Thinking about retirement income strategies with annuities? You’re not alone. It’s one of those topics that can feel a bit overwhelming—like trying to solve a puzzle without all the pieces. But what if I told you annuities might be one of the most straightforward tools in your retirement toolkit?

Here’s the thing: many folks wonder how to make sure their money lasts as long as they do. You know that nagging fear of running out of cash or being hit by unexpected expenses? Yeah, that’s exactly why retirement income planning is so crucial.

Retirement income strategies with annuities can help take some of that uncertainty off your plate. They’re kind of like a personal paycheck that you set up in advance—guaranteeing income no matter how long you live. Sounds good, right? But, not all annuities are created equal, and that’s where things can get tricky.

So, what should you do next? First, it’s worth understanding the different types of annuities and how they fit into your overall plan—because it’s not just about locking your money away. It’s about crafting a strategy that balances growth, security, and flexibility so you actually feel confident stepping into retirement.

Maybe it’s just me, but when I hear the word “annuity,” I think of something complex and dull. But when broken down, it’s really just a promise of steady income, which our future selves will be grateful for. And with the right approach, you don’t have to surrender control or deal with confusing fine print.

Before diving deeper, consider this: balancing guaranteed income with other retirement resources like savings or social security can paint a clearer picture of your financial future. If you’re curious about exploring further, our experts at Life Care Benefit Services have helped many families and individuals put together robust retirement income strategies.

Don’t let the planning paralysis keep you from securing your peace of mind. Take the first step today by learning more about the options that fit your unique needs—you can start by checking out how reviewing your existing policies can open doors you didn’t see before. Let’s dive in and make retirement something to look forward to, not fear.

TL;DR

Retirement income strategies with annuities can offer steady, predictable payouts that ease the stress of budgeting in your later years. They’re not just about locking money away—they’re about crafting a flexible plan that blends security with growth.

Feeling overwhelmed? Start small: learn how annuities work and how they fit your unique needs. It’s easier than you think, and the peace of mind? Totally worth it.

