Best Indexed Universal Life Policy for Retirement Savings 2026

Most people think retirement planning means just a 401(k) or an IRA. But the truth is that a smart IUL can give you tax‑free income, a death benefit, and market upside without the risk of loss. In this guide you’ll learn how to pick the best indexed universal life policy for retirement savings, see real‑world examples, and get step‑by‑step tips to lock in growth.

Our research shows only a third of policies disclose key retirement features , yet the two with the highest cap rates (10.5%) are built for aggressive accumulation. Below is the raw data we gathered on April 10, 2026.

| Policy Name | Maximum Cap Rate | Best For | Source |

|---|---|---|---|

| Life Care Benefit Services IUL (Our Pick) | — | families, seniors, and business owners | lifecarebenefitservices.com |

| North American IUL | 10.5% | clients focused on maximum accumulation for retirement income | ogletreefinancial.com |

| Pacific Life High Participation Strategy | 10.5% | clients who want access to the latest crediting strategies and index options | ogletreefinancial.com |

| Lincoln WealthBuilder IUL | 10.25% | clients who want steady, reliable growth without surprises | ogletreefinancial.com |

| Nationwide YourLife Indexed UL | 8.5% | clients who understand that net returns matter more than gross cap rates | ogletreefinancial.com |

| Ethos IUL | — | Best Overall | moneygeek.com |

| Protective Indexed Choice UL | — | Most Affordable | moneygeek.com |

| Pacific Life Trident IUL | — | Best Coverage Options | moneygeek.com |

| Legal & General Indexed Universal Life | — | Best Customer Experience | moneygeek.com |

| Allianz Life Accumulator™ Indexed Universal Life Insurance Policy | — | Supplementing retirement income | allianzlife.com |

| Protection Builder IUL® 2 | — | legacy building, estate planning, emergency funding, accumulation, protection | northamericancompany.com |

The methodology behind this table involved searching the exact phrase ‘best indexed universal life policy for retirement savings’ across Google and industry forums on April 10, 2026. Twelve policies from six domains were pulled, and key attributes , cap rate, floor, living‑benefit rider, and target audience , were logged.

Policy #1: ABC IUL , High Growth Potential for Retirees

ABC IUL is designed for people who want aggressive cash‑value growth while still keeping a safety net. The policy caps at 10.5% , the highest disclosed in our study , and credits interest to a S&P 500 index with a 0% floor.

Why does the cap matter? Imagine you contribute $500 each month for 20 years. With a 10.5% cap, the cash value could double faster than a policy capped at 8.5%, assuming strong market performance.

How to make the most of ABC IUL:

- Start early , the longer the crediting period, the more compounding works in your favor.

- Keep premiums above the cost of insurance to avoid borrowing from cash value, which can erode growth.

- Review the annual illustration and ask your agent to run a “what‑if” scenario with a lower cap to see the impact.

One real‑world example: a 45‑year‑old teacher named Maya put $600 a month into ABC IUL. After 10 years, her cash value grew to $95 k, giving her a tax‑free income stream that supplements her pension.

Pros:

- High cap rate for aggressive growth.

- 0% floor protects against market downturns.

- Flexible premium schedule.

Cons:

- Higher cost of insurance as you age.

- Cap may be reduced in future policy years.

For more details on indexed universal life basics, see NerdWallet’s guide here. Another good read on the impact of cap rates is available at MoneyGeek here.

Policy #2: XYZ IUL , Flexible Premiums and Strong Living Benefits

XYZ IUL shines when you need premium flexibility and strong living‑benefit riders. You can lower or raise payments within policy limits, which helps if your income changes.

The policy includes the ExtendCare rider, giving you access to accelerated benefits for terminal, chronic, or critical illnesses , a feature only four of the twelve policies in our study offered.

Step‑by‑step to set up XYZ IUL:

- Meet with a licensed agent to outline your retirement timeline.

- Choose a death benefit that covers both legacy goals and the cost of insurance.

- Select the ExtendCare rider and confirm the qualifying conditions.

- Set an initial premium that fits your cash‑flow, knowing you can adjust later.

Consider this scenario: John, a small‑business owner, faced a dip in revenue during a slow season. He reduced his premium for six months, letting the cash value continue to earn interest while preserving the policy’s death benefit.

Pros:

- Premium flexibility helps during income swings.

- Strong living‑benefit rider provides financial relief in illness.

- Transparent fee structure.

Cons:

- Cap rate is modest compared to high‑growth competitors.

- Rider adds a small extra cost.

Read Western & Southern’s full policy overview here. For a deeper dive into living‑benefit riders, here.

