Affordable IUL Policy for Single Parents: A Practical Guide

Single parents face a tough math problem: one income, many bills, and a future that can change in a heartbeat. If you lose that income, your child’s world can wobble. An affordable IUL policy for single parents can lock in protection and give you a cash‑value tool you can tap while you’re alive. In this guide you’ll learn why an IUL can fit a tight budget, how to size the coverage, what to compare, and how to lock in living benefits that grow with you.

Understanding Why IUL Can Be Affordable for Single Parents

When you’re the only earner, every dollar counts. An affordable IUL policy for single parents offers two things at once: a death benefit that can replace income, and a cash‑value account that can be used for real‑world needs.

Think about it this way. A single‑parent home often covers housing, food, childcare, school fees, and health costs. If that paycheck disappears, the ripple can hit every line item. A well‑structured IUL can fill the gap with a lump‑sum payout that lets a guardian keep the lights on while they sort out finances.

Life insurance isn’t just for high earners. The Western & Southern guide notes that more than 23% of U.S. kids live with a single parent, and most families rely on one paycheck for everything. That fact alone makes a protection plan a practical need, not a luxury.

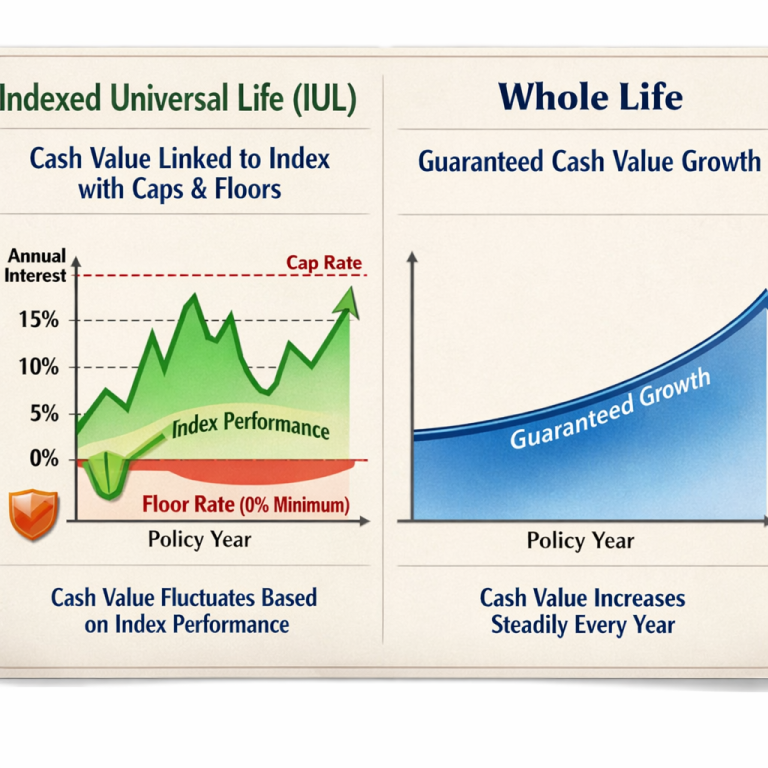

Why can an IUL be affordable? First, the policy lets you set a flexible premium. You can start low and raise payments when a bonus or tax return arrives. Second, the cash‑value growth is linked to a market index, but the policy has a floor (usually 0%). That means you never lose money when the market dips, so the insurer’s risk stays low and they can keep premiums down.

Third, many single parents start with term coverage and later add an IUL rider as income grows. The shift lets you keep costs low early on, then add the cash‑value feature when you’re ready.

And there’s a hidden benefit. The living‑benefit rider lets you borrow against the cash value if you become disabled or need long‑term care. That can replace lost wages without a bank loan.

But you need to size the policy right. A common rule of thumb is 7‑10 times your annual income, but you should also factor in mortgage balance, college costs, and any debt you’d want cleared.

Here’s a quick checklist:

- List monthly expenses you’d need covered if income stopped.

- Add future costs like tuition, a new car, or a down payment.

- Pick a death benefit that covers that total plus a safety margin.

