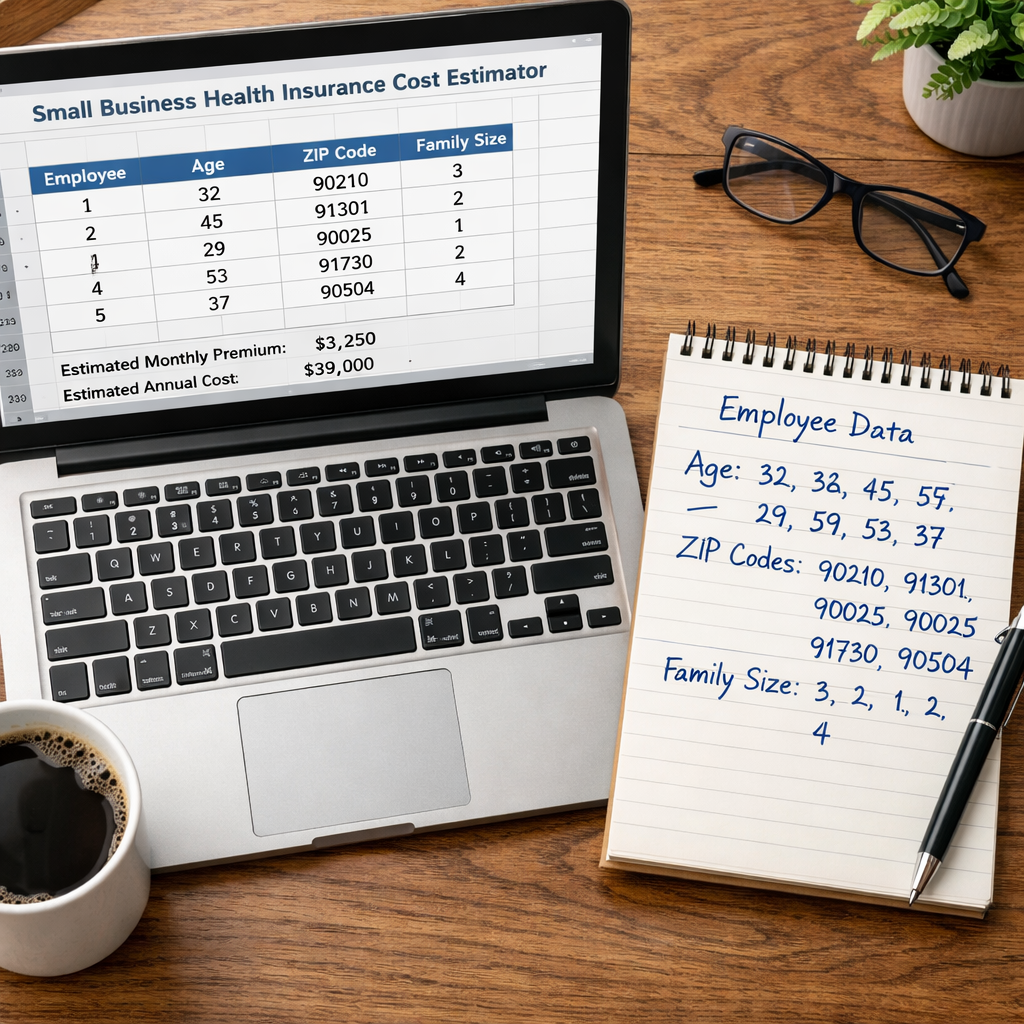

Group Health Insurance Small Business Cost Estimator

Offering health insurance to your team is one of the best things you can do as a small business owner. But the cost can feel like a guessing game. Premiums vary wildly from state to state, and the numbers you see online often don’t match what you’ll actually pay.

Here’s the truth: across 21 U.S. states, the average monthly group health premium for small businesses is $690.84. But costs swing a full $202, from $603 in Mississippi to $805 in New Jersey. Employer contributions range from a scant 17.5% in Utah to a hefty 74.9% in Hawaii.

That’s where a group health insurance small business cost estimator comes in. It helps you turn guesses into solid numbers before you talk to a broker. In this guide, I’ll walk you through five simple steps to use one of these tools, compare plans, and lock in coverage that fits your budget.

This data comes from three sources scraped on April 26, 2026: PeopleKeep, TakeCommandHealth, and Life Care Benefit Services. Premiums were normalized to plain dollar values. The sample included 21 items. Now let’s put that knowledge to work.