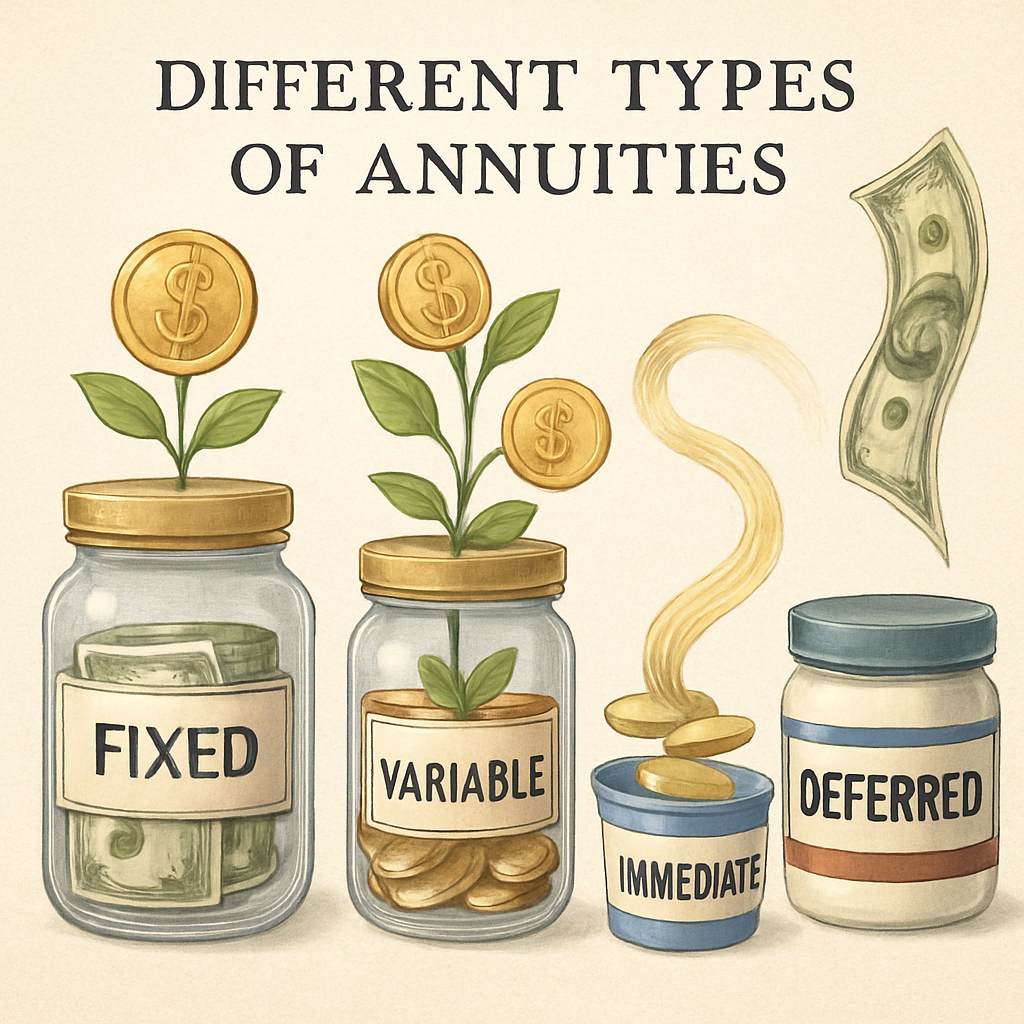

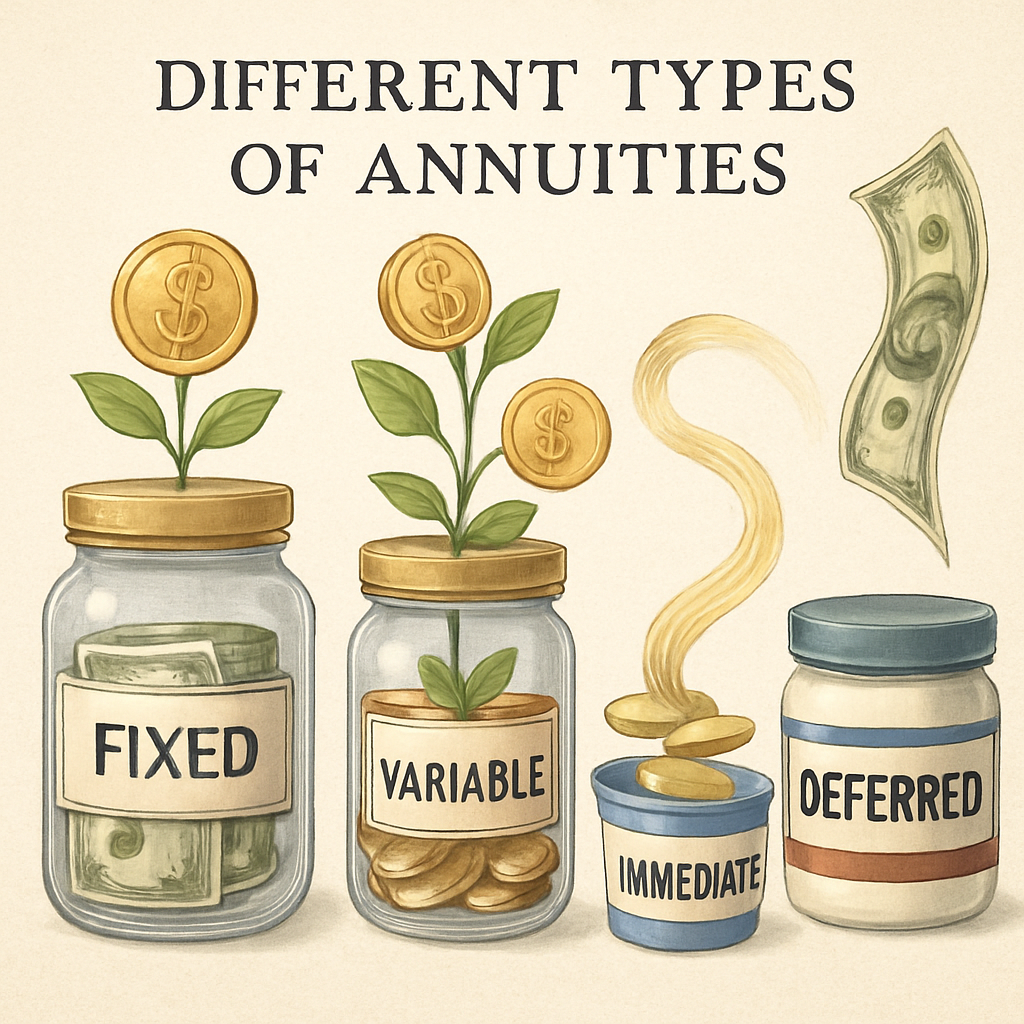

Step 1: Understand the Different Types of Annuities for Retirement Income

Okay, so you’re starting to explore retirement income strategies with annuities, and that feels a bit like stepping into a vast forest, doesn’t it? All these terms—fixed, variable, immediate, deferred—it can get confusing fast. But here’s the thing: getting a handle on the types of annuities is really your first step to building a rock-solid retirement plan.

Imagine annuities as different kinds of financial containers. Some are like sturdy jars that keep your money safe and give you a steady drip of income. Others are like adventure-packed tubs that can grow with the market but come with ups and downs. Your choice depends a lot on what feels right for your comfort level and goals.

Immediate vs. Deferred Annuities: When the Payments Start Matters

Let’s start with timing, because it’s a biggie. An immediate annuity kicks in right away. You give the insurer a lump sum, and boom—they start sending you income usually within a year. It’s great if you’re at or near retirement and want that predictable paycheck to begin.

On the flip side, there’s the deferred annuity. Think of this one like a savings pot that grows over time. You can put money in gradually or as a lump sum, then let it build up — tax-deferred, by the way — until you’re ready to start taking payments down the line. It’s perfect if you’re still working or want to prepare ahead without touching the money just yet.

Fixed Annuities: Stability and Peace of Mind

Maybe you don’t want your investment rollercoastering up and down with the stock market. In that case, a fixed annuity might feel like a warm, cozy blanket. It guarantees a fixed interest rate for a certain period or even the entire contract. That means your income is predictable and steady, which is a huge comfort when you’re trying to budget monthly expenses in retirement.

But fair warning: inflation can be the sneaky enemy here. While your fixed annuity payments won’t drop, they might not keep pace with rising living costs over the years. So, it’s good for peace of mind but maybe not ideal if you want your income to grow along with the economy.

