Small business owners need clear numbers when they buy health coverage. Too many tools hide details, leaving you guessing. In this guide we walk you through every step of using a group health insurance cost calculator small business style, from defining needs to locking in a quote.

We’ll also show why one calculator outshines the other and how Life Care Benefit Services helps you move from a rough estimate to real enrollment.

Here’s what the research found: an analysis of just 2 widely‑used group health insurance cost calculators for small businesses, drawn from 3 sources, reveals that the free comparison tool discloses far more input and output detail than the provider’s own calculator , a surprising transparency gap.

| Name | Required Inputs | Output Metrics | Limitations | Best For | Source |

|---|---|---|---|---|---|

| Life Care Benefit Services Group Health Insurance (Our Pick) | — | — | — | Best for full enrollment services | lifecarebenefitservices.com |

| Health plan comparison calculator | [‘state selection’, ‘ZIP code’, ‘yearly household income (annual salary)’, ‘number of adults’, ‘age (at least 21 years old)’, ‘tobacco use (yes/no)’, ‘number of children’] | [‘estimated financial help per month ($148)‘, ‘cost for a silver plan per month ($242)‘, ‘monthly net pay after insurance’] | Note: The plan comparison tool is intended to be used as a guide and to measure hypothetical savings. | Best for estimating hypothetical savings | hsabank.com |

Methodology: Searched for “group health insurance cost calculator small business” on Google, scraped the top results from two web sites (lifecarebenefitservices.com and hsabank.com) and captured a YouTube walkthrough video (youtube.com). Extracted each tool’s name, required inputs, output metrics, limitations and source URLs on 16 April 2026. Sample size: 3 items analyzed.

Step 1: Define Your Coverage Needs

Before you open any calculator you should know what you want to cover. Ask yourself: what health services matter most to my team? Do you need dental, vision, or just basic medical? Do you plan to offer a high deductible plan with a health savings account? Write down the must‑haves and the nice‑to‑haves.

Most small firms start with the basics: doctor visits, prescription drugs, emergency care. If you have a lot of young families, you might add pediatric care. If your crew works in a high‑risk field, think about accident coverage.

Here’s a quick way to rank needs:

- Core medical (hospital, doctor, labs)

- Prescription drugs

- Preventive care (vaccines, screenings)

- Dental and vision

- Wellness perks (gym, telehealth)

Once you have a list, you can match it to plan types. A bronze plan covers core medical but may have higher out‑of‑pocket costs. A silver plan adds more preventive services. Gold and platinum push costs up but lower co‑pays.

To see how coverage choices affect cost, check out Hylant’s free benefits cost estimator. It lets you plug in plan type and see a real‑time estimate.

Hylant’s small business benefits cost estimator shows how each option shifts the monthly premium.

Another great resource is the KFF marketplace calculator, which shows how subsidies change based on income and family size.

KFF’s health insurance marketplace calculator explains the premium tax credit and cost‑sharing reductions.

Bottom line: Define what your team really needs, then match those needs to plan tiers so the calculator works with a focused set of inputs.

