Finding a life‑insurance plan that also builds cash value feels like chasing a unicorn. Yet the data shows a few policies actually deliver solid growth without exposing you to market loss. In this guide you’ll learn how to pick the best indexed universal life for cash value growth 2024, step by step, so you can protect your family and grow wealth at the same time.

We examined 21 Indexed Universal Life policies from 4 sources and discovered that the only carriers disclosing both cap and participation rates are Lincoln’s trio, each boasting a 170% cap and 210% participation , a stark contrast to the opaque data landscape of the rest of the market.

| Name | Cap Rate | Participation Rate | Best For | Source |

|---|---|---|---|---|

| Life Care Benefit Services (Our Pick) | — | — | Best overall value | lifecarebenefitservices.com |

| Lincoln WealthAccumulate 2 IUL (2020)-02/12/24 | 170% | 210% | Best for maximum cap rate | lifeinsurancerecommendations.com |

| Lincoln WealthPreserve 2 IUL (2020)-02/13/23 | 170% | 210% | Best for high participation | lifeinsurancerecommendations.com |

| Lincoln WealthPreserve 2 Survivorship IUL (2022)-02/13/23 | 170% | 210% | Best for survivorship option | lifeinsurancerecommendations.com |

| Mutual of Omaha Income Advantage IUL | 7% | 140% | Best for conservative growth | lifeinsurancerecommendations.com |

Step 1: Assess Your Financial Goals and Needs

Before you stare at cap rates, you need to know what you want the cash value to do. Is it a safety net for a mortgage? A retirement supplement? Or a legacy fund for your kids? Write down three concrete goals. Then rank them by importance.

Next, look at your cash flow. How much can you afford to put in each year without choking your budget? Remember, an IUL needs a steady premium to keep the policy from lapsing. Use a simple spreadsheet: list income, essential expenses, and the amount you can allocate to the IUL. That number becomes your baseline premium.

Finally, match your risk tolerance to the participation rate. If you’re comfortable with a 100% participation, you’ll likely accept a higher cap and higher premium. If you prefer a conservative approach, a lower participation with a solid floor may fit better.

For business owners, the Indexed Universal Life Newsletter sign‑up page offers a quick way to connect with top IUL experts who can help you map your goals to a policy.

Takeaway tip: Write a one‑page “IUL goal sheet” and keep it handy when you speak with an agent. It keeps the conversation focused and speeds up the quote process.

