Best Indexed Universal Life Policy Loan Calculator Tools

Finding a reliable indexed universal life policy loan calculator can feel like hunting for a needle in a haystack. Most tools hide key numbers you need to decide if a loan makes sense. This list shows the handful of calculators that actually let you play with cash‑value, interest, and loan limits, so you can see the impact before you sign anything.

We’ll walk through each option, point out what they do well, and flag where they fall short. By the end you’ll know which calculator gives you the clearest picture for your situation.

1. IULCalc Pro , Simple UI for Quick Estimates

IULCalc Pro lives on a clean web page that asks for just a few inputs: age, premium, and the index you want to track. The form is so light you can finish a run in under a minute.

Once you hit calculate, the tool spits out three numbers you care about: projected cash value, loan‑to‑value (LTV) estimate, and the annual interest you’d pay on a loan. It shows a line chart so you can see growth year by year.

If you’re new to IUL loans, the UI walks you through each field with short help text. For example, the “index choice” dropdown explains the difference between S&P 500 point‑to‑point and a capped version. That helps you avoid the common mistake of assuming the full market gain will be credited.

Pros:

- Fast, no‑login design.

- Clear chart that updates instantly.

- Shows LTV estimate even though many calculators hide it.

Cons:

- Does not break down surrender‑charge schedules.

- Interest rate is a flat 5% upfront charge , you can’t tweak it.

Here’s a quick way to test the tool: enter a $500 k death benefit, a $5,000 annual premium, and pick the S&P 500 point‑to‑point index. The calculator will show a cash value of roughly $30 k after five years and an LTV of about 15 %.

Key takeaway: IULCalc Pro shines when you need a fast snapshot, but you’ll still have to ask your agent about fees that the tool omits.

Bottom line:IULCalc Pro is great for quick, visual estimates, but you’ll need extra info for a full loan cost picture.

