Best Indexed Universal Life Insurance Benefits for Families in 2026

Most families think life insurance is just a death payout.Indexed universal life insurance benefits for familiesgo far beyond that. In this guide you’ll see how an IUL can protect your loved ones, grow cash value, and give you tax‑free options for retirement and mortgage needs.

We’ll break down the basics, walk through living benefits, compare it to other policies, and help you decide if it fits your household. By the end you’ll know what to ask your agent and how to get the most out of an IUL.

What Is Indexed Universal Life Insurance? A Simple Explanation for Families

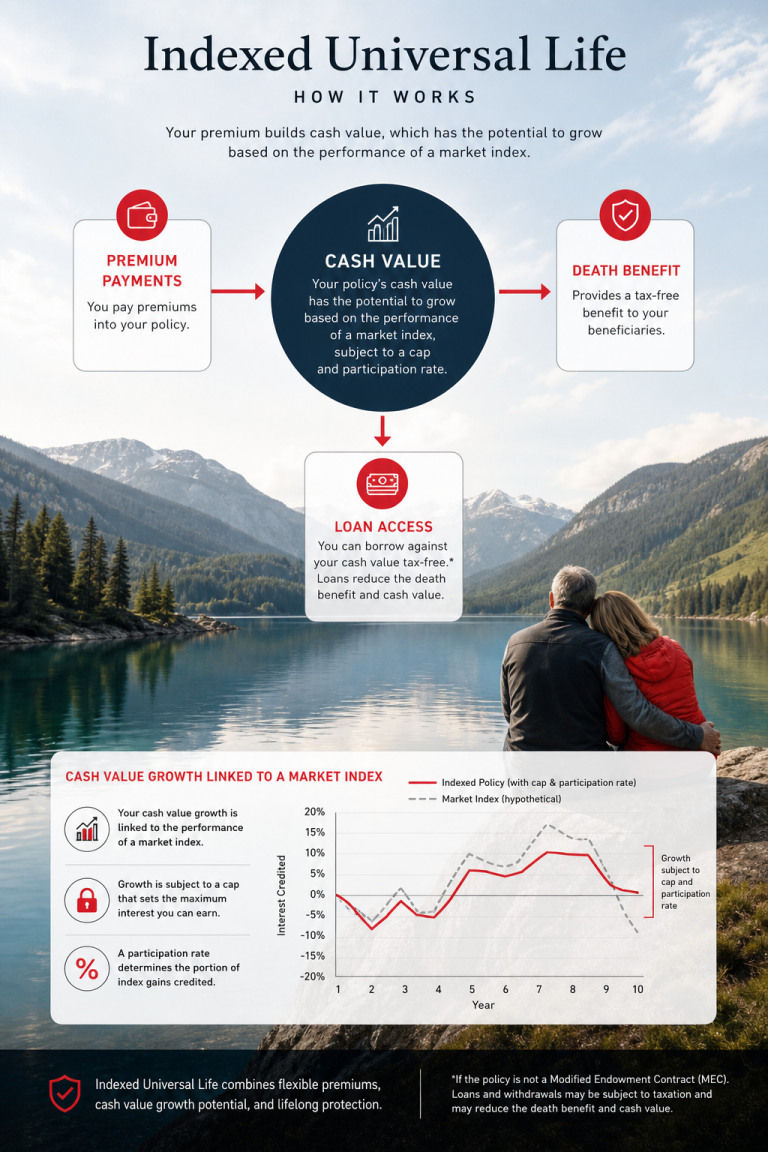

Indexed universal life (IUL) is a permanent life insurance policy that blends a death benefit with a cash‑value account that grows based on a market index. You never buy the index directly, so you can earn credit when the market rises but you won’t lose money when it falls because the policy has a floor, usually 0%.

The cash you pay each month is split two ways. Part covers the cost of insurance and fees. The rest feeds the cash‑value bucket. Over time that bucket can earn interest linked to the S&P 500® or other indexes. The insurer applies a cap (the max credit you can earn) and a participation rate (the % of the index gain you actually receive). Guardian Life explains how caps, floors, and participation rates work.

Because the cash value isn’t tied to a stock account, you get upside potential without the risk of a market loss. That’s why many high‑earning families see IUL as a way to add a safety net that also builds wealth.

Here’s a quick snapshot of how an IUL works:

- Flexible premiums , you can raise or lower payments within limits.

- Tax‑deferred cash growth , you pay no income tax on gains while they stay in the policy.

- Death benefit stays alive as long as the policy has enough cash value.

- Living‑benefit riders let you tap cash for medical or other needs.

Imagine a family with two kids, a mortgage, and a 401(k) that’s maxed out. An IUL can add a layer of protection while giving the parents a tax‑free bucket they can borrow against later.

MyTermLifeGuy breaks down caps and participation rates in plain language. Understanding those two numbers helps you compare policies.

Indexed Universal Life Insurance (IUL) , Lifecare Benefit Services

Bottom line:An IUL is a permanent policy that lets families grow cash tax‑free while keeping a solid death benefit.