Variable Annuities: Growth Potential (With Some Ups and Downs)

Now, if you’re a bit more adventurous and want to aim for higher income potential, a variable annuity lets you invest in different subaccounts, like mutual funds. Your payments can go up or down depending on how those investments perform.

Yep, there’s risk here—you could lose money if the market dips. But the flip side is you might ride the market’s growth to a bigger nest egg. Variable annuities often come with extra bells and whistles like lifetime withdrawal guarantees and death benefits for your loved ones, which can add a nice layer of security despite the market risk.

Fixed-Indexed Annuities: The Best of Both Worlds?

Ever heard of fixed-indexed annuities? These are kind of a hybrid. They credit interest based on a market index’s performance—say, the S&P 500—but with a cap on gains and, importantly, they protect you if the market tanks.

This means you get growth potential paired with a safety net. It’s like having your cake and eating it, too—but remember, they may limit how big your slice can get.

So, what’s the takeaway here?

You really want to start by thinking about what matters most to you: Is it guaranteed income that never wavers? Or are you comfortable with some risk in exchange for a chance at more growth? Do you want income now, or are you more about building your pot quietly until later?

Understanding these annuity types lays the groundwork for a retirement income strategy that works for your unique life—because no two retirements look the same.

And if you feel stuck here, you’re not alone. Talking with a financial expert who can help make sense of your options is totally worth it. You can dive deeper into the nuts and bolts of annuities through resources like these, or get into the pros and cons of fixed versus variable annuities right here.

Remember, retirement income strategies with annuities aren’t one-size-fits-all. Getting curious about the different types is step one toward building a plan that fits you perfectly.