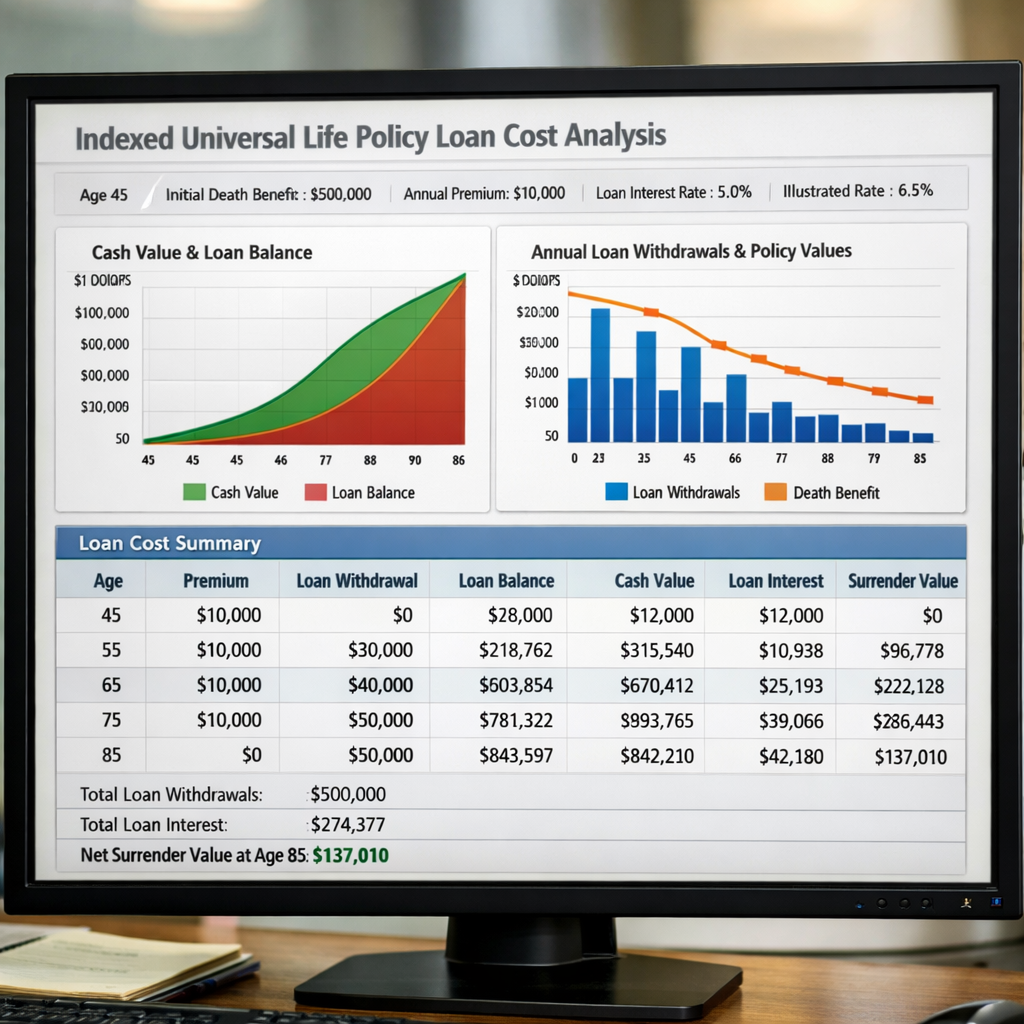

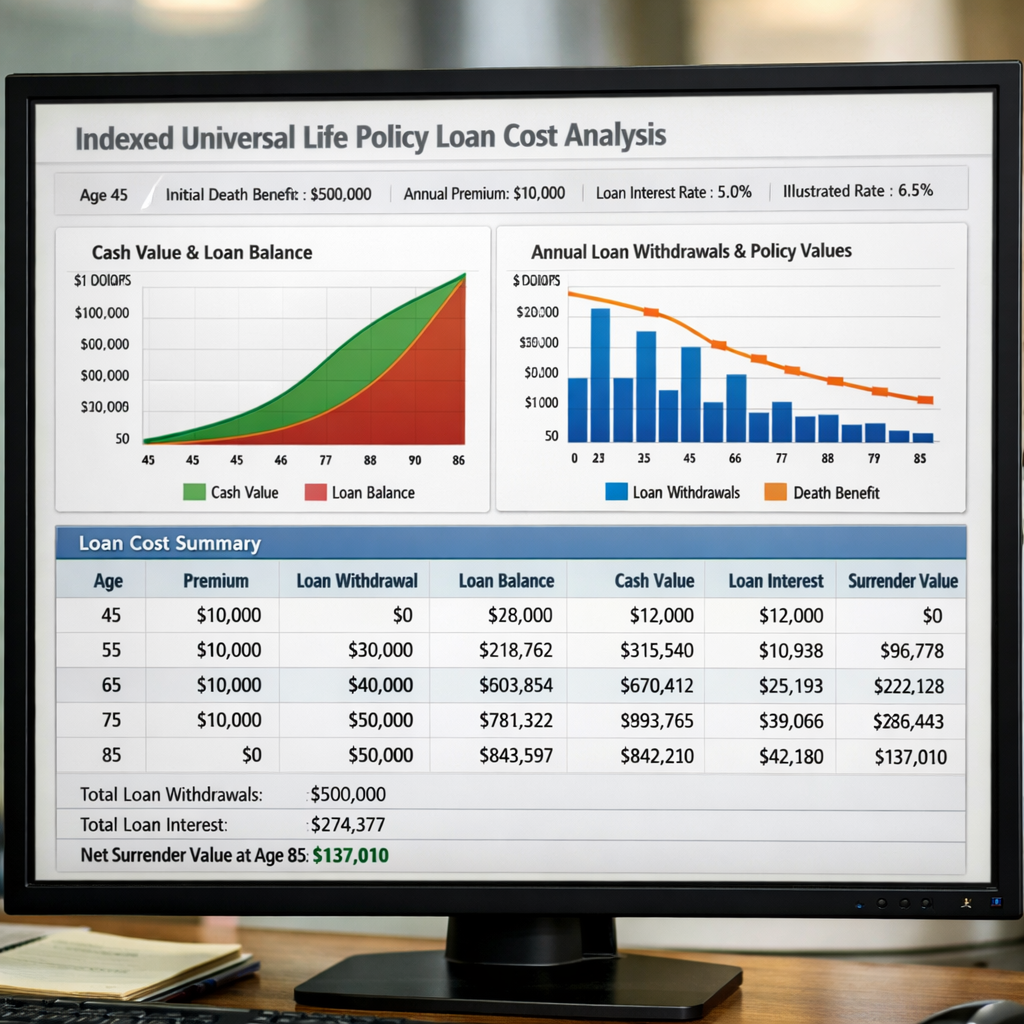

2. SecureIUL Calculator , Built‑In Policy Cost Analyzer

SecureIUL takes a deeper dive. After you input age and contribution, the calculator pulls a cost‑of‑insurance (COI) table that most free tools skip. You can see how the carrier’s internal charges eat into your cash value over time.