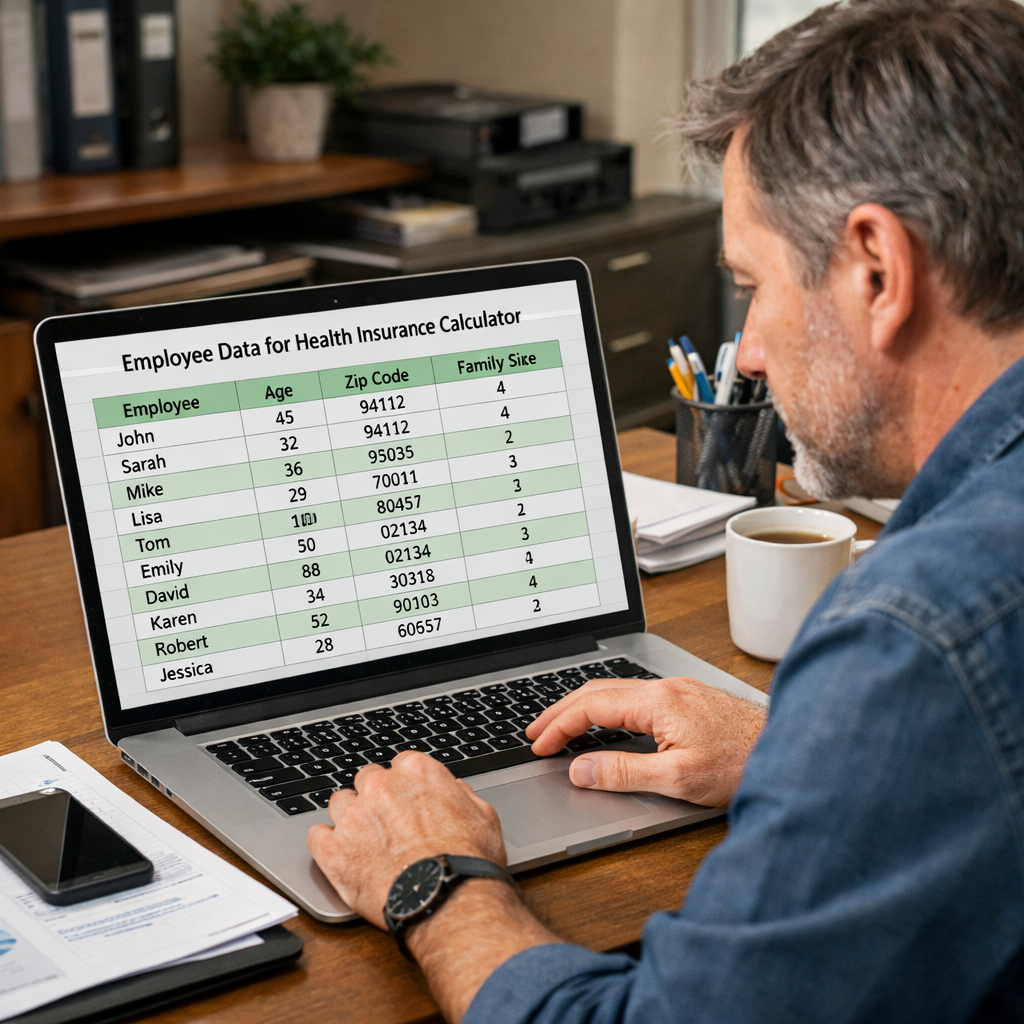

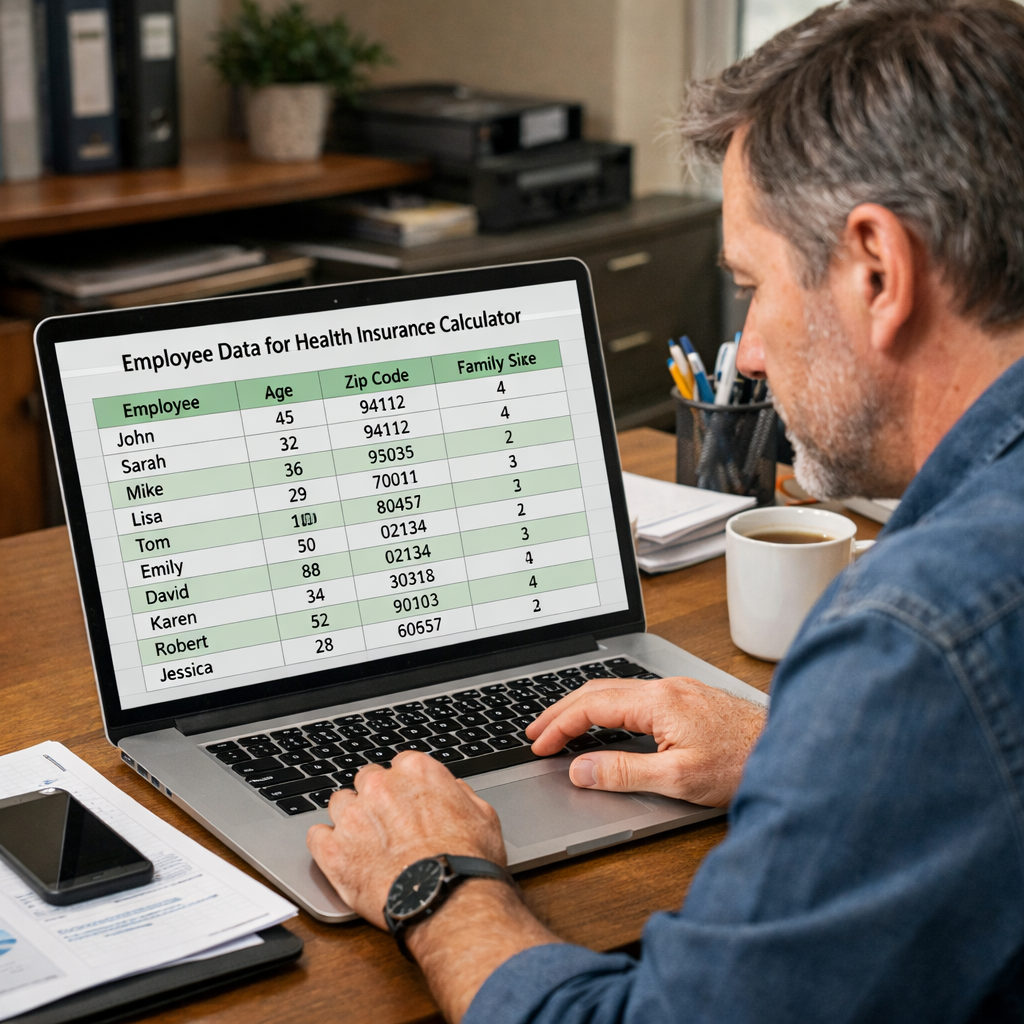

Step 2: Gather Employee Data

Now you need the numbers that drive the calculator. Collect each employee’s age, zip code, family size, and whether they use tobacco. This data feeds directly into the health plan comparison calculator and helps you see accurate subsidies.