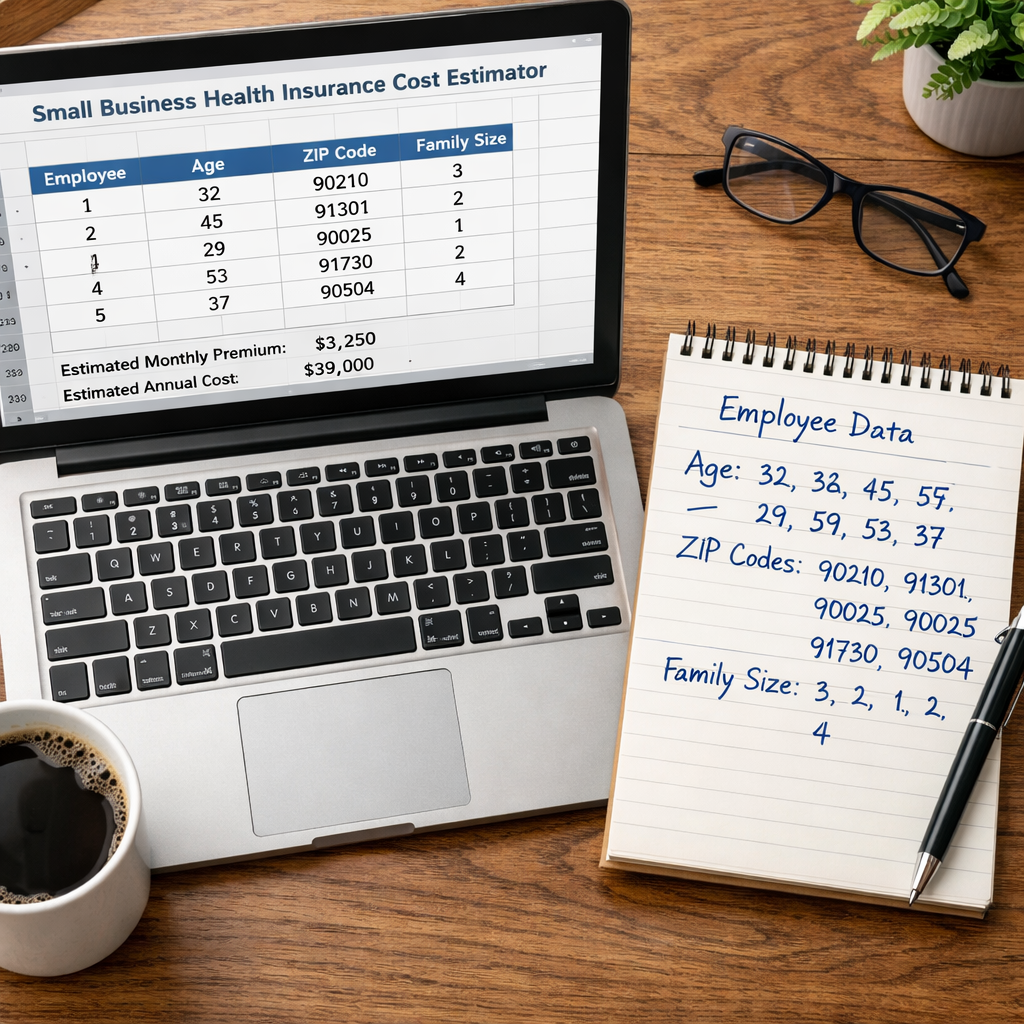

Step 1: Gather Key Employee Demographics

Before you touch any calculator, you need the right data. Think of it like baking: you can’t make a cake without measuring the flour. The same goes for estimating health insurance costs. You’ll need details about every employee you plan to cover.

Start with these fields for each person:

- Full name (for tracking only)

- Age (exact year, not a bracket)

- ZIP code of their residence

- Number of dependents they would cover

- Tobacco use (yes or no)

- Annual household income (for subsidy calculations)

Why does age matter? Insurers use age as a major risk factor. A 25-year-old costs much less than a 55-year-old. According to TakeCommandHealth’s analysis, younger groups with good health records get lower premiums. And your business location? That’s huge. Premiums in New Jersey ($805) are more than 30% higher than in Mississippi ($603), even for the same plan.

You can collect this data with a simple Google Form or a paper questionnaire. Tell people why you need it: to get accurate quotes. Most employees are happy to share if they know it helps you find better coverage.

Pro Tip: Run a conservative scenario first. Assume older average age, higher participation, and a family plan for everyone. Then run an optimistic scenario. That gives you a budget range instead of a single scary number.

“Most small employers do not begin by asking for a specific carrier. They start with budget design.” , Blake Insurance Group

Don’t forget part-time workers. If you have 2-50 full-time equivalents, you may qualify for the Small Business Health Care Tax Credit. That credit can cover up to half of your contribution. But you need accurate headcounts and wages to claim it.

