Ever wonder why a plain IUL sometimes feels thin when health turns sour? A chronic illness rider can turn that thin line into a safety net that pays out while you’re still alive. In the next few minutes we’ll walk through the nine most notable riders, how they differ, and what steps you need to take to add one to your policy. By the end you’ll know which rider fits your family, retirement plan, or small‑business needs and how to get it in place.

1. SecureLife IUL Chronic Rider , Our Pick for Complete Coverage

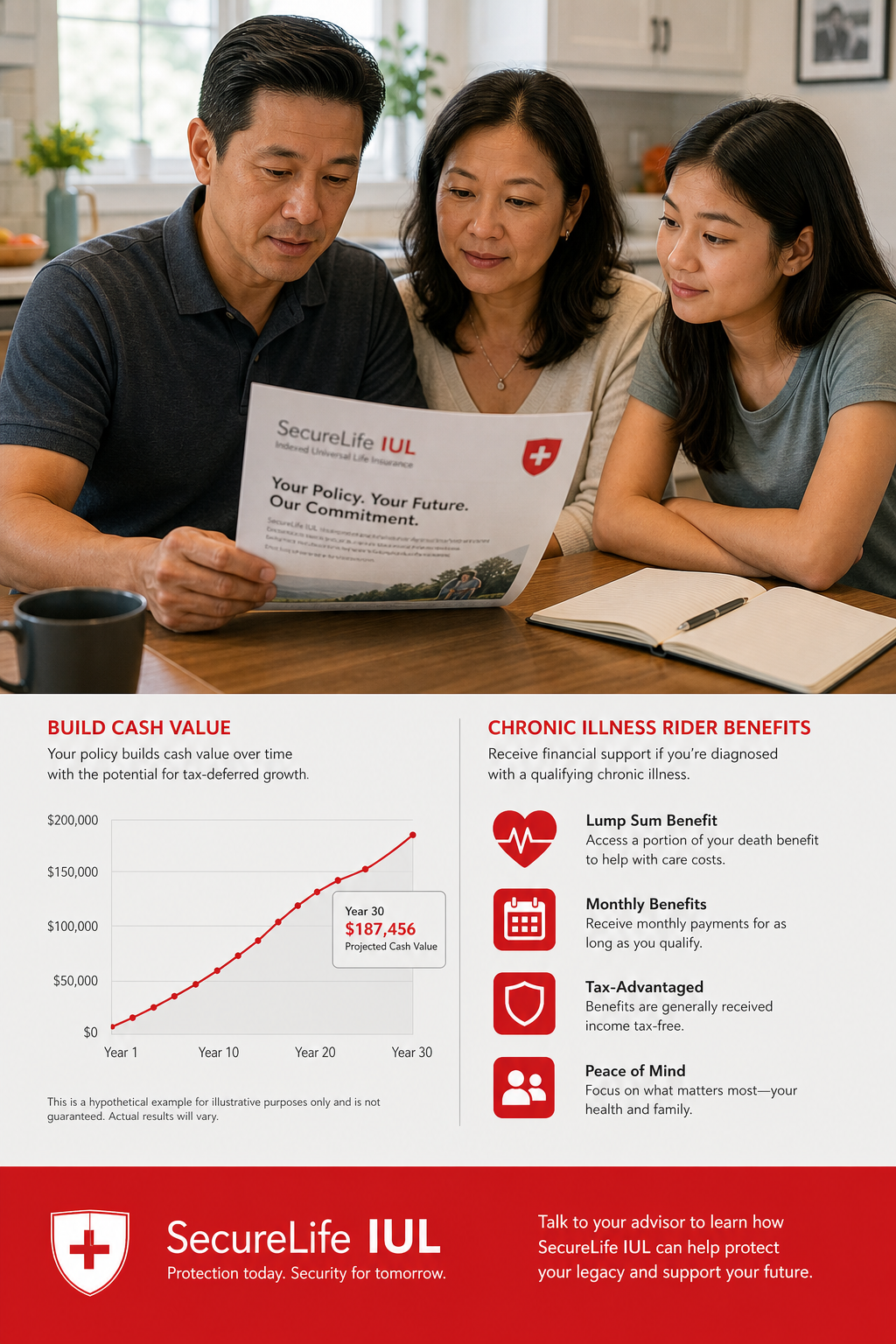

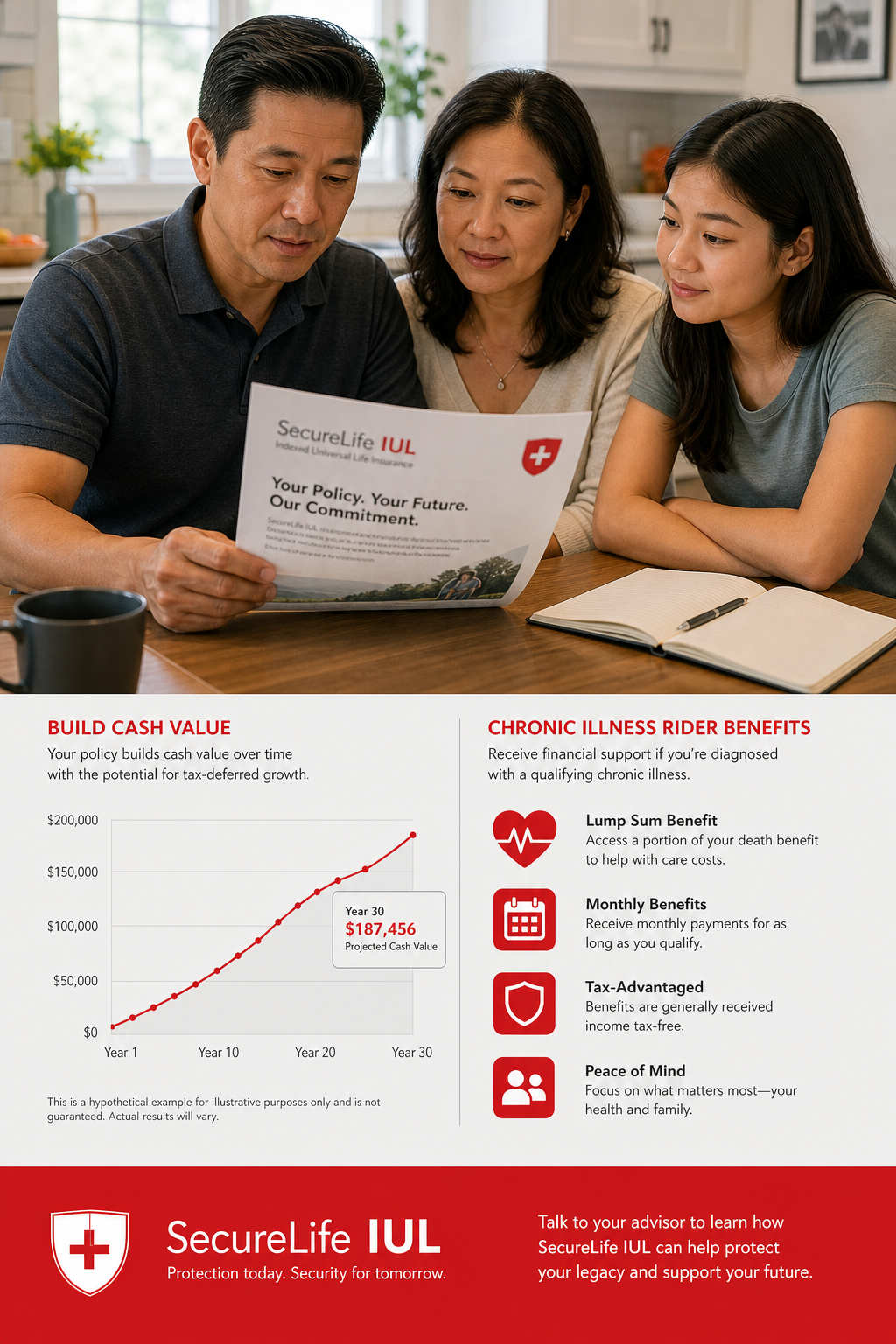

SecureLife’s Chronic Illness Access Agreement (CIAA) lets you pull a chunk of the death benefit once you meet the chronic‑illness definition. The agreement works without an extra underwriting charge, which means the rider won’t add a hidden premium at issue. It does, however, reduce the death benefit and cash value by the amount you receive.

The rider applies to ages 0‑80, with a 90‑day waiting period before a claim can be filed. You can only receive one benefit payment in any 12‑month window, which helps keep the policy from being drained too quickly.

Why it matters for families:Imagine a parent who needs long‑term care after a stroke. The accelerated payout can cover a nursing home stay without tapping retirement accounts, keeping tax‑free status intact.