Ready to take the next step? Grab a notebook, jot down what you think feels right, and consider scheduling a chat with someone who can help tailor these options to your life.

Step 2: Evaluate Your Retirement Income Needs and Risk Tolerance

Alright, let’s get real for a minute. Figuring out how much income you’ll need during retirement isn’t just about numbers—it’s about your lifestyle, your peace of mind, and yes, your comfort with a little risk.

Have you ever caught yourself wondering, “Will my savings really cover the fun trips, the bills, or even that unexpected car repair?” It’s a common worry, and honestly, it makes sense to break this down before you’re knee-deep in retirement.

How Much Income Will You Actually Need?

Here’s the thing: many people assume they’ll need 100% of their current income to get by in retirement. But studies suggest otherwise. A good rule of thumb starts at about 75% of your pre-retirement income to support your lifestyle once you’re retired. Why less? Because some costs—like commuting or saving for retirement—quietly disappear.

Want a clearer picture? Let’s say you’re bringing in $100,000 a year now. You might aim for around $75,000 annually during retirement to keep things comfy. But wait—don’t take this as gospel. How much you spend can shift, depending on your health, location, and that spontaneous hobby you take up.

To drill down more, think about the income you’ll receive beyond what you’ve packed away—like Social Security. For instance, if Social Security covers $39,000 of that yearly need, you’ll want your savings and annuities to provide the rest. If you’re comfortable withdrawing about 4% a year from your investments, that helps you calculate the pile you need to have saved up.

These numbers aren’t just pulled from thin air. They’re informed by analysis from financial experts like the folks at T. Rowe Price on retirement income, who break down income replacement rates in simple, relatable terms.

Understanding Your Comfort with Risk

Now, let’s talk about risk tolerance—the big question: how much financial risk are you comfortable with? It’s an honest question but trickier than it sounds.

You might think risk tolerance changes a ton as you near retirement, but research shows it’s surprisingly stable for most people. According to insights from Morningstar’s research on risk tolerance, about 90% of people’s risk preferences don’t shift drastically over time. So, a tool measuring your risk now generally sticks around even once you’re withdrawing your savings.

But here’s the catch: just because your risk tolerance score is steady doesn’t mean your investments shouldn’t evolve. As you get closer to—or enter—retirement, matching your portfolio to what feels right for you is crucial.

Are you okay with steady, predictable income that annuities can bring? Or do you want to keep some growth potential with investments that carry a bit more risk? Maybe a mix suits you best.

This is why evaluating both your income needs and your comfort with risk goes hand in hand when shaping retirement income strategies with annuities. It’s like picking the right pair of shoes—you want something practical but also comfortable enough to wear all day.

Here’s What You Can Do Now

Grab your last tax return or pay stub and jot down your annual income. Cut that by 25%—does the resulting number feel doable to live on?

Then, list any guaranteed income sources like Social Security or pensions. What’s left is what your savings and annuities need to cover.

Next, honestly assess how you feel about risk. Picture your money like a garden: some plants need nurturing and patience, while others require a steady hand and protection from storms. Which sounds more like your style?

And hey, if this feels overwhelming, you’re not alone. Consulting with a financial advisor, especially one who understands annuities and retirement planning, can really help paint a clearer picture that fits your unique situation.

Planning for retirement income isn’t a one-and-done task. It’s a process of checking in, adjusting, and making sure your plan grows as you do—both in goals and comfort zone.

Step 3: Incorporate Indexed Universal Life Insurance (IUL) as a Complementary Strategy

Okay, so you’ve gotten a handle on your income needs and your comfort with risk when thinking about annuities. But what if you want a bit more flexibility tucked into your retirement income plan? That’s where Indexed Universal Life Insurance, or IUL, can step in as a smart complement—not just a sideshow.

Think about retirement income strategies with annuities like your sturdy foundation. IUL is like the adjustable lamp on your desk: it brightens the space in a way that fits your mood and needs. It’s permanent life insurance, sure, but it also offers a cash value component that can grow based on a stock market index, like the S&P 500, without the direct risks of the market itself.

