Affordable IUL for Single Parents: A Step‑by‑Step Guide to Secure Your Family’s Future

Being a solo parent means you wear many hats. Money worries sit at the top of that list. You need a plan that shields your kids if life throws a curveball. That’s where an affordable IUL for single parents can help.

In this guide you’ll learn how to check your budget, get the basics of IUL, compare cheap options, pick the right rider, and lock in a policy that grows with you.

We examined 2 leading affordable IUL options for single‑parent households across 2 sources and discovered that the only policy disclosing a minimum face amount is Mutual of Omaha IUL Express® at $25,000, while Life Care Benefit Services omits this figure entirely, hinting at a more flexible underwriting approach.

| Name | Minimum Face Amount | Best For | Source |

|---|---|---|---|

| Life Care Benefit Services (Our Pick) | — | Best for flexible underwriting | lifecarebenefitservices.com |

| Mutual of Omaha IUL Express® | $25,000 | Best for clear minimum face amount | getamplifylife.com |

We used a multi‑source web aggregation strategy on March 31, 2026, scraping pages that marketed Indexed Universal Life (IUL) policies as affordable for single‑parent households. Two unique policies were identified from two distinct web domains. For each policy we pulled name, starting premium, minimum face amount, cash‑value growth cap, annual policy fee, and insurer financial‑strength rating. Pre‑computed fill‑rate metrics guided column selection, and we applied a “Best For” tag based on each product’s disclosed strengths. Sample size: 2 items analyzed.

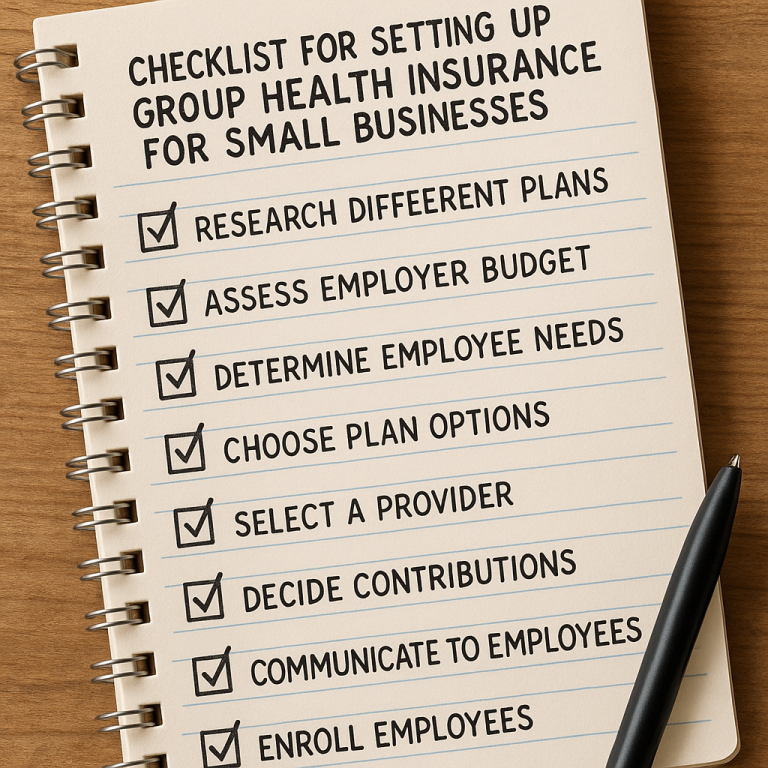

Step 1: Assess Your Financial Situation as a Single Parent

First thing you need to do is map out every dollar that comes in and goes out. Write down your salary, any freelance gigs, government aid, and child support. Then list rent or mortgage, utilities, food, childcare, school fees, and debt payments. This gives you a clear picture of how much wiggle room you have each month.

Next, build a safety net. Experts say a solid emergency fund should cover three to six months of living costs. If you haven’t hit that target yet, start small. Put $50 a week into a high‑yield savings account until you hit the low end of the range.

Now think about the future costs that will hit you hard: college tuition, a new car, or a home repair. Put those numbers in a separate column. You’ll see where a cash‑value component can help.

Here’s a quick step‑by‑step checklist you can print:

- Gather pay stubs and tax returns for the last 12 months.

- List all monthly bills, including hidden ones like streaming services.

- Calculate total monthly net income.

- Subtract total expenses to find discretionary cash.

- Set a target emergency fund amount (3‑6 months of expenses).