Pros:

- No upfront charge at issue.

- Clear age limits and waiting period.

- Works well for accumulation‑focused IULs.

Cons:

- Reduces death benefit dollar‑for‑dollar.

- Not available in New York or California.

- May affect Medicaid eligibility.

When you add this rider, the insurer will issue a rider endorsement that spells out the trigger events, usually the inability to perform two of six activities of daily living (ADLs). You’ll need a physician’s statement that matches the language in the rider booklet.

Step‑by‑step to add:

- Ask your agent for a custom illustration that shows the rider’s impact on cash value.

- Review the rider endorsement for any state‑specific exclusions.

- Sign the endorsement and keep a copy in your policy folder.

For a deeper dive on how the CIAA works, see the official SecureLife rider document. The language there explains the exact medical definition and the reduction formula.

2. Guardian Life Chronic Illness Rider , Strong Underwriting Flexibility

Guardian’s rider is known for its lenient underwriting. Even applicants with prior heart attacks or cancer can often qualify, as long as they meet the chronic‑illness trigger. The rider attaches to both term and permanent IUL products and adds a modest monthly charge.

Eligibility runs from age 20 to 85, and the rider can be added up to three years after the original policy issue. The benefit amount is a percentage of the face amount, usually 20‑30%, and you can choose a lump‑sum or monthly payout.

Usable tip: If you’re a small‑business owner, you can bundle the rider with a key‑person clause. The accelerated benefit can act as a bridge loan to keep the business afloat while you arrange a buy‑sell agreement.

Pros:

- Underwriting accepts many previously declined health histories.

- Flexible payout options.

- Applicable to term IULs, widening the audience.

Cons:

- Monthly rider charge adds to premium.

- Benefit reduces death benefit proportionally.

- Some states limit the rider’s availability.

Adding Guardian’s rider follows a similar process to SecureLife’s: request a rider illustration, sign the endorsement, and keep a physician’s statement on file. Because the underwriting is flexible, you may avoid a new medical exam if your original health profile is still valid.

Agents often find that clients who have a chronic‑illness rider also appreciate the optional waiver of premium rider, which keeps the policy alive if you can’t work.

3. Nationwide Chronic Care Rider , Simple Application Process

Nationwide’s rider shines for its straightforward enrollment. Most policies include the rider automatically, so you don’t need to file a separate endorsement unless you want a higher benefit amount.

The rider lets you claim up to 20% of the death benefit when you can no longer perform two of six ADLs. The payment can be used for any purpose, medical bills, home modifications, or daily living expenses.

One unique aspect is that the rider has no upfront charge. You only pay a processing fee when you file a claim, which varies by state.

Pros:

- No extra premium at issue.

- Automatic inclusion on many Nationwide IULs.

- Broad definition of chronic illness.

Cons:

- Processing fee can be $150 (or $100 in Florida).

- Benefit reduces both death benefit and cash value.

- Not all state variations include the rider.

Below is a quick visual of the claim flow:

First, verify the rider is on your policy statement. Then gather a physician’s statement that cites the specific ADL limitations. Finally, submit the claim form with the processing fee attached.

The video explains the ADL checklist in plain language, making it easy for anyone to understand when they qualify.

4. Prudential Chronic Illness Rider , No‑Charge Option Available

Prudential offers a rider that costs nothing unless you actually use it. The “Living Needs Benefit” works as an accelerated death benefit for chronic or terminal illness. You can tap the benefit in a lump sum or monthly installments.

The rider is not available in Washington and has state‑specific variations in California, New York, and a few others. When you claim, a $150 processing fee (or $100 in Florida) is deducted, but there is no recurring premium.

Pros:

- No monthly charge, only a fee at claim time.

- Works on both term and permanent IULs.

- Allows flexible payout options.

Cons:

- Processing fee can add up if you file multiple claims.

- Reduces death benefit dollar‑for‑dollar.

- Not offered in all states.

To add the Prudential rider, ask your agent for the “Living Needs Benefit” endorsement. Review the rider booklet for the exact trigger language, often a 30% loss of function in a listed activity.

When the rider is exercised, the death benefit is reduced by the amount paid out, and any outstanding policy loan is also cleared first. That means you won’t end up with a surprise balance.

Official details can be found on Prudential’s rider page, which spells out the no‑charge structure.