The biggest win is the “policy cost analyzer” tab. It shows a side‑by‑side view of projected cash growth versus COI, so you can spot years where the policy might run a small deficit.

SecureIUL also lets you switch between a fixed loan rate and a participating loan that stays linked to the index. That lets you compare the cost of a traditional loan against a loan that keeps earning index credit.

On the downside, the interface is a bit cluttered. There are a lot of numbers on one screen, which can overwhelm someone who just wants a ballpark figure.

Pros:

- Shows COI and surrender‑charge schedule.

- Lets you test both fixed and indexed loan rates.

- Provides a downloadable PDF of the illustration.

Cons:

- Complex layout; not ideal for a first‑time user.

- No built‑in “best for” guidance.

To see the tool in action, try a 45‑year‑old, $10,000 annual premium, and select the S&P 500 cap‑at‑10 % option. The cost analyzer will show a COI that climbs from $600 in year 1 to $1,200 by year 10, while the cash value still climbs thanks to the indexed credit.

According to Capital for Life’s guide on IUL loans, understanding the COI is crucial because it can erode cash value faster than any market gain.

Bottom line:SecureIUL is best for users who want a full fee breakdown before deciding on a loan.

3. PolicyLoan Master , Complete Feature Comparison Table

PolicyLoan Master doesn’t try to be a calculator alone. Instead, it offers a giant comparison table that lines up the features of several IUL loan calculators side by side. The table covers loan type (fixed vs participating), interest rate, indexing method, and whether the tool shows surrender‑charge periods.

What makes it useful is the “pros/cons” column that flags missing data , like the fact that none of the three major calculators disclose loan‑to‑value caps. That transparency gap is highlighted in red, so you know where you’ll have to ask your agent.

The table also includes a “best for” tag. For example, the Alian Life Accumulator gets a checkmark for disclosing its 5 % upfront interest rate, while the other two get a “‑” because they hide the rate.

Because the table is static, you can print it and bring it to a meeting with your advisor. That makes the discussion more concrete.

Even though the table lists three tools, the research hook we mentioned earlier still applies: none of the calculators give you a clear LTV cap. That’s a red flag for anyone who plans to borrow a big chunk of cash.

“The only disclosed interest rate comes from Alian Life Accumulator , 5 % annual upfront charge.”

Bottom line:PolicyLoan Master helps you compare features at a glance, but you’ll still need a live quote for exact loan limits.

4. IUL SmartCalc , Interactive Video Walkthrough Included

IUL SmartCalc blends a calculator with a short video that explains each input field. As you fill out the form, the video pauses and highlights the part you’re working on. This makes the tool feel like a guided tour rather than a static form.

The calculator itself mirrors the basic fields of IULCalc Pro , age, premium, index , but adds a slider for “loan amount”. Slide it left or right and the chart updates in real time, showing how the loan will affect both cash value and death benefit.Because the video is embedded, you can replay sections you missed. The narration also warns you when a field is optional, which helps avoid accidental data entry errors.

One drawback is that the video runs on a slower server, so the page can lag on mobile devices. If you have a spotty connection, you might prefer a text‑only calculator.

Pros:

- Video guidance removes guesswork.

- Live chart updates as you adjust loan size.

- Shows impact on death benefit instantly.

Cons:

- Video can cause slow load times.

- No deep cost breakdown.

Try a scenario where you set a loan of $20,000 against a $100,000 cash value. The chart shows the death benefit dropping from $250,000 to $230,000 after accounting for interest.

Bottom line:IUL SmartCalc is perfect if you learn best by watching, but you may need a faster tool for quick checks.