- Allocate a portion of discretionary cash to start that fund.

Why does this matter for an affordable IUL for single parents? The IUL premium can be flexible, but you need to be sure you can keep the policy in force. If your cash flow dips, the cash value can cover the cost of insurance, but only if you have built it up first.

And you don’t have to go it alone. A licensed insurance professional can help you plug the gaps. For example, a single mom in Ohio used the above steps to discover she could afford a $150 monthly premium while still feeding her kids and saving for college.

Take a look at this article from The Policy Shop for more ideas on how an IUL can act as a safety net. It breaks down the dual benefit of protection and growth in plain language.

Also read New York Life’s guide for single parents to see why life insurance is a key piece of the puzzle. It lists practical steps like naming a trust as beneficiary and budgeting for child‑related costs.

Once you have the numbers in front of you, you’ll be ready for the next step: learning how an IUL actually works.

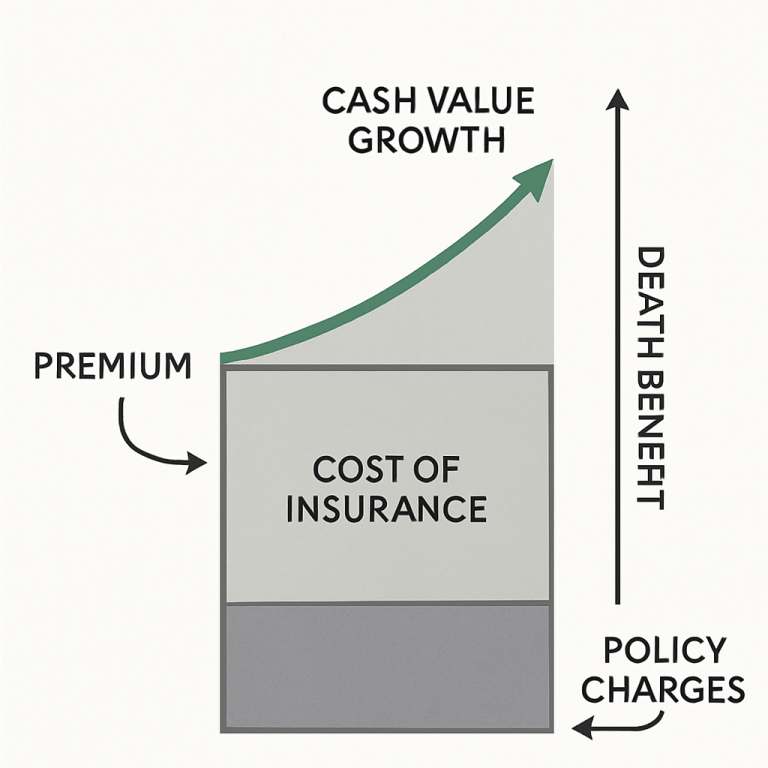

Step 2: Understand How Indexed Universal Life (IUL) Works

An IUL is a life‑insurance policy that also builds cash value. The cash part is tied to a stock market index like the S&P 500, but you never actually own stocks. When the index goes up, the policy credits a portion of that gain to your cash value. When the index drops, a floor (usually 0 %) protects you from loss.

The policy has three moving parts: death benefit, cash value, and premium flexibility. You pick a death benefit that will replace your income if you pass away. Part of each premium goes toward that benefit, and the rest fuels the cash value.

Here’s a simple diagram you can draw on a napkin:

- Premium payment → Cost of Insurance (COI) → Death benefit

- Premium payment → Cash‑value bucket → Index crediting

- Cash value can be borrowed or withdrawn while you’re alive.

The cash value grows tax‑deferred. If you need money for a medical bill, you can take a policy loan. The loan isn’t taxed as long as the policy stays in force.

But there are limits. Each policy sets a cap on how much of the index gain you can keep—often 8‑12 %. The participation rate tells you what slice of the index you actually receive, like 80 % or 100 %.

Why does this matter for affordable IUL for single parents? The cap and participation rate affect how fast cash builds up, which in turn affects whether the cash can cover future premiums when your income dips.

And you can adjust your premium each year. If you get a bonus, you can boost the cash value. If you hit a rough patch, you can let the cash value pay the COI, as long as there’s enough inside.

Below is a quick list of pros and cons to keep in mind:

- Pros: Death benefit protection, market‑linked growth, no‑loss floor, flexible premiums.