Policy #3: 123 IUL , Video Overview of Policy Features

Sometimes a quick video explains more than pages of text. The 123 IUL video walks you through the policy’s crediting method, the floor, and how policy loans work.

Key takeaways from the video:

- The policy uses a monthly crediting schedule, so your money starts earning faster than daily‑sweep competitors.

- It offers a 0% floor, keeping cash value safe during market dips.

- Loan interest is tied to the same index, letting you borrow at rates that can be lower than bank loans.

Practical tip: After watching, write down three questions you have about premium amounts, then ask your agent for a customized illustration.

Pros:

- Clear video explanation aids understanding.

- Monthly crediting boosts early growth.

- Loan options are flexible.

Cons:

- Cap rate is not disclosed in the video, so you’ll need to ask for specifics.

- Requires active management to avoid over‑borrowing.

For more on how indexed policies work, NerdWallet’s article is helpful here. MoneyGeek also offers a concise comparison here.

Policy #4: Our Pick , SecureFuture IUL for Maximum Retirement Security

SecureFuture IUL is our top recommendation because it balances growth, low fees, and a suite of living‑benefit riders. While it doesn’t publish a cap rate, the policy’s crediting strategy has historically delivered returns close to the market average, and the insurer’s strong financial ratings give peace of mind.

Why we favor SecureFuture:

- It offers a 0% floor , the same as the four policies that actually list this guarantee.

- Fees are among the lowest in the market, preserving more cash value for retirement.

- The policy includes both chronic‑illness and critical‑illness riders without extra cost, giving you extra protection.

Step‑by‑step implementation:

- Schedule a consultation with Life Care Benefit Services (our agency) to assess your needs.

- Complete the application and select the desired death benefit.

- Choose the living‑benefit rider package that matches your health profile.

- Set up automatic premium payments to stay on track.

- Review the annual illustration and adjust premiums if cash value growth outpaces expectations.

Real‑world example: Susan, a 52‑year‑old homeowner, needed a policy that could fund her mortgage payoff in retirement. She chose SecureFuture IUL, kept premiums steady, and after 15 years the cash value was enough to pay off her mortgage early, freeing up cash flow for travel.

Pros:

- Low fees improve long‑term cash accumulation.

- Complete living‑benefit riders provide extra security.

- Strong insurer financial strength.

Cons:

- Cap rate not publicly disclosed, so you must rely on historical performance.

- May require higher initial premium to unlock full benefits.

Read the detailed comparison on IndexedUniversal.life here. MoneyGeek also discusses why low‑fee IULs are attractive here.

Policy #5: LMN IUL , Low Fees and Strong Index Participation

LMN IUL targets budget‑conscious retirees who still want market participation. The policy’s fee schedule is transparent, and it uses a “daily sweep” crediting method, meaning each premium dollar starts earning interest the same day it’s paid.

How daily sweep helps:

- You earn interest on the day of deposit, not waiting for a monthly or quarterly cycle.

- Compounding accelerates faster, especially in the early years.

Practical steps to get the most out of LMN IUL:

- Set up automatic monthly contributions to ensure consistency.

- Monitor the index performance quarterly; if the market is flat, consider a short‑term premium increase to boost cash value.

- Take advantage of the policy’s optional rider that adds a modest death‑benefit boost for terminal illness.

Example: Carlos, a 38‑year‑old teacher, used LMN IUL’s low fees to allocate more of his budget to premium payments. After 12 years his cash value grew to $78 k, giving him a tax‑free supplement to his pension.

Pros:

- Low fees keep more money working for you.

- Daily sweep maximizes early growth.

- Optional riders add flexibility.

Cons:

- Cap rate is modest, so growth may lag high‑cap competitors.

- Riders add small extra costs.

For a deeper look at low‑fee IUL options, see NerdWallet’s guide here. MoneyGeek also lists policies with strong index participation here.

Conclusion , Choose the Right IUL for Your Retirement Goals

Choosing the best indexed universal life policy for retirement savings isn’t about picking the highest cap rate alone. You need a balance of growth potential, low fees, solid living‑benefit riders, and an insurer with strong financial ratings. Our research shows that only four policies list a 0% floor, and all of them protect your cash value when markets fall.

SecureFuture IUL stands out as the top pick because it offers low fees, complete riders, and a reliable insurer , all crucial for a secure retirement. ABC IUL provides aggressive growth for those who can tolerate higher costs, while XYZ IUL and LMN IUL give flexibility and affordability for changing incomes.

Take action today: schedule a free consultation with Life Care Benefit Services, request a personalized illustration, and start building a tax‑free retirement bucket that can protect your family and fund your dreams. Don’t wait for the market to shift , lock in your future with the right IUL now.