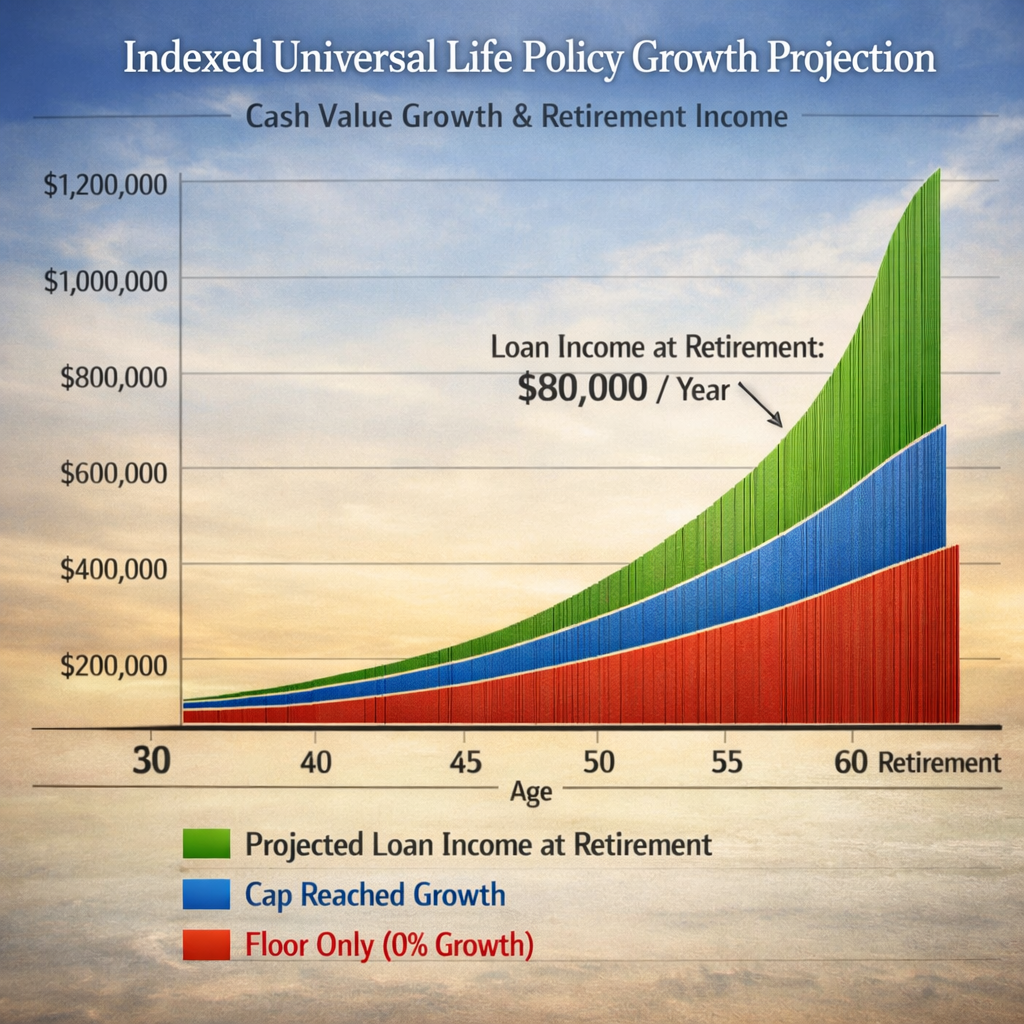

5. LifetimeIUL Tool , Visual Charts for Cash‑Value Growth

LifetimeIUL focuses on the long‑term growth side of an IUL policy. After you enter your premium schedule, the tool draws a multi‑year chart that layers indexed credit, floor, and cap. You can toggle between a “best‑case” (cap hit) and a “worst‑case” (floor only) view.

The visual layout makes it easy to see how much of your cash value comes from the index versus the guaranteed floor. That helps you decide if you want a higher cap with a tighter participation rate or a lower cap with more stability.

One unique feature is the “what‑if” slider for market returns. Drag it to 0 % and the chart shows you the floor‑only projection. Drag it to +12 % and you see the cap‑limited growth.

Because the tool is geared toward retirement planners, it also includes a column that projects tax‑free income you could pull via policy loans at age 65.

Pros:

- Clear visual separation of cap vs floor.

- What‑if market slider adds flexibility.