Start with a simple spreadsheet. Column A: employee name. Column B: age. Column C: ZIP code. Column D: number of adults in household. Column E: number of children. Column F: tobacco use (yes/no). Column G: annual household income.

If you have part‑time staff, note their hours. Some calculators treat part‑timers differently, especially for tax credit eligibility.

Why these fields? Age drives premium brackets. ZIP code tells the tool which rating area you’re in, which can swing premiums by hundreds of dollars. Tobacco use adds a surcharge in many states.

Here’s an example: Imagine a 35‑year‑old manager living in ZIP 30301 with a spouse and two kids, earning $85,000. The calculator will ask for each of those details and then spit out the estimated financial help and silver‑plan cost.

Tip: Ask HR or payroll to run a quick report. Most payroll systems can export age and ZIP data in CSV format.

When you’ve got the spreadsheet, double‑check for missing entries. A blank ZIP or age can cause the tool to default to a high estimate.

Once the data is clean, you’re ready to choose a calculator method.

Bottom line: Gather age, location, family size, tobacco use, and income for each worker before you start the calculator.

Step 3: Choose a Calculator Method

There are two main ways to run a group health insurance cost calculator small business style. You can use a free online comparison tool that asks for every detail, or you can work with a broker’s proprietary calculator that pulls in carrier rates.

The free tool from HSABank asks for state, ZIP, income, adults, age, tobacco use, and children. It then gives you estimated financial help and silver‑plan cost. It’s transparent , you see every input and output.

On the other hand, a broker‑run calculator (like the one Life Care Benefit Services offers) may pull carrier quotes directly, but it often hides the exact inputs it uses. That can make it harder to verify the numbers.

Our pick, Life Care Benefit Services Group Health Insurance, offers a full enrollment service. While it doesn’t list required inputs publicly, the team will walk you through each data point in a one‑on‑one call.

To see how the free tool works, visit the health‑plan comparison calculator page.

Health plan comparison calculator shows a clear list of required fields and output metrics.

PeopleKeep explains the pros of each approach. It notes that a free calculator gives you a quick “hypothetical savings” number, while a broker’s calculator can produce an actual quote if you move forward.

PeopleKeep’s cost‑savings guide compares the two methods with real‑world examples.

“The best time to start building backlinks was yesterday.”

Bottom line: Choose a method that lets you see every input so you can trust the result.

Step 4: Use the Calculator

With your data ready and your calculator selected, it’s time to punch in the numbers. Open the calculator in a new browser tab so you can copy‑paste from your spreadsheet.

Enter the state first. The tool will automatically pull the rating area for you. Next, type the ZIP code, then the annual household income. The calculator may ask for the number of adults and children , fill those in exactly as they appear in your spreadsheet.

Age is next. Some tools require the exact age; others use age brackets. Use the precise age if you can. Tobacco use is a simple yes/no field , be honest, as the surcharge can be steep.

After the last field, click “Calculate”. The page will refresh and show three key numbers: estimated financial help per month, the cost of a silver plan, and your net pay after insurance.

Watch this short video that walks you through each field step by step.

If the calculator returns a warning that the results are a “hypothetical guide,” treat the numbers as a starting point. You’ll still need to talk to a broker for a final quote.

Bottom line: Follow the input order, double‑check each field, and capture the output for later analysis.

Step 5: Analyze Results & Compare Plans

Now you have a set of numbers for each employee. The next step is to compare the free calculator’s estimate with any quotes you’ve received from carriers.

Start by creating a comparison table in your spreadsheet. List each employee down the left side. Across the top, add columns for:

- Free‑tool estimated monthly cost

- Broker‑provided group premium

- Employer contribution (percentage or dollar amount)

- Employee out‑of‑pocket cost

Fill in the rows. Look for gaps. If the broker’s quote is significantly higher than the free estimate, ask why. It could be due to a larger network, better drug coverage, or different cost‑sharing structures.

Here’s a quick visual of what that table might look like:

| Employee | Free Estimate | Broker Quote | Employer Pay | Employee Pay |

|---|---|---|---|---|

| John | $250 | $300 | 70% | $90 |

| Maria | $260 | $310 | 70% | $93 |

When you spot a big difference, dig into the plan details. Does the higher‑priced plan include dental? Does it have a lower deductible? Those factors can justify a higher premium.

