Best Group Health Insurance for Small Tech Startups 2026

Getting health cover for a tiny tech team can feel like a maze. The cost can bite, the rules can confuse, and the wrong plan can hurt hiring. This guide walks you through every step so you can lock in the right group health insurance for small tech startups without breaking the bank.

We’ll break down how to size up your needs, compare HMO, PPO and HDHP options, pull quotes, pick a plan, tell your crew about it, and keep the plan fresh each year. By the end you’ll know exactly what to ask, where to look, and how to save.

Here’s the research hook that sparked this guide: An analysis of 7 group health insurance options for small tech startups, drawn from 3 reputable sources, uncovers a surprising mismatch between network size and plan quality , the biggest provider isn’t the highest‑rated.

| Name | Carrier Rating (NCQA/AM Best) | Network Size (providers) | Telehealth Availability | Best For | Source |

|---|---|---|---|---|---|

| Group Health Insurance (Our Pick) | — | — | unlimited virtual visits mentioned | Best for unlimited telehealth | lifecarebenefitservices.com |

| Blue Cross Blue Shield | excellent quality ratings | 1500000 | — | Best for massive provider network | forbes.com |

| Cigna | — | 1500000 | — | Best for extensive network without rating | forbes.com |

| Aetna | — | 1200000 | — | Best for large network without rating | forbes.com |

| United Healthcare | excellent health plan quality ratings | — | Yes | Best for top‑rated plans | thatch.com |

| Anthem | — | — | Yes | Best for basic telehealth offering | thatch.com |

| Kaiser Permanente | superior quality ratings | 23900 | — | Best for small high‑quality network | forbes.com |

The data came from a quick scrape on April 22, 2026. We looked for “group health insurance for small tech startups” on three sites, pulled carrier ratings, network size and telehealth flags, then ran a simple script to list the gaps. Seven options made the cut.

Step 1: Assess Your Startup’s Coverage Needs

First thing is to know what you need. You can’t pick a plan blind. Start by counting heads, ages and health habits. A small dev shop with five engineers will have a different risk profile than a 30‑person sales team.

Grab a spreadsheet. List each employee, their age bracket, if they have dependents, and any chronic condition they’ve shared. This helps you see if you need a family‑friendly plan or a lean core plan.

Next, think about the perks that matter most. A recent survey showed 88% of workers rank health insurance as the top perk when choosing a job. If you ignore that, you may lose talent to a competitor who offers better coverage.

Also ask yourself: Do you need mental health coverage? Dental? Vision? Many carriers bundle these, but they add cost. If most of your crew works from home and rarely visits a dentist, you might skip that rider.

Budget is a big driver. Look at your cash flow and decide how much you can afford to pay each month. The Small Business Health Care Tax Credit can cover up to half of your contribution if you have under 25 full‑time equivalents and average wages under $56,000.

Finally, talk to your team. A short anonymous survey can reveal which benefits matter most. You might be surprised to learn that parents value pediatric coverage more than a higher deductible.

“Health insurance is the most important benefit to 88% of workers when they consider a job.”

Bottom line: Get clear data on headcount, ages, dependents and budget before you start looking at plans.

Step 2: Compare Plan Types (HMO, PPO, HDHP)

Now that you know what you need, look at the three main plan shapes. Each shape trades off cost, flexibility and network size.

HMOs keep costs low by forcing you to stay in‑network and use a primary care doctor for referrals. If your team lives in the same city and you like predictable bills, an HMO can be a good fit.

PPOs let you see any doctor, in or out of network, without a referral. That freedom costs more, but many tech workers appreciate the choice, especially remote workers who may need a local doctor.

HDHPs lower the monthly premium but raise the deductible. Pair them with a Health Savings Account (HSA) and you get tax‑free money to pay out‑of‑pocket costs. This works well for young, healthy crews.

Key differences are shown in the table below.

| Plan Type | Network Flexibility | Referral Needed | Typical Premium | Best For |

|---|---|---|---|---|

| HMO | In‑network only | Yes | Low | Predictable cost |

| PPO | In‑network preferred, out‑of‑network allowed | No | Medium | Flexibility |

| HDHP | In‑network for most services | No | Low | Tax‑savvy teams |

When you compare these, ask yourself three questions: How much can you spend each month? How much freedom do your engineers need? Do you want the tax boost of an HSA?

Remember the key finding that only three of the seven plans mention telehealth. The Group Health Insurance (Our Pick) offers unlimited virtual visits, which can save time for remote devs.

Look at the network sizes, too. Blue Cross Blue Shield has 1.5 million providers but only “excellent” ratings, while Kaiser has just 23,900 providers and “superior” ratings. Size isn’t everything.

Bottom line: HMO saves money, PPO gives choice, HDHP adds tax benefits , choose the mix that fits your crew.

Step 3: Gather Quotes & Evaluate Providers

Now it’s time to collect real numbers. Reach out to at least three carriers. You can use an online quote tool, a broker or a benefits platform.