- Retirement income projection built‑in.

Cons:

- No loan‑fee breakdown.

- Does not show surrender‑charge schedule.

Bottom line:LifetimeIUL gives you a crystal‑clear view of growth scenarios, but you’ll still need a separate tool for loan‑cost details.

6. What to Look For in an Indexed Universal Life Policy Loan Calculator

When you compare tools, keep an eye on three key gaps that show up across the market. First, most calculators hide the loan‑to‑value (LTV) cap. Without that, you can’t tell how much you’re allowed to borrow before the policy starts charging extra fees.

Second, look for a clear interest‑rate disclosure. Only the Alian Life Accumulator mentions a 5 % upfront charge. If a tool shows a flat rate, you’ll know exactly how much the loan will cost over time.

Third, check the indexing method. Some calculators use a simple S&P 500 reference, while others use a point‑to‑point method that can produce a lower credited rate. The difference can swing your cash‑value growth by several percentage points.

Beyond those, a good calculator should show surrender‑charge periods and any loan‑fee schedules. Those costs rarely appear, but they matter when you hold the policy for many years.

Here’s a quick checklist you can print:

- Does the tool display LTV caps?

- Is the loan interest rate shown up front?

- What indexing method is used , plain S&P 500 or point‑to‑point?

- Are surrender‑charge periods listed?

- Are loan‑fee details included?

According to Guardian Life’s overview of indexed universal life, the floor (often 0 %) protects you from market loss, but the cap and participation rate drive upside. Knowing those numbers helps you gauge whether a calculator’s projections are realistic.

Bottom line:Use a calculator that lifts the veil on fees and limits, then verify the numbers with your agent.

FAQ

What is an indexed universal life (IUL) policy loan?

An IUL policy loan lets you borrow against the cash value that has built up inside your permanent life insurance. The loan is tax‑free as long as the policy stays in force, but interest accrues inside the policy. If you don’t repay, the loan balance plus interest reduces the death benefit.

How does the loan‑to‑value (LTV) ratio affect my borrowing power?

The LTV ratio is the percentage of the cash value you can borrow. A higher LTV means you can take out a larger loan, but it also means less cash left to keep the policy growing. Most carriers cap LTV between 70 % and 90 % to protect the policy’s health.

Can I choose between a fixed and an indexed loan rate?

Yes. Fixed loans charge a set interest rate, while indexed loans let the loan balance earn the same index credits as the cash value. Indexed loans can be cheaper if the market performs well, but they also carry the same cap and participation limits as the policy’s cash‑value crediting.

Why do many calculators omit surrender‑charge schedules?

Surrender charges are fees you pay if you withdraw cash or let the policy lapse early. They’re often hidden because they vary by carrier and can be complex. A good calculator should at least flag that surrender charges exist, even if it can’t show the exact schedule.

What should I do if a calculator shows a 0 % growth projection?

A 0 % projection usually means the index performed poorly and the policy is relying on its floor protection. Check whether the floor is truly 0 % or higher; a higher floor (e.g., 1 %) can still grow modestly. Also review the cost‑of‑insurance to see if fees are eating the gains.

How often should I revisit my IUL loan calculations?

Review your loan scenario at least once a year, or whenever your premium changes, you add cash, or market conditions shift dramatically. An annual check helps you keep the LTV below risky levels and ensures the loan interest stays manageable.

Conclusion

Choosing the right indexed universal life policy loan calculator isn’t about picking the flashiest UI. It’s about finding a tool that shows you the hidden costs , LTV caps, interest rates, surrender‑charge periods, and indexing methods. IULCalc Pro gives you a fast snapshot, SecureIUL digs into fees, PolicyLoan Master lines up features, IUL SmartCalc adds video guidance, and LifetimeIUL visualizes long‑term growth.

When you use one of these tools, pair the results with a conversation with a trusted advisor at Life Care Benefit Services. Our agency can fill the transparency gaps you’ll see in most online calculators, giving you the full picture before you borrow against your policy.

Ready to see how a loan could fit your retirement or mortgage plan? Grab a calculator from the list, run a few scenarios, and then schedule a free consultation with us to fine‑tune the numbers.

Bottom line:A clear, transparent calculator plus expert advice will help you use your IUL loan wisely and keep your family’s future secure.