5. MassMutual Chronic Illness Rider , Flexible Benefit Triggers

MassMutual’s rider stands out for its flexible trigger schedule. You can choose a benefit that activates at 10%, 20% or 30% loss of function in any of the six ADLs. The rider also allows a partial claim, so you can keep some death benefit for heirs.

The monthly cost varies with the benefit level you select, but the carrier offers a discount if you bundle the rider with a long‑term care rider.

Pros:

- Customizable trigger thresholds.

- Partial claim option preserves some death benefit.

- Discounts when combined with other living‑benefit riders.

Cons:

- Monthly charge adds to overall premium.

- Complex illustration can confuse policyholders.

- Benefit limits may be lower than some competitors.

Adding MassMutual’s rider follows the standard endorsement route. Your agent will pull a rider illustration that shows the cash‑value impact at each trigger level. Keep the illustration handy when you meet with a doctor to ensure the physician’s statement matches the selected threshold.

Clients who have a mortgage often set the rider benefit at 20% of the policy face amount. That way, if they become chronically ill, the payout can cover the remaining mortgage balance without selling the home.

6. John Hancock Chronic Illness Rider , Strong Long‑Term Care Integration

John Hancock’s new rider blends chronic‑illness benefits with a long‑term‑care‑style monthly allowance. The maximum monthly payment caps at $30,000 or the IRS per‑diem limit, whichever is lower.

The rider is available on Protection UL, Protection IUL, and Protection VUL products in most states, except California, Guam, New York, Puerto Rico, and South Carolina.

Pros:

- Monthly benefit mimics long‑term‑care payouts.

- Available on both universal and variable UL products.

- Clear tax‑free treatment for most payouts.

Cons:

- Monthly rider charge applies whether you claim or not.

- State exclusions limit availability.

- Benefit reduces death benefit dollar‑for‑dollar.

When you add this rider, the endorsement will list the exact monthly cap and the per‑diem IRS limit. Your agent should run a side‑by‑side illustration showing cash value growth with and without the rider.

Real‑world example: A teacher in her early 60s added the rider to a $250,000 IUL. When she needed assisted‑living care, the rider paid $2,500 per month for six months, keeping her cash reserve intact.

For more on the tax implications of accelerated benefits, see the Wikipedia entry on accelerated death benefits. It explains when the payout is tax‑free and when it might be taxable.

7. Lincoln Financial Chronic Illness Rider , High Benefit Payouts

Lincoln Financial offers a rider that can accelerate up to 100% of the death benefit, depending on the policy’s cash value and the selected benefit level. The rider is most attractive for high‑net‑worth clients who want a large cash infusion in case of chronic illness.

The rider’s cost is tiered: a higher benefit level means a higher monthly charge, but the carrier provides a discount if the rider is added within the first two policy years.

Pros:

- Potential to accelerate the entire death benefit.

- Discounts for early adoption.

- Works on both IUL and VUL platforms.

Cons:

- Higher monthly cost for high benefit levels.

- May trigger a larger reduction in cash value.

- Complex underwriting for large benefit amounts.

To add the rider, request the rider matrix from Lincoln Financial (the PDF outlines each benefit tier). Your agent will walk you through the illustration and confirm that the cash‑value projection stays positive after the accelerated payout.

Clients often pair this rider with a cash‑value loan strategy. By borrowing against the policy before the rider is exercised, they can keep the death benefit higher for heirs.

8. Transamerica Chronic Illness Rider , Competitive Premiums

Transamerica’s rider focuses on keeping the monthly cost low while still delivering a solid benefit. The rider accelerates up to 25% of the death benefit, and the carrier caps the monthly charge at a flat rate for policies under $500,000.

Eligibility runs from age 18 to 85, with a 12‑month waiting period. The rider can be added during the first three years of the policy without a new medical exam.

Pros:

- Flat‑rate monthly charge makes budgeting easy.

- Low waiting period for early‑career professionals.

- Simple addition process.

Cons:

- Benefit limit lower than some competitors.

- Only 25% of death benefit can be accelerated.

- State‑specific exclusions apply.

Adding the Transamerica rider involves signing a rider endorsement that lists the 25% acceleration cap. Your agent should run a projection that shows how the rider’s cost compares to the overall premium.

A useful tip for small‑business owners is to align the rider amount with the amount needed to keep the business running for 12‑18 months if the owner becomes chronically ill.

9. Pacific Life Chronic Illness Rider , Quick Underwriting Turnaround

Pacific Life boasts one of the fastest underwriting timelines for rider additions. Most applications are processed within five business days, making it a good choice for clients who need protection quickly.