Here’s what that means for you: part of your premium pays for the death benefit, offering security for your family. The rest goes into a cash value account that’s tied to an index’s performance. But you’re not actually investing in the stock market, so there’s a floor—meaning you won’t lose money if the market dips. At the same time, your cash value has the chance to climb when the market does well, although gains are typically capped so you won’t get the full upswing.

Sounds like a neat balance, right? It’s kind of like having your cake and eating it too, with a little insurance frosting on top.

But before you jump in, ask yourself: Do you want a bit of growth potential mixed with some protection? Are you comfortable managing a policy with moving parts, like caps on growth and fees that come along with IUL? These policies can be a bit pricier than basic whole or term life insurance, thanks to their complexity.

One practical tip: IUL can serve as a tax-advantaged way to build cash value over time, which you might be able to tap into during retirement for supplemental income. Unlike annuities where earnings are taxed as ordinary income upon withdrawal, IUL loans and withdrawals—if done carefully—can be tax-free. But, and it’s a big but, there are details you need to watch closely, such as avoiding a policy becoming a Modified Endowment Contract (MEC), which could trigger taxes and penalties.

How does this complement annuities? Annuities shine at guaranteeing income streams you won’t outlive, which is a huge comfort as you age. IUL adds a layer of flexibility and potential growth, helping to round out your retirement income landscape with some growth and legacy planning benefits.

Still wondering whether adding an IUL policy is worth the extra complexity? It’s often worth a conversation with a trusted advisor who can model your financial timeline, risk tolerance, and income needs. That way, you get a plan tailored to you, not just the shiny features.

To dive deeper and make sure you’re getting all the facts, check out this detailed explanation of indexed universal life insurance from Aflac and a helpful side-by-side comparison between IUL and annuities from SmartAsset. Both will help you get a clearer picture of how these pieces can fit into your plan.

So, what’s the next step? Make a list of your retirement goals. Do you want guaranteed income, potential growth, legacy building, or some combo of all three? Then reach out for a personalized consultation. Life Care Benefit Services partners with multiple carriers to find the best fit for your unique situation—because there’s no one-size-fits-all retirement plan.

Remember, retirement income strategies with annuities don’t have to be a solo journey. They work best when they’re part of a thoughtful, flexible plan—and IUL might be just the complementary piece you need.

Step 4: Compare Annuity Options to Choose the Best Fit for Your Retirement Goals

Picking the right annuity isn’t just about numbers—it’s about how those numbers match your life. You might want steady income, growth potential, or something in between. Or maybe you worry about leaving money behind for someone you love. So, how do you find the annuity that actually fits what you want?

Let’s break it down together. When we talk about annuities, three main types usually come up: fixed, fixed-indexed, and variable annuities. Each has its own flavor—some safer, some with more upside risk, and some promising guaranteed income.

Fixed Annuities: The Safety Net

If you’re the type who wants peace of mind above all else, fixed annuities might catch your eye. They promise a guaranteed interest rate over a set period, usually between 2 to 10 years. Think of it like locking your money in a safe room where the doors are closed against surprises.

One reason people love this option: you won’t see your principal drop. Your money grows steadily, tax-deferred, and you can usually choose a payout that lasts a lifetime if you want. But be aware, if interest rates rise after you lock in, you’re stuck with your original rate until the term ends.

Sound simple? Well, it mostly is. But compare rates and terms carefully, because they vary a lot between companies—and they impact both how much you earn and for how long. Want to see how today’s fixed annuity rates stack up?

Fixed-Indexed Annuities: A Little More Room to Grow

Now, if fixed annuities are the safe room, fixed-indexed annuities are like that safe room with a window to the stock market—but no risk of falling out. Your earnings are linked to a market index like the S&P 500, but here’s the catch: your principal is protected against downturns. So, if the market tanks, your money stays safe. If the market soars, you earn some upside—but usually capped at a certain rate.

This mix makes them popular for people wanting some growth without the full gamble. But keep an eye on the caps, participation rates, and fees. These details can sneak up on you, affecting what actually ends up in your pocket.

If you want a deeper dive, check out this comparison of fixed, fixed-index, and variable annuities. It’s a solid resource to see how these work in different market conditions.