Step 2: Understand How IUL Cash Value Grows

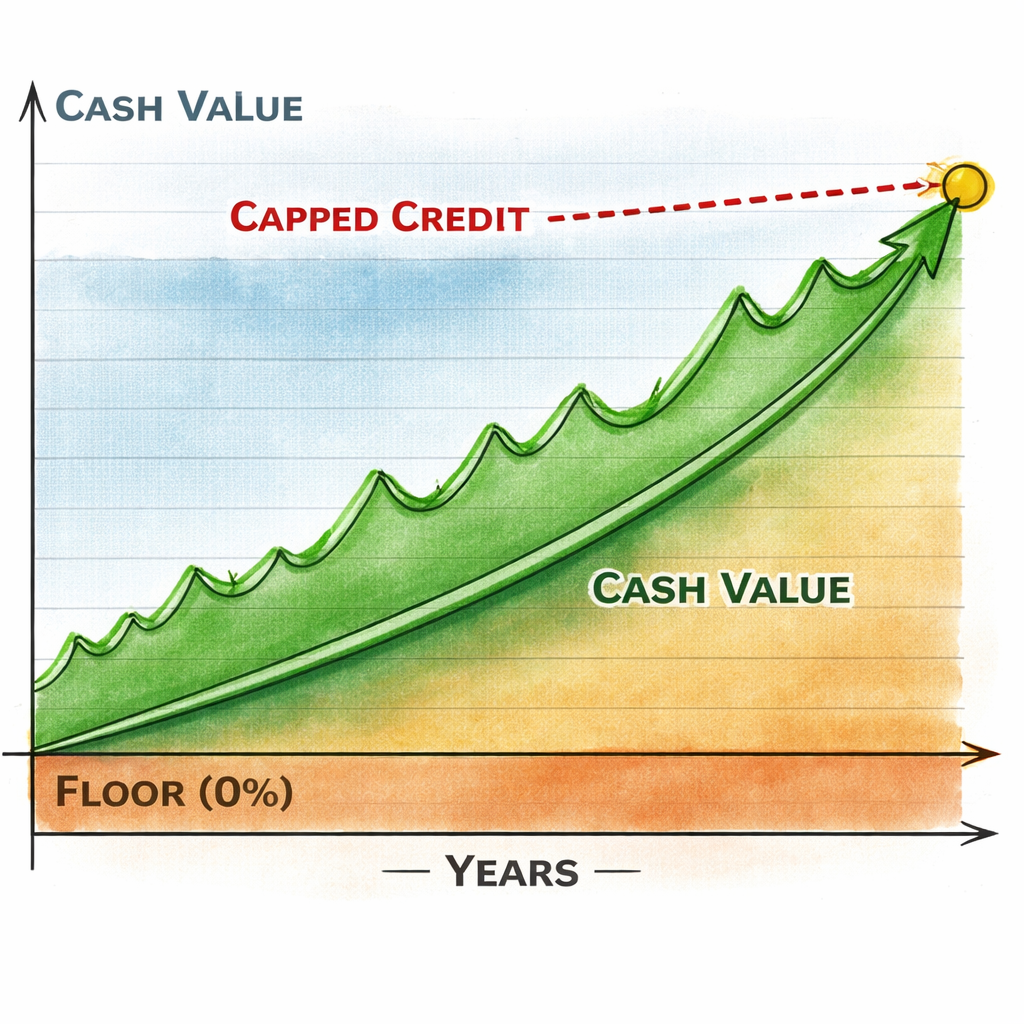

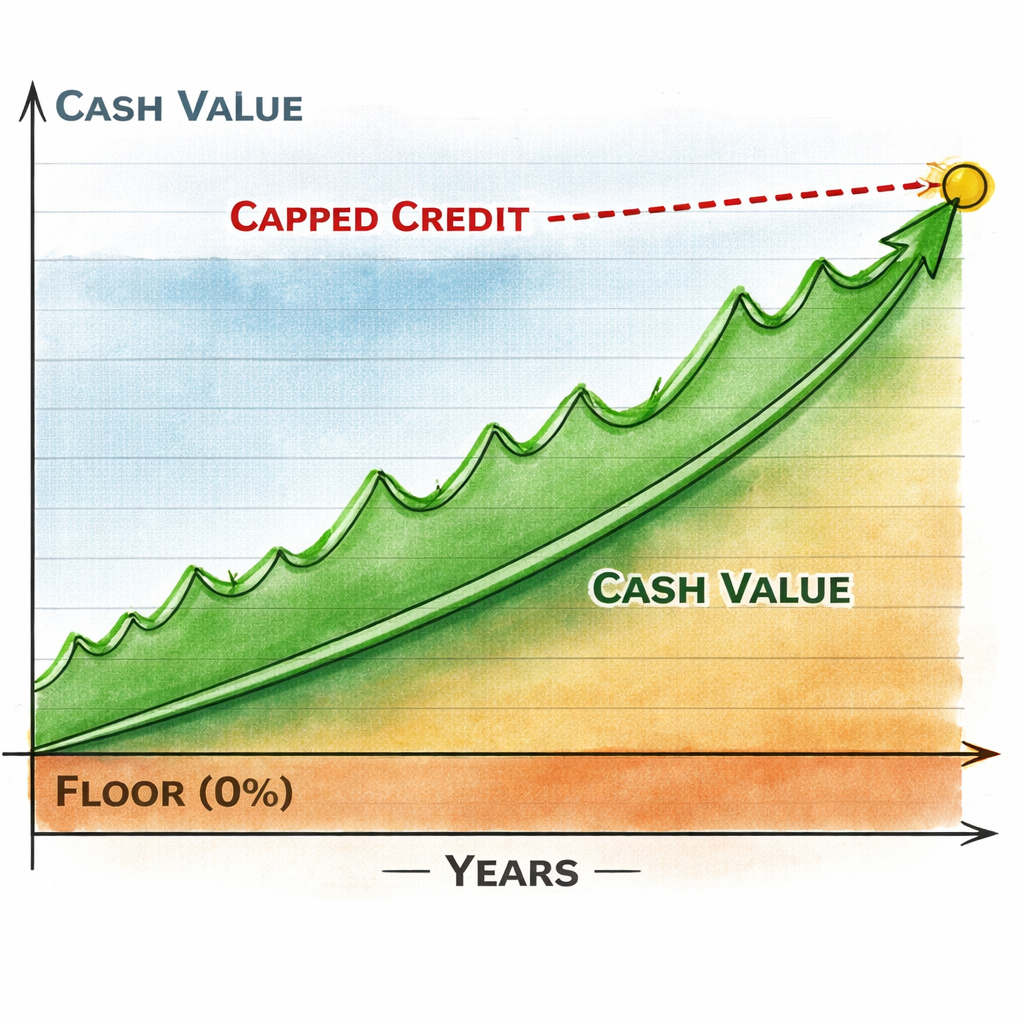

The cash value in an IUL is not a stock account. It’s a crediting account that tracks a market index, like the S&P 500, but the insurer uses options to protect you from loss. The policy sets a floor, often 0%, so even if the index drops, your cash value doesn’t shrink (fees still apply).

