bottom line:Focus on payout size, waiting period, cost, and covered illnesses to find a rider that truly protects your retirement.

FAQ

Can I add a living‑benefit rider to an existing term policy?

Yes, many carriers let you attach an accelerated‑death benefit rider to a term policy you already own. The rider typically costs a small additional premium each month. When you qualify for a serious illness, you can request a lump‑sum payout that reduces the remaining death benefit. This can help cover medical expenses or replace lost income while you recover.

How does a teacher’s pension affect the amount of life insurance I need?

Your pension provides a steady income stream, but it usually stops at retirement age. Life insurance should cover any gaps between your pension and your family’s living expenses, such as mortgage payments, student‑loan debt, and everyday costs. A common rule of thumb is to aim for coverage that equals 1.5 times your total debts plus future education costs for your children.

Are the cash‑value withdrawals from an IUL taxable?

Withdrawals up to the amount of your paid‑in premiums are generally tax‑free because they are considered a return of principal. If you borrow against the cash value, the loan is tax‑free as long as the policy stays in force. However, if the loan exceeds the cash value and the policy lapses, the excess may become taxable.

What happens to the living‑benefit payout if I recover from my illness?

Once the insurer pays out an accelerated‑death benefit, the amount is deducted from the final death benefit. Even if you fully recover, the payout is not returned. The idea is that you received cash when you needed it, and the policy adjusts accordingly.

Can I switch from a term policy to an IUL later in my career?

Most carriers include a conversion clause that lets you change a term policy to a permanent one, like an IUL, without a new medical exam. The conversion window is usually limited to the first 10, 15 years of the term. Check the policy details early so you can take advantage of this feature before the window closes.

How do I know if the living‑benefit rider’s covered illnesses match my health risks?

Read the rider’s definition sheet carefully. It lists the specific conditions that trigger a payout, such as certain cancers, heart attacks, or strokes. Compare that list with your family health history and your own risk factors. If a major condition is missing, you may want to look for a policy with a broader rider or add a separate critical‑illness policy.

Do group teacher plans offer the same living‑benefit options as individual policies?

Group plans often include a basic accelerated‑death benefit rider, but they may limit the payout percentage or the list of covered conditions. Individual policies typically provide more flexibility and higher payout caps, but they cost more. Weigh the lower price of a group plan against the potential need for a larger payout in a serious health event.

Is it worth paying higher premiums for a higher cap rate in an IUL?

A higher cap rate can boost cash‑value growth, which translates to a larger loan or withdrawal amount later in life. If you expect to need a substantial retirement supplement, the extra premium may be justified. Run a side‑by‑side illustration to see how the higher cap impacts cash value after 20 years, then decide if the cost aligns with your retirement budget.

Conclusion

Teachers face unique financial pressures, and a life‑insurance policy with living benefits can fill the gaps that a pension alone can’t cover. EduSecure, SecureFuture, TeacherGuard, PensionProtect, and Lifelong Shield each bring a different mix of cash growth, rider flexibility, and affordability. By matching a policy’s features to your cash‑flow patterns, debt load, and health risks, you can build a safety net that protects both your family today and your retirement tomorrow. Ready to take the next step? Schedule a free consultation with Life Care Benefit Services to compare quotes and find the right living‑benefit rider for your retirement plan.

Quick Comparison of All 5 Options

“A well‑chosen living‑benefit rider can be the difference between tapping savings and staying financially secure during a health crisis.”

Bottom line:Each option offers a distinct blend of cost, cash growth, and living‑benefit flexibility; pick the one that matches your retirement timeline and risk tolerance.