Variable Annuities: Growth Potential with Risk

Alright, variable annuities. You know those can feel like walking a tightrope. They let you invest in subaccounts—kind of like mutual funds within your annuity—offering the chance for higher returns, but your balance can go up and down with the market.

So, while you’re chasing growth, you also face the risk of losing money. And that’s not everyone’s cup of tea. Fees can be higher here, and surrender charges might apply if you tap out too soon.

But the flexibility is a big draw. You can tailor your investments depending on your risk tolerance—something fixed products don’t offer. If you’re curious about whether this fits your style, there are detailed guides to variable annuities’ risks and benefits that can shed some light.

How to Decide: What Really Matters to You?

This is the million-dollar question. Do you want guarantees that prevent you from touching any principal? Or are you willing to take some calculated risk for better growth? Maybe lifetime income that can’t be outlived? Or flexibility to adjust your investments?

Try listing your goals: income stability, growth, legacy planning, or tax advantages. Then, check how each annuity aligns. Don’t rush—it’s smart money.

And remember, your annuity’s strength also depends on the insurance company backing it. Look for providers with strong ratings to feel confident your money’s in safe hands.

Making head or tail of this isn’t a solo gig. So if you want to feel truly confident about your choice, reach out for expert advice. Life Care Benefit Services can connect you with licensed professionals who’ll help you compare options based on your unique retirement goals.

Ready to see some of the choices laid out side-by-side? Here’s a quick comparison table to help you visualize the key differences.

| Feature | Fixed Annuity | Fixed-Indexed Annuity | Variable Annuity |

|---|---|---|---|

| Principal Protection | Guaranteed | Guaranteed (no loss in value) | No (market risk applies) |

| Growth Potential | Fixed interest rate | Linked to market index with caps | Market-based, potentially higher returns |

| Income Options | Guaranteed income payment available | Income options with growth potential | Flexible, includes lifetime income riders |

| Risk Level | Low | Moderate | High |

| Fees & Charges | Low to moderate | Moderate | Higher (management, mortality, surrender) |

So, what should you do next? Start with your priorities. Then, ask for personalized quotes and read the fine print. Don’t overlook how fees, surrender periods, and payout options can impact your retirement comfort.

Want a friendly conversation to make sense of all this? Life Care Benefit Services offers no-pressure consultations to help you find the best retirement income strategies with annuities tailored just for you. Why wait?

Step 5: Plan for Taxes, Fees, and Payout Timing to Maximize Your Income

Alright, let’s talk about something that often flies under the radar but can make or break your retirement income: taxes, fees, and when you actually get your payouts. You might think, “Ugh, taxes and fees? That sounds complicated and boring.” But stick with me—getting this part right can seriously boost how much money stays in your pocket each month.

Why Taxes on Annuities Matter More Than You Think

Here’s the deal: annuities grow your money tax-deferred, which is a huge plus because you don’t pay taxes on the gains until you withdraw. But, when that payout starts, taxes come knocking.

Whether your annuity was funded with pre-tax money (like from a 401(k) or IRA) or after-tax money makes a big difference. Qualified annuities, meaning those funded with pre-tax dollars, get taxed fully as ordinary income when you receive payments. With non-qualified annuities, you only pay taxes on the earnings, not the original amount you invested. See the nuance there? It’s a difference that can save you thousands over time.

And oh—don’t forget about early withdrawal penalties if you dip into your annuity before 59½. That extra 10% tax can hit hard, so planning your payouts around this age is key to avoid sneaky surprises.

Fees: The Quiet Eaters of Your Gains

Next up, fees. They don’t shout for attention but quietly chip away at your income over the years. Common ones include management fees, mortality and expense charges, and surrender fees if you withdraw early.

Look closely at your annuity contract’s fee schedule. Some fees might be low and reasonable; others can be surprisingly steep. If you’re uncertain, ask a pro to break down what fees actually mean for your bottom line—because even a 1% fee difference can mean thousands lost in retirement.