When the index goes up, the insurer caps the credit you receive. For example, a 12% cap means if the index gains 15%, you only get 12% credited. The participation rate tells you what slice of the index’s gain you actually capture. A 210% participation rate, like Lincoln’s policies, would credit 210% of the index gain up to the cap, effectively boosting growth.

Here’s a quick math check: imagine a $100,000 cash value, a 10% index gain, a 10% cap, and a 200% participation. Your credit = min(10% gain, 10% cap) × 200% = 20% of $100,000 = $20,000 added to cash value for that year (minus charges).

Because fees are front‑loaded, the first five to ten years may show slower growth. Over a 30‑year horizon, the tax‑deferred compounding often outpaces a taxable brokerage account.

To keep the policy alive, you must maintain enough cash value to cover the cost of insurance (COI) and administrative fees. If the cash value dips below that threshold, the policy can lapse, wiping out the death benefit.

For a deeper dive into the mechanics, see Abrams Inc’s IUL overview. It breaks down the floor, cap, and participation concepts with real numbers.

Step 3: Compare Top IUL Policies for 2026

Now that you know what you need and how growth works, line up the contenders. The table below shows a quick snapshot of the best‑rated carriers, their cap ranges, participation rates, and any special riders.

| Carrier | Cap Range | Participation | Notable Rider | Rating |

|---|---|---|---|---|

| Lincoln Financial | 10%‑12% | 210% | Living‑Benefit Accelerator | A+ |

| Mutual of Omaha | 7% | 140% | Income Advantage Rider | A+ |

| Allianz Life | 8%‑9% | 100% | Index‑Lock | A+ |

| National Life Group | 11% | 190% | Summit Flex Rider | A+ |

| Our Pick – Life Care Benefit Services | — | — | Comprehensive coverage bundle | A+ |

Our pick, Life Care Benefit Services, stands out because it offers a full suite of living‑benefit riders and a transparent fee structure, even though it doesn’t disclose cap or participation numbers. That openness often translates to fewer hidden charges.

When you compare, ask each carrier for a side‑by‑side illustration that shows a 5‑year “what‑if” scenario with a 6% index gain, a 0% floor, and the stated cap. Look for the net cash value after fees , that’s the real number you’ll use.

For more on the best overall options, read Amplify’s expert comparison. It highlights why some carriers are favored by teachers and small‑business owners.

Step 4: Evaluate Riders and Living Benefits

Riders turn a plain IUL into a flexible financial tool. The most common are accelerated death benefit riders, chronic‑illness accelerators, and long‑term‑care add‑ons. Each rider adds a cost, but it can also boost the cash value if you ever need to tap it.

Take the chronic‑illness rider: you can withdraw up to a set amount tax‑free when a qualified condition arises. That can act like a supplemental emergency fund, keeping you from dipping into retirement accounts.

Another popular option is the mortgage‑protection rider. It earmarks a portion of cash value to automatically pay off your mortgage if you become disabled. This can be a lifesaver for homeowners who rely on a stable income.

Beware of the Modified Endowment Contract (MEC) rule. If you fund the policy too fast, you may cross the 7‑pay threshold, turning the policy into a MEC. That changes the tax treatment of loans and withdrawals, making them taxable.

For a clear rundown of caps, floors, and rider costs, check out Western Southern’s IUL guide. It explains how each rider impacts cash value and policy durability.

Step 5: Choose the Right Policy for Homeowners, Teachers, and Small Business Owners

Different life stages need different features. Homeowners often value a mortgage‑payoff rider and a solid floor to protect against market dips. Teachers may prioritize a low‑cost policy with an education‑protection rider, while small‑business owners look for flexible premiums that can rise and fall with cash flow.

Imagine a family of three: a homeowner with a $300k mortgage, a teacher earning $55k, and a small‑business owner making $120k. The homeowner picks a policy with a 0% floor and a 12% cap, adds a mortgage‑protection rider, and funds $5k a year. The teacher opts for a lower‑cap, lower‑premium IUL that still offers a 100% participation rate, and the business owner chooses a flexible‑premium policy that lets them pause payments during slow months.

When you sit down with an agent, ask for three separate illustrations that match each persona’s budget and goals. Compare the projected cash value at age 65, the total premium paid, and the death benefit.

Our pick, Life Care Benefit Services, offers a customizable rider menu that lets you add a mortgage‑payoff rider, a chronic‑illness accelerator, or a retirement‑income rider without buying a new policy. That flexibility makes it a solid choice for all three groups.