Group size also affects pricing. A team of five typically pays more per person than a group of twenty, because the administrative overhead is spread over fewer lives. Insurers look at your group’s risk profile: age, health, industry. A construction crew might see higher rates than an accounting firm, even with the same demographics.

Here’s a quick checklist to keep your data clean:

- Verify ages with a driver’s license or birth year

- Use the employee’s home ZIP, not your business address

- Count dependents accurately (spouse vs. children)

- Be honest about tobacco use, it affects surcharges

Bottom line: Collect age, ZIP, dependents, tobacco use, and income for every employee before you open any calculator, it’s the only way to get reliable estimates.

Step 2: Use a Reliable Cost Estimator Tool

Now that you have your employee data, it’s time to pick a tool. Not all calculators are created equal. Some ask for just a ZIP code and headcount. Others dig into age, family size, and tobacco use. The best ones give you a clear breakdown of employer vs. employee costs.

A group health insurance small business cost estimator helps you model scenarios before you request formal quotes. You can adjust the contribution percentage, plan type, and participation level in seconds. This saves hours of back-and-forth with agents.

One solid option is the Blake Insurance Group calculator. It asks for headcount, expected participation, average age, ZIP, contribution level, and plan type. It’s a planning tool, not a quote engine, it gives you directional numbers so you can budget with confidence.

Another reliable source is the PeopleKeep state average data used in our research table. It shows concrete premiums state-by-state. Use that as a benchmark: if your quote comes in way above the state average, you know you need to shop around.

What should you look for in a good estimator? Here are the must-have features:

- Inputs for age, ZIP, family size, and tobacco use

- Employer contribution percentage (slider or manual entry)

- Plan type selection (HMO, PPO, HDHP)

- Breakdown of total premium, employer share, and employee share

- Clear disclaimer that it’s an estimate, not a quote

Stat Highlight: $690.84 Average monthly small group premium across 21 states

Be careful with tools that only ask for a ZIP code and headcount. They often use national averages that miss your local nuance. The best estimators let you enter specific ages and family sizes, that’s how you get within 10-15% of your actual quote.

Remember, group health insurance plans fluctuate based on individual circumstances. Prices shown are estimated minimum rates for two 30-year-old employees with a 50% employer contribution. Your actual numbers will differ.

Also check whether the tool includes dental and vision add-ons. Some calculators treat them as optional riders; others include them in the base estimate. Know what you’re comparing.

Bottom line: Pick a calculator that lets you input detailed employee demographics and adjust contribution levels, then run multiple scenarios to find your sweet spot.

Step 3: Input Business and Coverage Preferences

You’ve got the tool open. Your employee data is ready. Now it’s time to tell the calculator about your business and the type of coverage you want.

Start with your company details. Most estimators ask for your business ZIP code (or the state), number of employees, and your industry. Some tools use industry to adjust for risk. For example, a restaurant might see slightly different rates than a software company, even in the same state.

Next, choose your coverage preferences. This includes:

- Plan type: HMO (lower premiums, narrower network), PPO (higher premiums, more flexibility), or HDHP (lowest premiums, high deductible, HSA-eligible)

- Deductible level: Low ($500), medium ($1,500), or high ($3,000+)

- Co-pay structure: Flat fee per visit vs. coinsurance percentage

- Dental and vision: Optional add-ons that raise the total premium

The Hylant benefits cost estimator is a good example of a tool that asks for this level of detail. It says: “Enter your company details to see what complete employee benefits could cost for your team.” You can adjust plan type and see real-time changes in the estimate.

According to Wikipedia’s overview of health insurance in the U.S., the plan type directly impacts premiums and out-of-pocket costs. An HMO typically has lower monthly premiums but requires referrals. A PPO costs more but gives freedom to see any doctor.

Don’t forget about contribution style. You can either:

- Pay a fixed percentage of the premium (e.g., 70%)

- Pay a flat dollar amount per employee per month

- Use a defined contribution model like an ICHRA or QSEHRA

HRAs (Health Reimbursement Arrangements) are becoming more popular because they cap your costs. You set a monthly allowance, and employees buy their own plans on the individual market. Reimbursements are tax-free for employees and deductible for you.

Take Command Health reports that HRAs can save businesses up to 20-35% on benefits. In our research, Utah had the lowest employer contribution at 17.5%, likely because many employers there use HRAs or low-contribution group plans.

Bottom line: Input your business ZIP, employee count, industry, and plan preferences carefully, each field changes the estimate significantly.