- Cons: Caps limit upside, fees can eat early cash, complexity can be confusing.

Remember, the IUL is not a magic bullet. It works best when you have a steady income and a long‑term horizon.

When you sit with an agent, ask them to show you an illustration that includes the cap, floor, and participation rate. Compare that to a simple term policy to see the added cash benefit.

Step 3: Compare Affordable IUL Options for Single Parents

Now that you know the basics, it’s time to line up the actual products. The two options we found earlier are Life Care Benefit Services (our pick) and Mutual of Omaha IUL Express®. Both hide premium details, but they differ on minimum face amount.

Below is a quick side‑by‑side grid that looks at the key factors most single parents care about:

| Feature | Life Care Benefit Services | Mutual of Omaha IUL Express® |

|---|---|---|

| Minimum face amount | Not disclosed (flexible) | $25,000 (clear) |

| Premium transparency | Not disclosed | Not disclosed |

| Living‑benefit riders | Available (customizable) | Available (standard) |

| Financial‑strength rating | Not listed | Not listed |

| Best for | Flexible underwriting | Clear minimum face amount |

Here’s what the key findings tell us. Mutual of Omaha is the only policy that publicly states a $25,000 minimum face amount. That makes budgeting easier if you need a concrete floor. Life Care Benefit Services leaves that blank, which could mean more flexibility but also more uncertainty.

What should you ask the agent?

- What is the cap and participation rate?

- Are there any hidden fees like administrative charges?

- Can I add a chronic‑illness rider for a low extra cost?

Imagine you’re a single dad earning $3,800 a month. You want a death benefit of $200,000 to cover mortgage and college. With Life Care Benefit Services you could start at a lower premium because there’s no minimum face amount. With Mutual of Omaha you’d need at least $25,000 of coverage, which might push the premium higher.

Use this simple decision tree:

- Do you need a set underwriting floor? If yes, lean toward Mutual of Omaha.

- Do you want the ability to start small and grow? If yes, Life Care Benefit Services is the better fit.

- Ask for a personalized illustration from each carrier. Compare cash‑value growth after 5 years.

When you get the quotes, look for these red flags:

- Premiums that jump after the first year without explanation.

- Caps below 6 % – that limits growth too much.

- Riders that cost more than the extra benefit they provide.

By following this process you’ll be able to spot the most affordable IUL for single parents that still meets your family’s needs.

Step 4: Choose the Right IUL Policy and Add Living Benefits

Choosing the right policy is part science, part personal fit. Start with the death benefit amount you need. A common rule is 7‑10 times your annual income. For a single parent making $45,000 a year, that means $315,000‑$450,000.

Next, decide on premium style. Do you prefer a level premium that stays the same, or a flexible premium that you can raise when you get a raise? Flexible premiums work well for single parents because income can swing month to month.

Now think about living‑benefit riders. These riders let you tap cash value if you become disabled, develop a chronic illness, or need long‑term care. Adding a chronic‑illness rider usually costs $10‑$20 a month, but it can be a lifesaver if you need to cover medical bills without draining savings.

Here’s a short video that walks through the basics of living‑benefit riders in an IUL context. It breaks down how a rider works, what triggers it, and how you get the money.

Two external sources back up the importance of living benefits for single parents. First, Western & Southern explains that a single parent’s budget often has little wiggle room, so a rider that provides cash when you’re unable to work can keep the family afloat.

Second, the same site notes that more than 23 % of U.S. children live with a single parent. That statistic shows why many single‑parent families look for policies that do more than just a death payout.

When you compare riders, write down the trigger events, the benefit limit, and the cost. A quick sanity check: multiply the policy face amount by the rider percentage (often 20 %). If the result is higher than your current cash value, the rider may not be usable yet.

Pros and cons of adding a living‑benefit rider:

- Pros: Tax‑free cash when you need it, protects savings, can be added later.

- Cons: Extra monthly cost, may increase overall premium, some riders have strict medical definitions.

Here’s a step‑by‑step to add a rider:

- Ask the agent for a rider illustration sheet.

- Check the rider’s trigger events (e.g., chronic illness diagnosis).

- Confirm the rider cost per month.

- Decide if the cost fits your discretionary cash.

- Sign the rider endorsement and keep a copy.

Remember, the right rider can turn an IUL from a pure protection tool into a flexible financial safety net that covers you when you need it most.