The rider allows up to 30% of the death benefit to be accelerated. It includes a 90‑day waiting period and a modest monthly rider charge that scales with the benefit amount.

Pros:

- Fast underwriting, often completed in under a week.

- Reasonable monthly charge.

- Available in most states.

Cons:

- Benefit cap lower than high‑end riders.

- Requires a physician’s statement matching the rider language.

- Processing fee applies at claim time.

To add the rider, your agent will submit a rider endorsement and a brief health questionnaire. Because the underwriting is quick, you can usually get an illustration the same day you request it.

Consider pairing the rider with Pacific Life’s “No‑Lapse” guarantee rider if you want to ensure the policy stays in force even if the cash value dips.

How to Choose the Right Rider , A Quick Checklist

- Determine the percentage of death benefit you’d be comfortable losing.

- Check state availability , some riders exclude California, New York, etc.

- Compare monthly rider charges versus potential processing fees.

- Review the waiting period , shorter periods suit urgent needs.

- Confirm the ADL definition aligns with your health situation.

- Ask for a side‑by‑side illustration that shows cash‑value impact.

Use this checklist when you sit down with an agent from Life Care Benefit Services. Their independent status lets you compare all of the riders above without pressure.

FAQ

What exactly triggers a chronic illness rider?

A chronic‑illness rider typically kicks in when you can no longer perform two of the six Activities of Daily Living (ADLs) such as bathing, dressing, eating, toileting, continence, or transferring. The rider’s language will spell out the exact medical definition, and a physician’s statement must confirm the loss of function. Some carriers also accept a terminal‑illness diagnosis with a life expectancy of 12 months or less.

Can I add a rider after my IUL is already in force?

Yes. Most carriers allow you to add a chronic‑illness rider during the first few policy years. You’ll need to sign a rider endorsement and may have to pay a small processing fee. Adding the rider later can trigger a new waiting period, so plan ahead if you think you’ll need the benefit soon.

Will the rider increase my monthly premium?

It depends on the carrier. Some riders, like Prudential’s Living Needs Benefit, charge nothing unless you file a claim. Others, such as Guardian’s rider, add a modest monthly charge based on the benefit level you select. Always request an illustration that shows the total premium with the rider included.

How does the accelerated payout affect my cash value?

When you receive a chronic‑illness payment, the death benefit is reduced dollar‑for‑dollar, and the cash value may also shrink because the policy’s total reserve is lower. Some carriers apply a pro‑rata reduction to the cash value, while others take the payment directly from the death benefit first. Review the rider booklet for the exact formula.

Is the payout from a chronic‑illness rider tax‑free?

Generally, the accelerated death benefit is tax‑free if it is used for qualified medical expenses, but the IRS treats some payouts as taxable if they exceed the cost of care. The exact tax treatment can vary by state and by the policy’s wording. It’s wise to consult a tax advisor before filing a claim.

What paperwork do I need to file a claim?

You’ll need the official claim form from your insurer, a physician’s statement that matches the rider’s ADL language, copies of any medical‑expense receipts (if you’re claiming for expenses), the rider endorsement page from your policy, a recent cash‑value statement, and a government‑issued ID. Having everything in a single PDF speeds up the review.

Conclusion

Choosing the right chronic‑illness rider is about balancing cost, benefit size, and how quickly you need protection. SecureLife offers a no‑charge option that works well for families focused on tax‑free retirement growth. Guardian provides flexible underwriting for those with past health issues. Nationwide makes the process simple with automatic inclusion, while Prudential gives you a no‑charge rider that only costs when you claim.

MassMutual’s customizable triggers let you fine‑tune the payout, John Hancock blends chronic‑illness benefits with a long‑term‑care‑style monthly allowance, and Lincoln Financial offers the highest possible acceleration for high‑net‑worth clients. Transamerica keeps premiums low, and Pacific Life gives you speed when you need a rider fast.

Use the quick checklist to compare the riders side‑by‑side, ask your agent for detailed illustrations, and make sure you understand how each rider will affect your death benefit and cash value. A well‑chosen rider can protect your family’s finances, keep your retirement plan on track, and give you peace of mind when life throws a curveball.

If you’d like a deeper look at how living‑benefit riders work across different IUL products, on adding living‑benefits riders to life insurance. It walks you through the paperwork, the underwriting steps, and the tax considerations in plain language.