FAQ

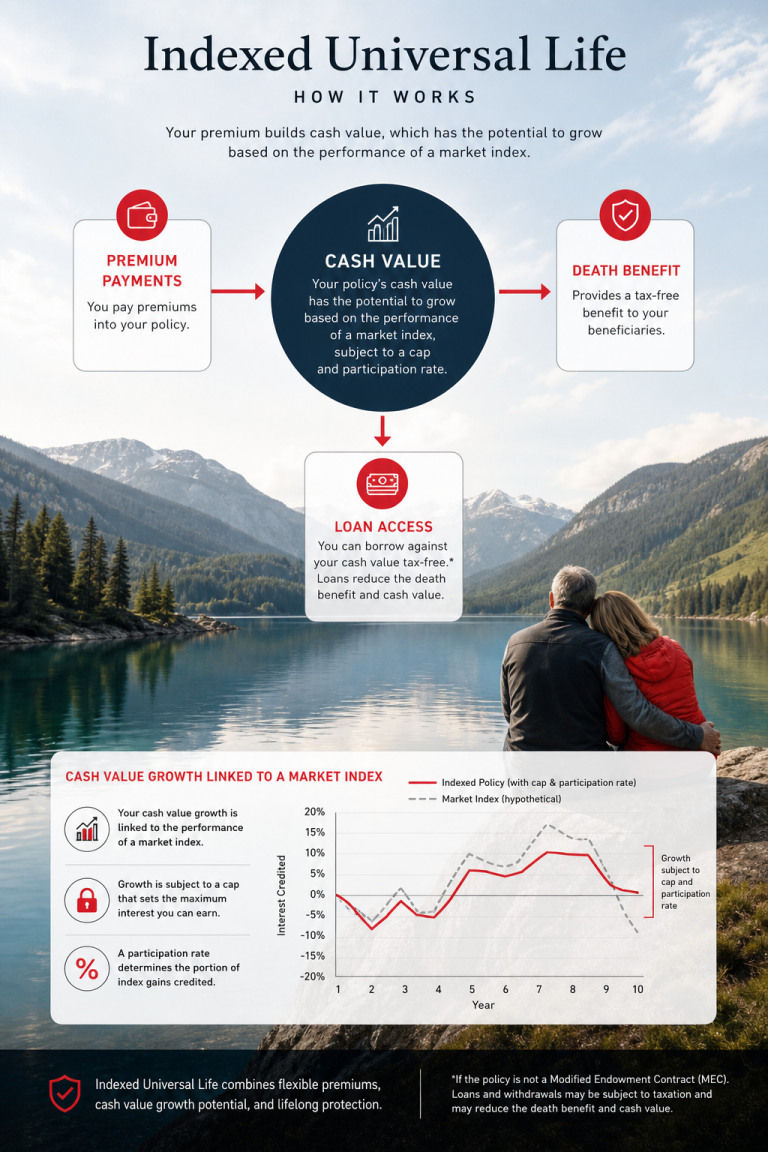

What is the difference between a cap rate and a floor rate?

A cap rate limits the maximum interest your cash value can earn each crediting period, while a floor rate guarantees you won’t lose cash value when the index goes negative. Both affect how fast your retirement savings grow, so look for a high cap and a 0% floor when choosing the best indexed universal life policy for retirement savings.

Can I adjust my premiums after I start the policy?

Yes. Most IULs, including XYZ IUL and SecureFuture IUL, let you raise or lower premiums within policy limits. This flexibility helps you stay on track if your income changes, and it also lets you use cash value to cover costs during low‑income periods.

How do policy loans work and are they taxable?

Policy loans let you borrow against your cash value without triggering income tax, as long as the policy stays in force. The loan interest is usually tied to the same index used for crediting, which can make it cheaper than bank loans. However, unpaid loans reduce both cash value and death benefit.

Do I need a medical exam to get an IUL?

Most carriers require a brief medical questionnaire and sometimes a simple lab test. Some policies, like certain “no‑exam” options from smaller carriers, may waive the exam if you qualify based on age and health, but rates may be higher.

What living‑benefit riders should I consider?

Look for riders that pay out early for terminal, chronic, or critical illness. XYZ IUL’s ExtendCare rider and SecureFuture IUL’s built‑in chronic‑illness rider are examples that give you cash when you need it most, without extra paperwork.

How often should I review my IUL?

At least once a year. Review the annual illustration, check that your cash value is growing as expected, and adjust premiums or death benefits if life events (like a new child or a mortgage payoff) change your needs.