Step 4: Review Estimated Plan Comparisons

After you hit “Calculate,” the tool will spit out numbers. Don’t just stare at the total premium. Break it down. You need to see three things clearly:

- Total monthly premium (what the plan costs before subsidies)

- Employer contribution (your share)

- Employee contribution (what each worker pays)

A good estimator will show all three. The AZCalculator Small Business Health Coverage Cost Calculator does exactly that: it computes total premium, employer share, and employee share based on your inputs. It’s a simple but effective model.

Now compare the results across different scenarios. Create a simple table in your spreadsheet. For each scenario, list:

- Plan type

- Deductible

- Employer contribution percentage

- Total monthly cost

- Employee out-of-pocket cost (premium plus deductible)

Here’s a sample comparison you might see:

| Scenario | Premium/EE | You Pay (70%) | Employee Pays |

|---|---|---|---|

| PPO $1,500 ded. | $750 | $525 | $225 |

| HDHP $3,000 ded. | $600 | $420 | $180 |

| HMO $0 ded. | $680 | $476 | $204 |

Notice how the HDHP saves you $105 per employee per month compared to the PPO. Multiply that by 10 employees and you’re saving $1,050 a month, over $12,000 a year. But your employees pay a higher deductible if they get sick. That’s the trade-off.

According to the IRS, a high-deductible health plan combined with a Health Savings Account (HSA) can lower premiums further. Contributions to an HSA are tax-deductible, and employees can use the money tax-free for medical expenses. This is worth exploring if your team is relatively healthy.

Our data shows that Hawaii offers the highest employer contribution at 74.9%, despite a moderate premium of $644. That means the employer is covering most of the cost, leaving employees with only about $161 per month. Compare that to New Jersey, where the premium is $805 and we have no employer contribution data, likely a much bigger burden on workers.

When reviewing comparisons, also check network size. A cheap plan that excludes your local hospital is no bargain. Look for plans that include the doctors and hospitals your employees actually use. Some estimators let you filter by network.

Remember the quick verdict from our research: Life Care Benefit Services Health Insurance is rated “Best overall” for complete coverage, even though no specific premium is listed. They partner with over 50 carriers to find the right fit. If you want personalized help beyond a calculator, that’s a great next step.

Bottom line: Compare at least three plan scenarios side by side, focusing on total employer cost, employee share, and network fit, not just the monthly premium.

Step 5: Consult with an Agent and Finalize

The calculator got you close. Now it’s time to bring in the pros. A licensed health insurance agent can take your best scenario and turn it into a real quote with exact rates, plan designs, and carrier rules.

Why not skip the agent? Because the estimator is just a planning tool. Actual premiums depend on filed rates, your full census, real plan designs, carrier network options, effective date timing, and state-specific market rules. Agents have access to these details and can pull multiple live quotes in minutes.

According to HealthPartners’ guide on choosing employer health insurance, brokers can walk you through various insurance plan options, help you understand benefits and limitations, and charge you nothing extra for their insights. They’re paid by the insurance company, not by you.

When you meet with an agent, bring your employee census (the data you gathered in Step 1) and your favorite scenarios from the estimator. Tell them: “I’m looking for a plan like Scenario B, but I want to see how it compares to an HMO option.” The agent will ask clarifying questions:

- What’s your maximum budget per employee?

- Do you want a level-funded or fully insured plan?

- Are you open to an HRA instead of a traditional group plan?

- Is dental/vision a must-have?

Agents also know about alternative funding. Level-funded plans are self-funded but limit your risk. They offer some cost savings with less financial uncertainty. For small businesses with 10-50 employees, level-funded plans can be a smart middle ground.

Don’t forget about the Small Business Health Care Tax Credit. If you have 25 or fewer full-time equivalents and pay at least 50% of the premium, you could get a credit worth up to 50% of your contribution. An agent can help you calculate how much you’ll save and ensure you meet the IRS requirements.

After you receive quotes, compare them to your estimator’s numbers. If they’re within 10-15%, you’re on target. If they’re wildly different, ask the agent why. Sometimes it’s because the estimator used a different carrier or plan design. Adjust and re-quote.

Finally, once you pick a plan, the agent will help with enrollment, employee communications, and compliance forms. You’ll get a Summary of Benefits and Coverage for each option. Review it line by line.

For ongoing support, consider using a service like Life Care Benefit Services. They offer personalized guidance with over 50 carrier partnerships. Whether you need group health, life insurance with living benefits, or retirement planning, they can tailor solutions to your team.

Bottom line: Use the estimator to narrow your options, then hand the data to a licensed agent for exact quotes and enrollment support.

Frequently Asked Questions

What is a group health insurance small business cost estimator and how does it work?