Use a free online calculator to plug those numbers in. The result will give you a target face amount.

Finally, remember that an IUL is a long‑term tool. The longer you stay in the policy, the more cash value builds, and the lower the cost‑of‑insurance (COI) becomes. That makes the policy cheaper over time, which is a win for anyone on a tight budget.

For more detail on how the index credit works, see the Western & Southern guide on life insurance for single parents. It breaks down the numbers in plain language.

Another helpful read from the same source explains how to choose a cap and participation rate that balance growth and cost. Understanding those terms helps you avoid overpaying for features you never use.

Step 1: Assess Your Financial Needs and Coverage Gaps

Before you look at policies, you need a clear picture of what you actually need. An affordable IUL policy for single parents should match both your protection goals and your cash‑flow reality.

Start with a simple spreadsheet. List every recurring expense – rent or mortgage, utilities, groceries, childcare, school fees, health insurance, and transportation. Then add occasional costs like car repairs, holiday gifts, and a college fund.

Next, estimate how long you’d need that money. If your child is five, you might plan for 13 more years of schooling, plus a few years after graduation for college.

Now, compare that total need with any existing coverage. Do you already have a term policy from an employer? Does a former spouse’s policy cover the kids? Identify any shortfalls.

Here’s a step‑by‑step worksheet you can print:

- Write down current monthly expenses.

- Multiply by 12 to get an annual need.

- Project the need for each year until your child turns 18.

- Sum the yearly amounts for a total coverage gap.

Once you have a number, you can size the death benefit. Remember, the cash value that builds in an IUL can also be used later, so you don’t have to over‑fund the death benefit if you plan to tap the cash value for things like a mortgage pause.

And don’t forget to factor in debts – credit cards, student loans, or a car loan. Those should be paid off quickly if you’re gone, so they belong in the coverage amount.

Real‑world example: Maya, a single mom of two, calculated $2,200 a month for all expenses. She projected $30,000 a year for the next 13 years, totaling $390,000. Her employer term policy only covered $150,000, leaving a $240,000 gap. She used that gap to request an affordable IUL policy for single parents with a $250,000 death benefit.

After the worksheet, you’ll have a concrete target. That target guides the next steps: comparing policies, checking premiums, and making sure the cash‑value growth will be enough to cover the cost‑of‑insurance as you age.

Tip: Keep the worksheet on your phone. Update it if your income or expenses change.

When you’re ready, move to the next step – comparing features.

For a deeper dive on budgeting for life insurance, see the Western & Southern budgeting guide. It offers a printable template you can adapt.

Step 2: Compare Policy Features and Cost Structures

Now that you know how much coverage you need, it’s time to line up the options. An affordable IUL policy for single parents can look very different from one insurer to another.

Focus on three pillars: premium flexibility, index credit mechanics, and living‑benefit riders. Each pillar affects both cost and the value you get.

Premium flexibility lets you adjust payments. A policy that lets you drop to a minimum premium during lean months can keep you from defaulting.

Index credit mechanics involve the cap, floor, and participation rate. A higher participation rate (80‑100%) means you capture more of the market’s upside. A reasonable cap (8‑12%) balances growth potential with cost. The floor (usually 0%) protects you from market loss.

Living‑benefit riders are the extra tools that let you tap cash while you’re alive. Common riders include accelerated death benefit for chronic illness, long‑term‑care rider, and waiver‑of‑premium rider if you become disabled.

Below is a quick‑reference table that shows what to look for when you compare quotes. This view is different from the one in the internal guide – it focuses on the three pillars mentioned above.

| Feature | What It Affects | What To Look For |

|---|---|---|

| Premium Flexibility | Monthly cash outflow & ability to adjust payments | Check minimum premium, and whether you can increase payments without re‑underwriting. |

| Cap & Participation | Potential indexed credit & growth ceiling | Higher participation (80‑100%) and caps around 9‑12% give decent upside. |

| Floor | Downside protection | Floor should be 0% or higher – you never lose cash value on market drops. |

| Living‑Benefit Riders | Cash access for illness, disability, long‑term care | Look for rider cost (usually $10‑$20 per month) and trigger conditions that match your health risk. |

| COI Trend | Long‑term sustainability of cash value | Ensure the cost‑of‑insurance rises slowly; front‑load cash in the first 5‑10 years. |

When you pull a quote, ask the agent to highlight each of these rows. That way you can see at a glance where the policy shines or where hidden fees hide.