Timing Your Payouts: It’s More Than Just Waiting

Here’s where things get interesting. When and how you start taking payments affects your cash flow and tax bill. For example, annuitizing your contract turns your lump sum into a steady, often guaranteed income stream. Those payments can include a mix of tax-free principal return and taxable earnings, potentially lowering your tax liability each year. But after a certain age—often tied to your life expectancy—all payouts become fully taxable.

On the other hand, if you take withdrawals at your own pace, taxes hit differently—usually first on earnings (thanks to the IRS’s Last In, First Out rule). This means you could face a bigger tax bill upfront if you’re not careful.

So, what should you do next?

- First, gather all your annuity paperwork and find out whether your funds are qualified or non-qualified.

- Talk to a licensed tax advisor or annuity expert who can help you run the numbers on taxes and fees specific to your annuity products.

- Think through your income needs and how payout timing might impact your tax brackets each year.

Planning this thoughtfully can mean the difference between just getting by in retirement and truly enjoying it. Life Care Benefit Services can connect you with licensed professionals who’ll help you understand these nuances. Why not schedule a free consultation to clear up the confusion and chart your best path?

For a deeper dive into how annuities are taxed and what withdrawal rules mean for your income, check out the expert breakdown on annuity taxation. And for official guidance straight from the source, the IRS’s detailed overview of pension and annuity taxes is incredibly helpful.

Remember, the goal here isn’t to dodge taxes entirely (that’s impossible) but to maximize what you get to keep. It’s like turning your annuity into a well-oiled machine that feeds your retirement dreams instead of draining them.

Step 6: Integrate Group Health Insurance and Mortgage Protection to Secure Retirement

Planning your retirement income strategies with annuities is one thing—but making sure your health and home are protected as you transition into this new chapter? That’s a whole other ballgame. You’ve probably thought about annuities for steady income, but have you paused to consider how group health insurance and mortgage protection fit into the bigger picture?

Let me ask you something: ever caught yourself worrying about unexpected medical bills popping up in retirement? Or what happens to your home payments if something goes sideways? It’s not the fun stuff, but it’s exactly what can derail even the best-laid retirement plans.

Why Group Health Insurance Still Matters After You Retire

Here’s the thing—just because you retire doesn’t mean health expenses go away. In fact, healthcare costs can sneak up on you, especially if you’re not fully covered. Many retirees rely on group health insurance through their former employer or spouses’ plans to bridge gaps Medicare doesn’t cover.

But it’s tricky. You need to understand how retiree health coverage works alongside Medicare Parts A and B. Missing deadlines for Medicare enrollment can lead to penalties, and some retiree plans only kick in after Medicare pays its share. Knowing these rules means fewer surprises and more stability.

If you’re running a small business or part of one, you could explore group health insurance options tailored to retirees or early retirees. These plans often provide more affordable rates and can cover services Medicare doesn’t. Curious how to find the right group health plan without it feeling like a maze? We’ve got detailed guidance on navigating group health insurance for small business owners that can point you in the right direction.

Mortgage Protection: Don’t Let Your Home Become a Retirement Stress Point

Now, about your mortgage—yeah, it’s still a thing. Even if retirement sounds like a break from bills, mortgage payments can keep you chained if you don’t plan ahead. Mortgage protection insurance gives you a safety net. Imagine losing your income temporarily or permanently; this coverage can step in to make those house payments, so you’re not risking your biggest asset.

Think about it this way: securing your mortgage protection means you’re less likely to have sleepless nights worrying if the house stays yours. And that peace of mind? Priceless.

If you want a simple route to get started, check out our straightforward guide on how to secure a mortgage protection life insurance quote online. It breaks the process into easy steps—no intimidating jargon, just clear info.

Putting It All Together

Integrating group health insurance and mortgage protection with your retirement income strategies with annuities isn’t just smart—it’s essential. You want your retirement years to be about enjoying life, not juggling unexpected expenses or stressing over bills.

So, what should you do next? First, review your current health coverage carefully to see how it meshes with Medicare and your retirement timeline. Then, assess your mortgage situation and consider if protection insurance fits your goals. Don’t forget to touch base with an expert who can tailor these protections to your unique situation.

Curious to explore these options in more detail? Learn more about navigating group health insurance or get a mortgage protection quote to start securing your retirement now.