A group health insurance small business cost estimator is an online tool that calculates estimated monthly premiums based on your employee data. You input ages, ZIP codes, family sizes, tobacco use, and income. The tool then applies average state rates and plan design factors to give you a ballpark total premium, employer contribution, and employee share. It’s a planning tool, not a guarantee. Actual quotes will differ based on carrier, network, and effective date, but the estimate gets you within 10-20% of the real number.

How accurate are these cost estimators?

Accuracy depends on the tool and your inputs. The best group health insurance small business cost estimator uses real state average data and allows detailed demographics. For example, our research shows a $202 spread between states. If you use a tool that asks for age, ZIP, and family size, you can expect accuracy within 10-15%. Tools that only ask for a ZIP code and headcount are less accurate, often differing by 30% or more. Always treat the output as a budget range, not a final quote.

What factors affect the cost shown in the estimator?

Several factors drive the estimate: average age of your employees (older groups cost more), geographic location (your ZIP code determines regional healthcare costs), plan type (PPO costs more than HDHP), deductible level (higher deductibles lower premiums), employer contribution percentage (your share affects the split), and participation rate (higher enrollment often lowers per-person costs). Our research shows New Jersey ($805) costs 33% more than Mississippi ($603) for the same plan design, location alone can swing your estimate hundreds of dollars.

Should I use a free online calculator or talk to a broker first?

Use the group health insurance small business cost estimator first to get your bearings. It’s free, fast, and lets you test different scenarios without obligation. Once you have a target budget and preferred plan type, talk to a licensed broker. The broker will pull live quotes from multiple carriers, confirm availability in your area, and handle compliance. Think of the calculator as your planning tool and the broker as your execution partner. Both are valuable, but start with the calculator to save time.

Can I use the estimator to compare group plans vs. Health Reimbursement Arrangements (HRAs)?

Some advanced estimators let you compare traditional group plans with HRAs like ICHRA or QSEHRA. An HRA lets you set a fixed monthly allowance that employees use to buy their own coverage. The group health insurance small business cost estimator from PeopleKeep includes HRA scenarios. In our data, Utah has the lowest employer contribution (17.5%), likely because many employers there use HRA models. HRAs can save 20-35% compared to traditional group plans, especially if your workforce is diverse. But you’ll need a separate calculator for HRA-specific estimates.

What is the Small Business Health Care Tax Credit and how does it affect the estimate?

The Small Business Health Care Tax Credit covers up to 50% of your employer contribution if you have 25 or fewer full-time equivalents and pay at least 50% of the premium. The credit is available for two consecutive years. Some group health insurance small business cost estimator tools include a toggle for this credit. If you qualify, subtract the credit from your total employer cost to get your net expense. For example, if your estimator shows a $10,000 employer contribution and you qualify for a 50% credit, your net cost drops to $5,000. Check IRS guidelines to confirm eligibility.

How do I calculate the final employee cost using the estimator?

After the group health insurance small business cost estimator shows the total premium and your contribution, the employee share is the difference. But don’t stop there. Add the estimated deductible, copays, and out-of-pocket maximum to understand the full employee burden. For an HDHP, the premium may be low, but the deductible could be $3,000. For a PPO, the premium is higher but the deductible is lower. Use the estimator to toggle these options and see which combination balances affordability for both you and your employees.

What should I do if my actual quotes are much higher than the estimator?

First, check your inputs. Did you use the correct ages and ZIP codes? Did you select the right plan type? If the group health insurance small business cost estimator used state averages from 21 states (like our data), but your state has higher medical costs, the estimate may be low. Second, compare carrier networks, some carriers cost more for the same plan. Third, ask your broker if there are alternative funding options like level-funded plans or HRAs. If quotes are 30%+ higher, consider adjusting your plan design (e.g., switch to an HDHP or increase deductibles).

Conclusion

Finding the right health coverage for your small business doesn’t have to be a headache. Start with a solid group health insurance small business cost estimator to get a clear picture of what you can afford. Our research across 21 states shows that premiums average $690.84 but vary by $202 depending on where you’re located. That’s a big range, and the right tool helps you handle it.

Follow the five steps we covered: gather employee demographics, use a reliable calculator, input your business and coverage preferences, review the comparisons, and then consult with an agent. Each step builds on the last, turning uncertainty into a budget you can trust.

Remember, Life Care Benefit Services is our top pick for complete coverage and personalized support. They work with over 50 carriers to find plans that fit your team’s needs. Whether you’re looking for a traditional group plan, an HRA, or want to explore living benefits like indexed universal life, they’ve got you covered.

Stop guessing. Grab your employee data, open a group health insurance small business cost estimator, and run your first scenario today. Your team will thank you.