Next, run a “stress test.” Plug a 0% index year into the illustration. If the cash value stays flat (thanks to the floor), the policy has a built‑in safety net.

Another practical tip: ask for a side‑by‑side table that compares at least two quotes. Seeing the premium, cap, participation, and rider cost together makes the decision clearer.

Real‑world scenario: Carlos, a single dad, got two IUL quotes. Quote A had a 6% participation and a 9% cap, but a $180 monthly premium. Quote B offered 8% participation, a 12% cap, and a $200 premium. After running a 0% stress test, he saw both kept cash value safe, but Quote B gave him more upside for the extra $20. He chose Quote B because the higher growth matched his long‑term goal of funding college.

Remember, the cheapest policy isn’t always the most affordable over 20 years. Look at the total cost of ownership, not just the first‑year premium.

For more on how caps and participation rates affect cost, see the Western & Southern explanation of index credits. It walks through real numbers in plain language.

Step 3: Choose a Trusted Provider and Apply (Video Walkthrough)

Finding a reputable carrier matters. Look for insurers with A or higher ratings from agencies like AM Best. A strong rating means they’re likely to stay solvent and keep paying claims decades from now.

Once you shortlist a few carriers, schedule a quick call with a licensed agent. A good agent will walk you through the illustration line by line, answer questions, and help you fill out the application.

Many agents use an online portal where you can upload documents, schedule a medical exam (if needed), and track the status. The whole process usually takes two to six weeks.

Here’s a simple three‑step checklist for the application:

- Gather personal info: birth date, Social Security, health snapshot, and desired death benefit.

- Complete the online questionnaire. Answer health questions honestly – a small mistake can delay approval.

- Schedule the medical exam (often a quick finger‑stick). Some carriers waive it for healthy adults under 40.

And if you prefer a face‑to‑face chat, many agencies set up Zoom meetings. That can help you see the illustration in real time.

Below is a short video that shows exactly how an agent walks a client through an IUL quote. Watch the pace, note the questions the agent asks, and see how the premium schedule changes as you adjust the cash value goal.

After the video, pause and write down any terms that feel fuzzy. Then ask the agent to explain those in plain language. The goal is to leave the call with a clear picture of the premium, the cap, and the rider cost.

When you get the final quote, double‑check that the minimum premium line matches the amount you can afford. If it’s higher, ask if you can start with a lower face amount and increase later.

For more guidance on choosing a carrier, see the Western & Southern carrier rating guide. It lists the top‑rated insurers for 2026.

Step 4: Maximize Living Benefits and Future Growth

Getting the policy in place is just the start. To get the most out of an affordable IUL policy for single parents, you need to use the living‑benefit riders and cash‑value growth wisely.

First, set up an accelerated death‑benefit rider that pays out a portion of the death benefit if you are diagnosed with a chronic illness. That can cover medical bills or replace lost wages without tapping the cash value.

Second, consider a long‑term‑care rider. It lets you draw cash to pay for assisted‑living or home‑care costs, keeping the family home stable.

Third, use the policy’s cash value as a low‑cost line of credit. Because loans are tax‑free (as long as the policy stays in force), you can borrow to cover a child’s tuition or a home repair, then repay at your own pace.

But don’t over‑borrow. Each dollar you loan reduces the death benefit until you repay. A good rule is to keep loans under 25% of the cash value.

Fourth, schedule an annual review. As your child grows, your needs shift. Maybe you need to raise the death benefit for college costs, or you can lower the premium once the cash value covers the COI.

Fifth, front‑load premiums in the early years. Adding extra cash in the first 5‑10 years builds a buffer that can cover the rising COI later, making the policy effectively “zero‑cost” in later life.

