Best IUL vs Whole Life Retirement Comparison: Top 5 Picks

Retirement can feel like a maze of numbers, taxes, and insurance jargon. Most people wonder which life‑insurance tool will actually grow their cash while protecting their loved ones. In this piece you’ll see a short list of five real options, how each works for retirement, and what to check before you sign.

We’ll walk through each pick, add practical tips, and finish with a quick checklist so you can match a plan to your goals.

1. SecureFuture IUL (Our Pick) , Flexible Growth for Retirement

SecureFuture’s indexed universal life (IUL) policy blends permanent coverage with a cash‑value bucket that follows a stock‑market index. The policy credits interest based on the S&P 500, but you never own the stocks directly. That means you capture upside when markets rise, yet a floor of 0 % stops any loss when markets fall.

What makes it stand out for retirees is the flexibility. You can raise premium payments when you have extra cash, or let the cash value cover the cost of insurance if a month gets tight. The policy also lets you take tax‑free loans against the cash value, which can serve as supplemental retirement income.

Because the cap on credited interest is usually set around 9‑12 %, the growth potential is higher than a traditional whole‑life policy’s guaranteed rate, while still offering downside protection.

SecureFuture also bundles living‑benefit riders that let you tap the death benefit early for chronic illness or long‑term care, adding another layer of retirement security.

When you compare quotes, look for a participation rate close to 100 % and a cap that matches your growth expectations. The higher the participation, the more of the index gain you keep.

Bottom line:If you want upside potential with a floor that protects your cash value, SecureFuture’s IUL is a strong contender.

2. Traditional Whole Life Insurance , Guaranteed Cash Value

Whole life insurance provides a fixed premium and a cash‑value account that grows at a guaranteed rate set by the insurer. The growth is modest, often 2‑3 % plus any dividends the company declares, but you know exactly what you’ll have at any point in time.

Because the cash value is guaranteed, whole life can serve as a reliable “emergency bucket” that you can borrow against without tax consequences, as long as the policy stays in force.

Many mutual insurers also pay annual dividends to policyholders. Those dividends can be used to buy paid‑up additions, which boost both cash value and death benefit. Over decades, the compounding effect of dividends can make the cash value grow faster than the base guarantee alone.

Whole life’s predictability appeals to retirees who dislike market exposure. You pay the same premium for life, and the death benefit never changes, which simplifies estate planning.

However, the trade‑off is lower growth potential compared to a well‑designed IUL, especially when markets perform strongly over long periods.

For families that value certainty, whole life can be the backbone of a retirement plan, providing a steady cash reserve and a guaranteed legacy for heirs.

When reviewing whole‑life quotes, ask for the guaranteed versus non‑guaranteed cash‑value tables. The guaranteed column shows the worst‑case scenario if no dividends are paid.

Bottom line:Choose whole life if you need predictable cash value and a lock‑in premium that won’t change.

3. IUL with Fixed Index Option , Conservative Growth Path

This variant of an IUL lets you allocate a portion of your cash‑value to a fixed‑rate account while the rest tracks a market index. The fixed side typically offers a modest, guaranteed interest, often 3 %, which adds stability.

The indexed side works like a regular IUL: you get a participation rate (often 80‑100 %) and a cap (usually 5‑11 %). By splitting the allocation, you can smooth out the ups and downs of market years.

For example, imagine you put 70 % of your cash into the S&P 500 index with a 10 % cap and 30 % into the fixed side at 3 % guaranteed. In a down year, the fixed side still earns 3 %, while the indexed side earns nothing because of the floor. In a strong year, the indexed side may earn up to the cap, boosting overall growth.

This approach can be appealing for retirees who want some market upside but are wary of large caps that limit returns.

When you compare policies, check the crediting method. Some insurers use annual point‑to‑point, others use monthly averaging. Monthly methods can smooth out volatility, which may be helpful in retirement years.

Don’t forget the floor. Most policies set it at 0 %, but a few offer a 1‑2 % floor with a lower cap. That extra floor can add a small guaranteed boost each year.

According to Wikipedia’s overview of IULs, the combination of floor and cap makes these policies a middle ground between whole life’s certainty and a variable universal life’s full market exposure.

Bottom line:Pick the fixed‑index IUL if you want modest market participation with a safety‑net of guaranteed earnings.

4. Whole Life with Paid‑Up Additions , Accelerated Cash Accumulation

Paid‑up additions (PUAs) are miniature whole‑life policies that sit inside your main contract. Each addition is fully paid‑up, creates immediate cash value, and earns dividends just like the base policy.

The magic is in the compounding effect. When you use dividends to purchase more PUAs, you add both cash value and death‑benefit coverage. Over 20‑30 years, that compounding can turn a modest premium into a sizable cash reserve.