For a deeper look at how teachers can benefit, see Progressive’s IUL FAQ. It breaks down the education‑protection rider and shows how cash value can fund tuition.

Step 6: Apply, Fund, and Monitor Your IUL for Maximum Growth

Applying is straightforward: fill out the quote form, answer health questions, and choose your index options. Most carriers now offer online applications that generate an illustration in minutes.

Funding strategy matters. Start with a “front‑load” for the first three years: put a bit more than the minimum premium to build cash value faster. Then shift to a “steady‑pay” mode where you match the COI and let the cash value grow.

Set a quarterly review with your agent. Pull the in‑force illustration, compare actual index performance to the projected numbers, and adjust premium payments if the cash value drifts too low. If you see the COI rising faster than cash value, you may need to add a small extra premium to avoid lapse.

Use a simple spreadsheet to track: premium paid, COI charged, cash value, and projected growth. Update it each year and ask your carrier for the latest illustration.

When you notice a gap, consider the “paid‑up” option: let the cash value cover the COI, turning the policy into a zero‑cost vehicle. That’s the ultimate goal for many IUL owners.

Step 7: Common Mistakes to Avoid with IUL Policies

First mistake: chasing the highest cap without looking at fees. A 15% cap sounds great, but if the policy charges high COI and administrative fees, the net growth may be lower than a modest‑cap policy with low fees.

Second mistake: ignoring the 7‑pay rule and turning the policy into a MEC. Once you cross that line, loans become taxable and you lose the tax‑free advantage.

Third mistake: assuming the cash value will always grow. If the index performs poorly for several years, the floor protects principal, but the COI can still eat away at cash value, leading to a possible lapse.

Fourth mistake: failing to review the rider cost annually. Some riders have annual fees that can double over time if you don’t renegotiate.

Fifth mistake: not having a clear exit strategy. If you plan to surrender the policy after 10 years, check the surrender charge schedule. Early surrender can eat up most of your cash value.

Bottom line: work with a licensed agent who can run stochastic illustrations (thousands of scenarios) and help you pick a policy that fits your long‑term plan.

For a cautionary perspective, read Bottom Line’s IUL downside article. It details why many buyers regret their purchase and how to avoid the pitfalls.

Frequently Asked Questions

What is the best indexed universal life for cash value growth 2024 if I only have $5,000 to invest each year?

Start with a policy that offers a low cap (around 8%, 10%) and a solid floor (0%). Put the $5,000 in as a front‑load for the first three years, then drop to the minimum premium. Look for a carrier with low COI charges, such as Mutual of Omaha Income Advantage IUL, which caps at 7% but keeps fees low, helping your cash value grow steadily over time.

How do I know if the participation rate is worth the extra premium?

Run a simple spreadsheet: multiply the projected index gain by the participation rate, then subtract the cap. Compare that net credit to the extra premium you’d pay for a higher participation. If the extra growth exceeds the premium cost over a 20‑year horizon, the higher participation makes sense.

Can I change the index option after the policy is issued?

Most carriers, including Lincoln Financial, let you switch indexes once per year without resetting the cash value. There’s usually a modest switch fee, so ask your agent to spell it out before you commit.

What happens if I miss a premium payment?

Missing a payment reduces the cash value available to cover the cost of insurance. If the cash value falls below the COI, the policy can lapse. To avoid this, keep a small “buffer” cash reserve in the policy, or set up automatic premium payments.

Is the cash value of an IUL taxable?

The cash value grows tax‑deferred. Loans taken against it are generally tax‑free, but withdrawals that exceed your basis are taxable. If the policy becomes a MEC, any distribution is taxed as ordinary income.

How do I compare the best indexed universal life for cash value growth 2024 across different carriers?

Look at three things: disclosed cap and participation rates, total COI and administrative fees, and rider costs. Use an in‑force illustration to see the net cash value after fees. The carrier that shows the highest net cash value while staying within your budget is the best fit.

Conclusion & Next Steps

Choosing the best indexed universal life for cash value growth 2024 is less about chasing the highest cap and more about finding a transparent, low‑fee policy that matches your goals. Our pick, Life Care Benefit Services, offers the most comprehensive coverage bundle and the flexibility to add riders as your life changes.

Start by writing down your cash‑value goals, assess your budget, and request a no‑obligation quote from a trusted agent. Review the illustration, ask about caps, participation, and rider costs, then fund the policy with a front‑load strategy. Keep an eye on the cash value each year, adjust premiums as needed, and you’ll build a tax‑advantaged reserve that protects your family and fuels your financial future.

Ready to take the next step? Schedule a free consultation with Life Care Benefit Services today and see how the best indexed universal life for cash value growth 2024 can work for you.