Real‑world illustration: Jenna, a single mother of three, added a chronic‑illness rider for $12 per month and a long‑term‑care rider for $15 per month. She also contributed an extra $100 each month for the first six years. By age 45, her cash value grew to $45,000, enough to cover the COI and still leave $10,000 for a college fund.

Another tip: align the index choice with your risk tolerance. If you’re comfortable with a bit more market swing, pick a blended index that offers higher participation. If you prefer safety, stick with a single‑index cap that’s lower but more predictable.

Finally, keep the policy documents in a safe place and share the location with a trusted family member or guardian. If something happens, they’ll know how to access the living‑benefit rider quickly.

Actionable checklist for maximizing benefits:

- Activate an accelerated death‑benefit rider within the first month.

- Set a loan limit of 25% of cash value and track it each year.

- Review the policy annually and adjust premium or death benefit as life changes.

- Front‑load extra cash for the first decade to lock in lower COI.

- Store policy paperwork with your will and guardian documents.

When you follow these steps, the affordable IUL policy for single parents becomes more than a safety net – it turns into a flexible financial tool that can support you today and protect your child tomorrow.

FAQ

What makes an affordable IUL policy for single parents different from a regular IUL?

An affordable IUL policy for single parents is built with flexible premiums, lower caps, and riders that address common single‑parent worries like disability or long‑term care. The policy lets you start with a modest payment and increase it as your income grows. It also includes an accelerated death‑benefit rider that can turn part of the death benefit into cash if you become seriously ill, helping you keep up with bills without dipping into savings.

How much coverage do I actually need?

Start by adding up all current monthly expenses – rent, food, childcare, school fees, and debt payments. Multiply by 12 for an annual figure, then project that amount for each year until your youngest child turns 18. Add any future costs like college tuition or a mortgage payoff. Compare that total to any existing coverage, and the difference is the amount you should target in an affordable IUL policy for single parents.

Can I change the premium after the policy starts?

Yes. One of the biggest advantages of an affordable IUL policy for single parents is premium flexibility. You can increase payments in a high‑earning year or drop to the minimum required amount when cash is tight. Just be sure the cash value stays enough to cover the cost‑of‑insurance, or the policy could lapse.

What are the living‑benefit riders and how do they work?

Living‑benefit riders let you tap the policy while you’re alive. Common riders include an accelerated death‑benefit rider for chronic illness, a long‑term‑care rider, and a waiver‑of‑premium rider if you become disabled. When a trigger event occurs, the insurer pays a portion of the death benefit or allows a loan without tax penalties. This cash can cover medical bills, replace lost income, or fund a child’s education.

Will the cash value be taxed when I withdraw it?

If you withdraw only the amount you’ve paid in premiums (your basis), the money is tax‑free. If you take out more than your basis, the excess is taxed as ordinary income. Policy loans are also tax‑free as long as the policy stays in force. That’s why many single parents use loans to pay for short‑term expenses and repay them later.

How long does it take to get the policy approved?

Most affordable IUL policies for single parents are approved in two to six weeks. The timeline depends on how quickly you complete the application, provide any needed medical info, and the insurer’s underwriting speed. Working with a knowledgeable agent can shave a few days off the process.

Conclusion & Next Steps

Securing an affordable IUL policy for single parents gives you two powerful tools: a death benefit that protects your child’s future and a cash‑value engine you can use while you’re alive. By assessing your true financial needs, comparing key features, choosing a solid carrier, and activating the right living‑benefit riders, you turn a simple insurance policy into a flexible financial safety net.

If you’re ready to take the next step, schedule a free consultation with a licensed agent at Life Care Benefit Services. They can pull personalized quotes, walk you through the illustration, and help you lock in a plan that fits your budget and long‑term goals.

Remember, the sooner you act, the sooner your family gains protection and the cash‑value starts growing. A small, consistent payment today can become a tax‑free source of money for college, a mortgage pause, or retirement years down the road.

Take charge of your family’s financial security now. Request a quote, ask the right questions, and watch your affordable IUL policy for single parents become a cornerstone of a brighter future.