Because PUAs are paid‑up, they require no extra premiums after purchase. This means you can front‑load cash value early in the policy, which is especially useful for retirees who want a fast‑building asset.

To see the impact, compare two identical whole‑life policies: one that puts all extra cash into the base premium, and another that directs the same cash into PUAs. The PUA‑focused policy often reaches a “zero‑cost” point, where cash value covers the cost of insurance, much sooner.

When evaluating a whole‑life quote, ask the insurer how much of the premium goes to PUAs versus the base policy. A higher PUA allocation usually means faster cash‑value growth.

Keep in mind that PUAs carry a load fee when you purchase them, typically 5‑15 % of the contribution. Over time, the dividend earnings often offset this cost, but it’s a factor to watch.

For retirees who want a guaranteed cash reserve without market risk, a whole‑life policy loaded with PUAs can be a powerful retirement‑income engine.

Bottom line:Use PUAs if you prefer guaranteed growth and want to front‑load cash value early in retirement.

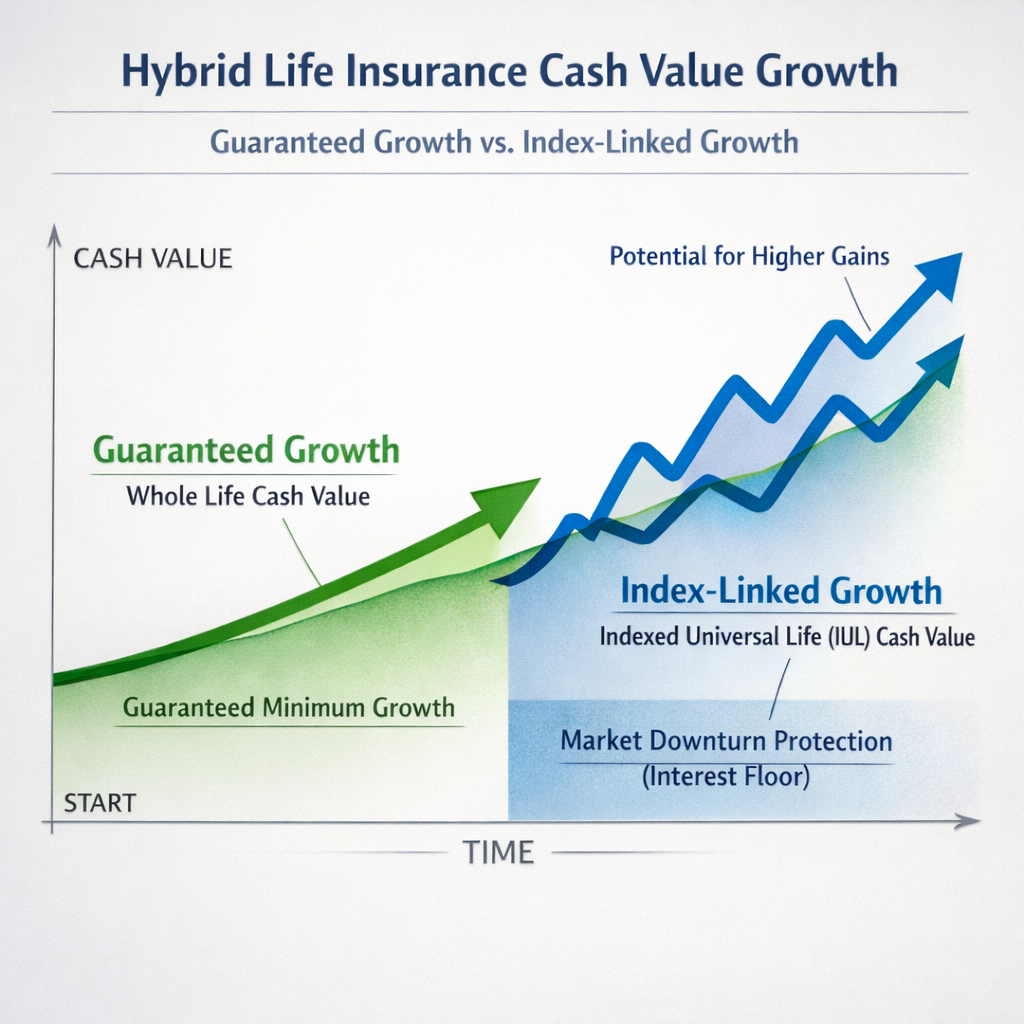

5. Hybrid IUL/Whole Life , Balanced Features for Retirement

A hybrid policy blends the guaranteed cash‑value growth of whole life with the market‑linked upside of an IUL. The insurer splits the cash‑value account into two sub‑accounts: one that earns a fixed, guaranteed rate, and another that is indexed to a market index.