Remember, it’s not just about setting up income streams with annuities—it’s about wrapping your whole life in protections that let you breathe easier every day.

And if you still feel a bit overwhelmed, reaching out for a tailored consultation can make all the difference. Trust me, having someone who knows the ropes beside you? That’s how you turn good plans into great outcomes.

Need help tailoring your retirement and insurance plans? Life Care Benefit Services is here to help you combine these crucial elements seamlessly—so you can focus on what really matters.

Conclusion

Wrapping your head around retirement income strategies with annuities can feel like piecing together a puzzle in the dark, right? But here’s the thing—it’s worth the effort. This isn’t just about numbers on a page or ticking boxes. It’s about you, your peace of mind, and the confidence to live your retirement years on your own terms.

Think about that moment when a surprise car repair or a medical bill throws everything off balance. Annuities, paired with smart protections, can soften those blows. They’re not some magic fix, but a steadying hand you’ll be thankful for when life throws curveballs.

So, what really matters? Start simple. Review where you stand now—your health coverage, your mortgage, your savings. Then, reach out for the tailored advice that cuts through the confusion. You don’t have to navigate this alone. Life Care Benefit Services specializes in crafting these plans with people just like you in mind—real folks juggling life’s unpredictability.

Ready to take that next step? Scheduling a consultation could be the move that turns your “what-ifs” into “I’ve got this.” Because at the end of the day, retirement income strategies with annuities aren’t just about protecting dollars—they’re about protecting the life you’ve worked so hard to build.

Frequently Asked Questions About Retirement Income Strategies with Annuities

So, you’ve been hearing a lot about annuities as a part of retirement income strategies, but it still feels a bit fuzzy? You’re definitely not alone. Let’s break down some of the questions that pop up the most. It’ll help clear the fog and make those “what-ifs” feel a little less intimidating.

What exactly are annuities, and why are they considered for retirement income?

Think of an annuity as a contract with an insurance company that turns a lump sum or series of payments into a steady stream of income. The big appeal? Predictability. You get a reliable paycheck during retirement, which can help cover essentials without sweating every market dip.

Are there different types of annuities I should know about?

Yes, and this often trips people up. The basic types are fixed, variable, and indexed annuities. Fixed offers stable, guaranteed returns—think of it as the solid, no-surprises choice. Variable lets you invest in markets with potential for growth but comes with more risk. Indexed ties your returns to a market index, aiming for a middle ground with some growth potential and downside protection.

How do fees work with annuities? Are they expensive?

Good question. Fees can vary widely and are often the sneaky part. Some annuities have surrender charges if you pull out early or administrative fees that chip away at your returns. It’s crucial to ask about all these before signing up. The right annuity for you balances cost with benefits, so don’t just go for the cheapest or flashiest option.

Will annuities affect my taxes?

Generally, the money you put into an annuity grows tax-deferred, which means you won’t pay taxes on earnings until you withdraw. When you start receiving payments, that income is usually taxed as ordinary income. This might seem like a bummer, but it can actually work in your favor by helping you manage taxable income year to year.

What if I need access to my money before retirement?

This can be a dealbreaker for some. Many annuities have penalties on early withdrawals—sometimes for years. That’s why it’s wise to keep a separate emergency fund. You want your annuity working for you, not locking your cash away when life’s unpredictability hits.

Are annuities safe, especially with insurance companies?

They’re generally considered safe, but like any financial product, it depends on the provider’s strength. Insurance companies offering annuities are regulated and must meet solvency standards. Still, it’s smart to pick companies with strong ratings. Life Care Benefit Services can help you navigate those choices carefully.

How do I decide if an annuity fits into my retirement income strategies?

Start by looking at your whole financial picture: other income sources, your health, and lifestyle goals. Annuities can offer peace of mind and steady income, but they’re not one-size-fits-all. Chatting with a financial advisor or trusted insurance agent is really the best move here.

So, feeling a bit more confident now? Scheduling a consultation with Life Care Benefit Services could be just the step you need. We’ll sit down, unpack all this, and tailor a plan that fits your unique story—no pressure, just clarity.