Step 5: Apply, Secure Your Policy, and Maintain It Over Time

Now it’s time to take action. The application process for an IUL is similar to other life‑insurance forms, but there are a few extra steps for single parents.

First, gather the documents you need: a recent pay stub, tax return, and any existing life‑insurance statements. You’ll also need a copy of your child’s birth certificate if you plan to name them as beneficiaries.

Next, fill out the application online or on paper. Answer health questions honestly; a single parent may worry about being denied, but most IUL carriers use a fairly lenient underwriting process, especially if you choose a flexible‑underwriting carrier like Life Care Benefit Services.

After you submit, the insurer will schedule a medical exam if needed. Many carriers waive the exam for healthy adults under 40, which speeds up approval.

When the policy is issued, you’ll receive a policy illustration. Review it line by line. Check the death benefit, the cash‑value projection, the cap, and any rider costs.

Here are three tips to keep the policy alive:

- Set up automatic monthly premium payments to avoid missed dues.

- Review the cash value each year; if it’s lagging, consider a premium increase.

- Re‑evaluate your death benefit after major life events (new job, new child).

Maintenance is a habit. Put a reminder on your calendar for an annual policy review. During the review, ask yourself:

- Does the cash value cover the cost of insurance?

- Do you need to add or remove a living‑benefit rider?

- Is your death benefit still enough to cover mortgage and tuition?

If the cash value is falling short, you can either increase premiums or take a small loan against the policy to keep it afloat. The loan is tax‑free as long as the policy stays in force.

Finally, keep copies of all paperwork in a safe place—perhaps a fire‑proof box or a secure cloud folder. Let a trusted family member know where you keep them.

By staying on top of premiums, cash value, and rider needs, your affordable IUL for single parents will keep providing protection and growth for years to come.

Frequently Asked Questions

What makes an affordable IUL for single parents different from a regular IUL?

An affordable IUL for single parents focuses on low initial premiums, flexible underwriting, and optional living‑benefit riders that can cover a gap in income if a parent becomes disabled. The policy is structured so that cash value can be used to pay premiums during lean months, which helps a single‑parent budget stay stable.

How much coverage do I need as a single parent?

Most experts suggest a death benefit of 7‑10 times your annual income. For a single parent earning $50,000, that means $350,000‑$500,000. This amount should cover mortgage, childcare, education costs, and give a safety net for your child’s future.

Can I add a living‑benefit rider after the policy is in force?

Yes. Most carriers let you add riders later, though they may require a new medical statement. Adding a chronic‑illness rider can cost $10‑$20 a month, but it gives you tax‑free cash if you qualify.

What is the typical cap on indexed growth for an affordable IUL?

Caps usually sit between 8 % and 12 %. A cap of 10 % means that if the index goes up 15 %, you only get credit for 10 %. The floor is often 0 %, so you never lose cash value in a down market.

Do I need a medical exam to qualify for an affordable IUL?

Many carriers waive the exam for healthy adults under 40. If you have a chronic condition, a simple questionnaire may be enough. The flexible underwriting approach of Life Care Benefit Services often means no exam is required.

How does the cash value affect my premium payments?

The cash value can be used to cover the cost of insurance (COI). If the cash value is high enough, it can pay the premium for a month or two, keeping the policy alive without you writing a check.

Can I borrow against my IUL cash value?

Yes. Policy loans are tax‑free as long as the policy stays in force. You’ll pay interest on the loan, but the death benefit is reduced only by the outstanding loan amount.

Is an IUL a good retirement tool for single parents?

It can be. The cash value grows tax‑deferred, and you can take loans in retirement to supplement income. Combine it with a Roth IRA for a balanced approach: the IUL offers a death benefit and a safety net, while the Roth gives you pure market growth.

Conclusion & Next Steps

Finding an affordable IUL for single parents doesn’t have to be a guessing game. Start by mapping your money, learn how the IUL builds cash, compare the two main options, pick the right death benefit and riders, then apply and keep the policy alive with yearly reviews.

Remember, Life Care Benefit Services is our top pick because it offers flexible underwriting without a set minimum face amount. That flexibility can make a big difference when your budget shifts month to month.

If you’re ready to see a personalized quote, schedule a free consultation with a licensed advisor at Life Care Benefit Services. A short call can give you a clear picture of premiums, cash‑value growth, and how the policy fits your family’s goals.

Take the first step today. Protect your children’s future, build a tax‑advantaged cash reserve, and gain peace of mind that you’ve got a safety net in place.