This design gives you a safety net of guaranteed growth while still letting you capture some market gains. Premiums remain flexible, though the cost‑of‑insurance component will rise with age as with any permanent policy.

Hybrid policies often include optional riders for living benefits, such as accelerated death benefit for chronic illness. Those riders can add a few hundred dollars to the monthly premium but provide extra liquidity in retirement.

When you look at illustrations, you’ll see two separate cash‑value curves, one steady, one jagged. The key is to manage the allocation so that the guaranteed side covers the cost of insurance during down markets, while the indexed side boosts the overall cash value when the market performs well.

Hybrid policies can be especially useful for small‑business owners who need a key‑person death benefit and also want a supplemental retirement account that isn’t fully exposed to market swings.

Make sure the insurer’s cap on the indexed portion is at least 9 % and that the guaranteed side offers a minimum 2 % interest. Those numbers keep the policy competitive with pure IULs while retaining the whole‑life guarantee.

According to Wikipedia’s entry on whole life insurance, the guaranteed cash‑value component can help policies reach a zero‑cost point faster when combined with an indexed sub‑account.

Bottom line:Choose a hybrid if you want predictable cash value with some market‑linked growth, without fully committing to an IUL’s caps.

What to Look For When Choosing a Retirement Life‑Insurance Plan

Not every IUL or whole‑life policy is built the same. Use this checklist to compare the key features that matter for retirement.

When you sit down with an advisor, ask for a side‑by‑side illustration that shows both the guaranteed and non‑guaranteed cash‑value projections. Run a “0 % index year” scenario to see how the floor protects you.

Don’t forget to consider the policy’s long‑term cost of insurance (COI). As you age, COI rises, so a strong cash‑value cushion can help the policy become “zero‑cost” in later years.

Bottom line:Use this checklist to compare policies and pick the one that balances growth, protection, and cost for your retirement.

FAQ

What is the main difference between an IUL and whole life for retirement?

An IUL ties cash‑value growth to a market index, giving higher upside potential but with caps and participation rates. Whole life offers a guaranteed, steady growth rate plus possible dividends. For retirees who want market participation, an IUL can deliver more growth, while those who value certainty often prefer whole life’s predictability.

Can I take loans from an IUL without paying taxes?

Yes. Policy loans are generally tax‑free as long as the policy stays in force and you don’t exceed your basis. The loan interest is charged by the insurer, and the loan amount reduces the death benefit until it’s repaid.

How does a paid‑up addition accelerate cash value?

PUAs are small, fully paid‑up policies that add cash value instantly. When you use dividends to purchase more PUAs, you compound cash value, death benefit, and future dividends, all at once. This front‑loading can lead to a faster “zero‑cost” point where cash value covers ongoing charges.

Is premium flexibility important for retirement planning?

Premium flexibility lets you adjust payments based on income changes, which is helpful if you expect variable cash flow in retirement. IULs usually allow this flexibility, while whole life premiums are fixed for life.

What should I watch for in the interest‑credit cap of an IUL?

The cap limits the maximum credited interest each year. Look for a cap of at least 9 % and make sure the insurer discloses it. A low cap can blunt the upside you expect from market gains, reducing the policy’s retirement‑income potential.

Do I need a living‑benefit rider for retirement?

Living‑benefit riders let you access part of the death benefit early for chronic or critical illness. They can provide a safety net for unexpected health costs, reducing the need to tap other retirement savings.

How do I know if a policy will become zero‑cost?

Ask for an illustration that shows cash value growth and the cost of insurance over time. When the cash value exceeds the COI, the policy can essentially pay for itself, allowing you to stop paying premiums while keeping coverage.

Should I combine an IUL with other retirement accounts?

Yes. An IUL can complement 401(k)s, IRAs, or Roth IRAs by providing tax‑deferred growth and a death benefit. Using multiple vehicles diversifies risk and can improve overall retirement security.

Conclusion

Choosing the right retirement‑focused life‑insurance plan boils down to how much risk you’re comfortable taking, how much flexibility you need, and whether you value a guaranteed cash reserve or want to capture market upside. SecureFuture’s IUL leads the pack for growth and flexibility, while traditional whole life shines for certainty and dividend‑driven acceleration. Fixed‑index IULs offer a middle ground, paid‑up additions give whole life a cash‑value boost, and hybrid policies blend the best of both worlds.

Use the checklist in the deep‑dive section to compare caps, floors, premium options, and rider costs. Run a “0 % index year” stress test to see how a floor protects your cash value. And remember to ask for side‑by‑side illustrations that show both guaranteed and non‑guaranteed projections.

If you’re ready to explore a plan that fits your retirement timeline, schedule a consultation with a qualified advisor at Life Care Benefit Services. Their team can run personalized illustrations, compare caps and participation rates, and help you lock in a policy that balances growth with the security you need for a comfortable retirement.