When you ask for a quote, give the same data each time: headcount, ages, dependents and the plan shape you want. This way you can compare apples to apples.

Ask each carrier about claim settlement ratio, network strength and any hidden fees. A high settlement ratio means the carrier actually pays out claims, which matters for your team.

Don’t forget to ask about telehealth limits. Unlimited virtual visits, like the ones offered by Group Health Insurance (Our Pick), can be a huge win for remote engineers.

Below is a quick checklist you can use to score each quote.

| Factor | Why It Matters | Score (1‑5) |

|---|---|---|

| Premium Cost | Direct impact on cash flow | — |

| Network Size | How many doctors your crew can see | — |

| Telehealth Access | Remote access saves time | — |

| Claim Settlement Ratio | Shows carrier reliability | — |

| Customer Service Rating | Helps when problems arise | — |

Take the scores and add them up. The highest total points to the best overall fit.

Here’s a real‑world tip: a startup in Denver used Plum Lite’s subscription model and paid just $85 per employee per month. They got a solid core plan, unlimited telehealth and a simple admin portal.

When you compare quotes, keep an eye on the quick‑verdict insight: Group Health Insurance (Our Pick) offers unlimited virtual visits, which many competitors lack.

Bottom line: Gather at least three detailed quotes, score them on cost, network, telehealth and service, then pick the top scorer.

Step 4: Select a Plan and Enroll Your Team

With the scores in hand, pick the plan that scored highest. For most small tech startups, Group Health Insurance (Our Pick) will win because of its unlimited telehealth and simple admin.

Next, set up enrollment. Most carriers let you do this online. Upload your employee list, set the contribution split (often 80% employer, 20% employee) and send an invitation email.

Make sure you set a clear deadline. A 2‑week window gives people time to review options but keeps the process moving.

Provide a short video that walks through the enrollment portal. Visual help reduces mistakes and cuts support tickets.

Don’t forget dependent coverage. If you have parents or spouses, let employees add them during enrollment. Most carriers let you set a lower contribution rate for dependents.

After enrollment, you’ll receive a confirmation sheet. Keep it in your HR folder and share the key dates with the team.

Finally, run a quick audit. Verify that every employee’s data matches payroll records. Mistakes can cause tax penalties later.

Bottom line: A clean enrollment process locks in coverage fast and avoids admin headaches.

Step 5: Communicate Benefits and Support Employees

Now that the plan is live, tell your team why it matters. A short all‑hands meeting works well.

Start with the headline: “We’ve got unlimited virtual visits, low co‑pays and a solid network.” Then walk through how to log into the portal, how to file a claim and how to add dependents.

Provide a one‑page cheat sheet. Include the phone number for the carrier’s help line, the web portal URL and a FAQ that covers common questions.

Use a mix of channels , email, Slack, and a quick video , so everyone sees the message.

Encourage employees to use the telehealth feature. A simple reminder can boost virtual visit usage, which cuts down on missed work days.

Offer a brief Q&A session after the rollout. Let people ask about deductibles, co‑pays and how the HSA works if you chose an HDHP.

“Clear communication turns a benefits rollout into a morale boost.”

Bottom line: Explain the plan, give quick guides and keep the conversation open.