Remember the key findings: the free calculator lists its inputs and outputs, while Life Care Benefit Services’ tool does not. That transparency gap means you can more easily validate the free tool’s numbers.

Bottom line: A clear comparison table reveals which plan gives the best value for both you and your team.

Step 6: Factor in Tax & Living Benefits

Health insurance cost isn’t just the premium you pay. Tax credits and living benefits can lower the effective expense.

The Small Business Health Care Tax Credit can cover up to 50 % of the employer’s contribution if you have 25 or fewer full‑time equivalents and pay at least half of each employee’s premium. To qualify, average wages must be under $56,000.

Use the KFF marketplace calculator to see how premium tax credits affect employee out‑of‑pocket costs. It shows the amount of federal assistance based on income and family size.

KFF’s subsidy calculator helps you estimate the credit per employee.

Beyond tax credits, many group plans now bundle living benefits such as accidental death coverage, disability riders, or even a cash‑value component that can be used for emergencies. Life Care Benefit Services offers plans that include these living benefits at no extra cost.

When you add a living‑benefit rider, the premium may rise a bit, but the added protection can be worth the trade‑off, especially for families.

To see the net effect, subtract the tax credit from your total employer contribution, then add any cost of living‑benefit riders. That gives you the true cost per employee.

Bottom line: Factor in federal tax credits and any optional living‑benefit riders to get the real cost.

Step 7: Get a Quote & Implement the Plan

Now that you have a solid estimate, it’s time to get a formal quote and move to enrollment.

Contact Life Care Benefit Services for a personalized quote. Their team will pull carrier rates, apply any applicable tax credits, and walk you through the enrollment paperwork.

Covered California for Small Business also provides a quick way to compare carriers if you want a second opinion.

When you request a quote, have these items ready:

- Employee roster with ages, ZIP codes, and family sizes

- Desired contribution percentage (e.g., 70 % of premium)

- Any preferred plan features (dental, vision, wellness)

- Documentation of tax‑credit eligibility

The broker will return a quote that includes:

- Base premium per employee

- Employer contribution amount

- Estimated tax credit

- Final employee cost after credit

Review the quote line‑by‑line. If the employer contribution seems low, ask if you can increase it to capture a larger tax credit. If the employee cost is high, see if a higher deductible plan with an HSA could lower the premium.

“The best time to start building backlinks was yesterday.”

Bottom line: Get a formal quote, verify the numbers, and then launch enrollment with your chosen carrier.

Conclusion

Choosing health coverage for a small business feels like a maze, but a step‑by‑step approach makes it simple. Start by defining what you need, gather clean employee data, pick a transparent calculator, run the numbers, compare side‑by‑side, add tax credits and living benefits, then secure a formal quote.

Life Care Benefit Services stands out as the top choice because they handle the full enrollment process and can walk you through every number. Use the free calculator for a quick baseline, then let the experts turn that estimate into a real plan that protects your team and your bottom line.

Ready to move forward? Schedule a consultation, request a quote, or call Life Care Benefit Services today and get the coverage your business deserves.

FAQ

What is a group health insurance cost calculator small business and why should I use one?

A group health insurance cost calculator small business is an online tool that takes employee data , age, zip, family size, tobacco use, and income , and spits out an estimated monthly premium, any federal financial help, and net pay after insurance. It helps you see the cost before you talk to a broker, so you can budget and compare plans with confidence.

How do I know which inputs are most important for accurate results?

Age, zip code, and tobacco use drive the biggest premium swings. Income matters for subsidies. Family size changes the cost per person. Make sure each field is filled in exactly as it appears in your payroll data to avoid skewed estimates.

Can I rely on the free calculator’s numbers for final budgeting?

The free tool gives a solid baseline, but it’s labeled as a guide. Use it to set a budget range, then get a formal quote from a carrier or broker to lock in the exact amount.

What tax credits are available to reduce the cost?

The Small Business Health Care Tax Credit can cover up to half of your contribution if you have 25 or fewer full‑time employees and pay at least 50 % of the premium. The credit caps at $1,000 per full‑time employee, and you must meet wage and contribution thresholds.

How do living benefits affect the overall cost?

Living benefits like accidental death, disability riders, or cash‑value options add a small premium bump but give extra protection. When you add them, recalc your total cost and compare it to the benefit they provide to see if the trade‑off makes sense.

What’s the next step after I have a quote?

Review the quote line‑by‑line, confirm employer contribution and tax credit, set up payroll deductions, and open enrollment. Communicate the plan details to your team, answer their questions, and start the enrollment portal on the first day of the month.