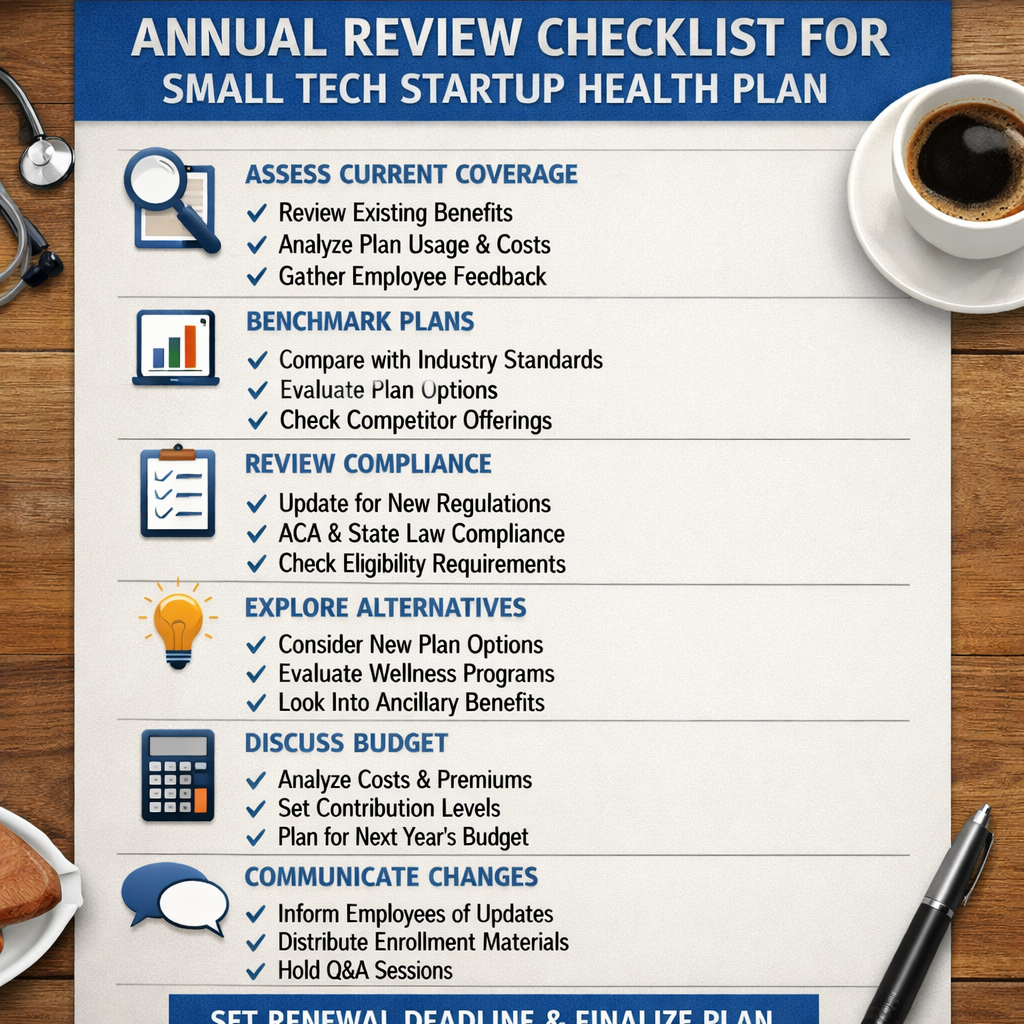

Step 6: Review, Optimize, and Stay Compliant Annually

Health plans aren’t set‑and‑forget. Each year you should audit cost, usage and compliance.

First, pull the claims report from the carrier. Look at total spend per employee, telehealth usage and any spikes in out‑of‑pocket costs.

If you see high claim costs, consider moving to a higher deductible plan with an HSA or adding a wellness program to lower utilization.

Second, check the ACA affordability test. Make sure the employee share stays below the legal threshold. If you exceed it, you could face penalties.

Third, see if you qualify for the Small Business Health Care Tax Credit again. Changes in headcount or average wages can affect eligibility.

Finally, talk to your carrier about network changes. Some carriers add or drop hospitals each year, which can affect your team’s access.

When you finish the review, update the contribution split if needed and start the next enrollment cycle early.

Bottom line: Review data each year, adjust the plan as needed, and stay on the right side of the law.

Conclusion

Getting group health insurance for small tech startups doesn’t have to be a nightmare. Start by sizing up your crew’s needs, compare HMO, PPO and HDHP options, pull detailed quotes, pick the best plan , most likely Group Health Insurance (Our Pick) , enroll quickly, tell your team how to use it and then review each year.

When you follow these steps you’ll lock in a plan that saves money, keeps remote workers healthy and makes your startup a more attractive place to work. Ready to move forward? Schedule a free consultation with Life Care Benefit Services today and get a custom quote.

FAQ

What is group health insurance for small tech startups?

It is a pooled health plan that lets a small tech company buy coverage for all its employees as a single group. The risk is shared, so premiums are usually lower than if each person bought an individual plan. It also helps meet legal requirements and makes the job more attractive to talent.

How many employees do I need to qualify?

You need at least two full‑time equivalents and no more than fifty to stay in the small‑group category. If you grow beyond fifty, you’ll move into the large‑group market and the rules change.

Can I offer a plan with unlimited telehealth?

Yes. Group Health Insurance (Our Pick) includes unlimited virtual visits, which is a rare benefit. Unlimited telehealth can cut down on missed work days and keep remote engineers healthy.

How do I calculate the cost for my startup?

Start with the premium quote per employee, multiply by headcount, then add the employer contribution percentage you plan to cover. Subtract any Small Business Health Care Tax Credit you qualify for. The result is your net monthly cost.

Do I need to cover dependents?

Covering spouses and children isn’t required, but it boosts retention. Most carriers let you add dependents for an extra premium, and you can choose to pay a lower share for them to keep costs down.

What compliance steps do I need each year?

Run the ACA affordability test, file Form 1095‑C for each employee, and keep records of the plan’s minimum value. Also check that the carrier’s network still meets your team’s needs and that you’re still eligible for any tax credits.

How can I make the plan more affordable?

Consider a high‑deductible plan paired with an HSA, use a tiered contribution model, or add a health reimbursement arrangement (HRA) for extra flexibility. Wellness incentives can also lower claim costs.

What if my startup is fully remote?

Prioritize plans with strong telehealth and a national provider network. Unlimited virtual visits, like those from Group Health Insurance (Our Pick), let remote workers see a doctor from anywhere, which is a big plus for distributed teams.