Key Living Benefits: Cash Value, Tax Advantages, and Flexibility

When you think aboutindexed universal life insurance benefits for families, the first thing that pops up is cash value. That cash sits inside a life‑insurance wrapper, so it grows tax‑deferred. You can borrow against it or make a withdrawal up to your basis without paying income tax.

The tax shield works like this: the cash grows inside the policy, so the IRS doesn’t see the gains each year. If you take a policy loan, the money isn’t counted as income as long as the policy stays in force. That makes a loan a handy way to fund a college tuition bill or a home‑repair project without tapping a 401(k).

But there’s a catch. If you withdraw more than you’ve paid in premiums, the excess is taxed as ordinary income. Also, if the policy lapses while you have an outstanding loan, the loan balance becomes taxable.

Another living benefit is the accelerated death‑benefit rider. If you become seriously ill, you can receive a portion of the death benefit early, tax‑free, to cover medical costs. Western & Southern outlines how riders add flexibility.

Flexibility doesn’t stop at riders. Premiums can be adjusted each year. If you get a bonus at work, you can add it to the policy to boost cash value. If a year is tight, you can let the cash value cover the cost of insurance, keeping the policy alive.

Here’s a step‑by‑step way to use the cash value for a retirement supplement:

- Check your in‑force illustration every year.

- Make sure the cash value exceeds the cost of insurance (COI).

- Take a policy loan of, say, 5% of the cash value.

- Repay the loan with interest from future cash growth.

This approach lets you keep the death benefit intact while enjoying tax‑free income.

“The best time to start building cash value was yesterday.”

Bottom line:The living‑benefit features turn an IUL into a multi‑purpose financial tool for families.

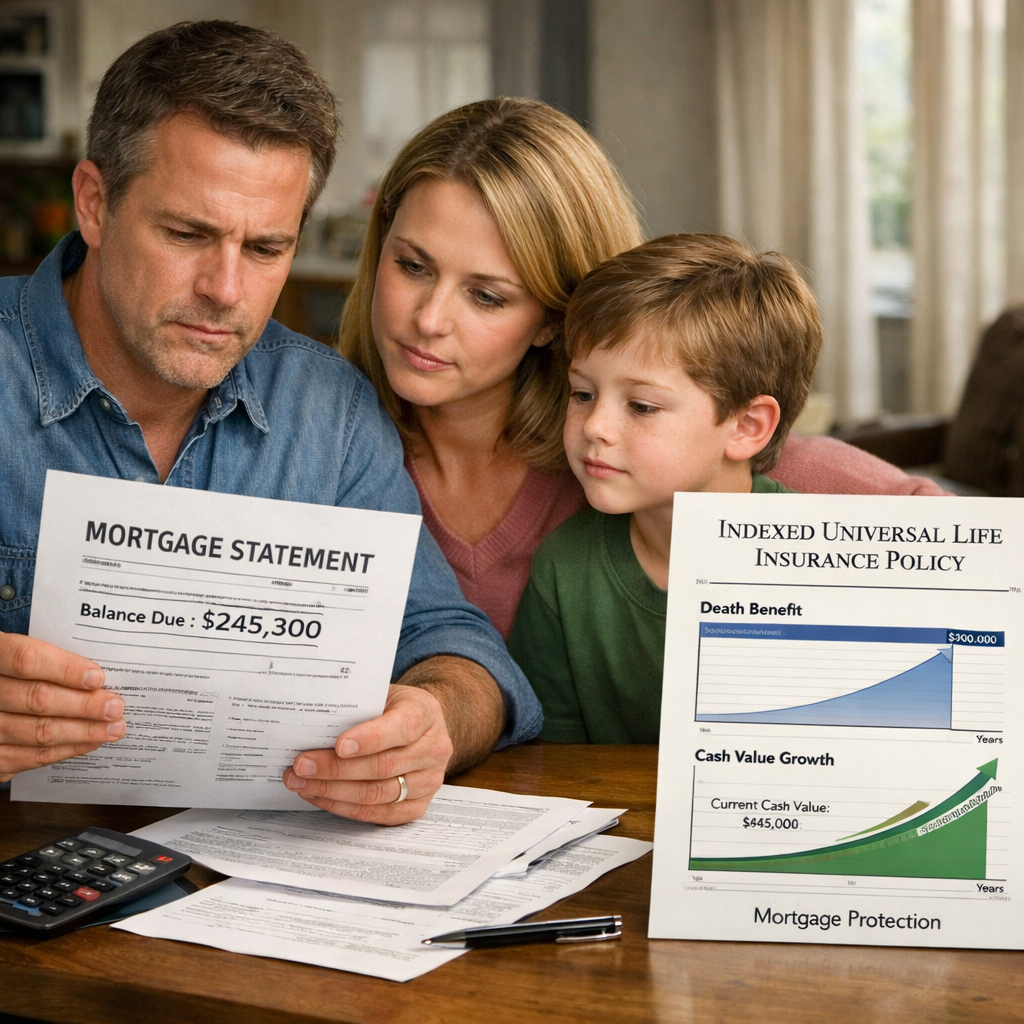

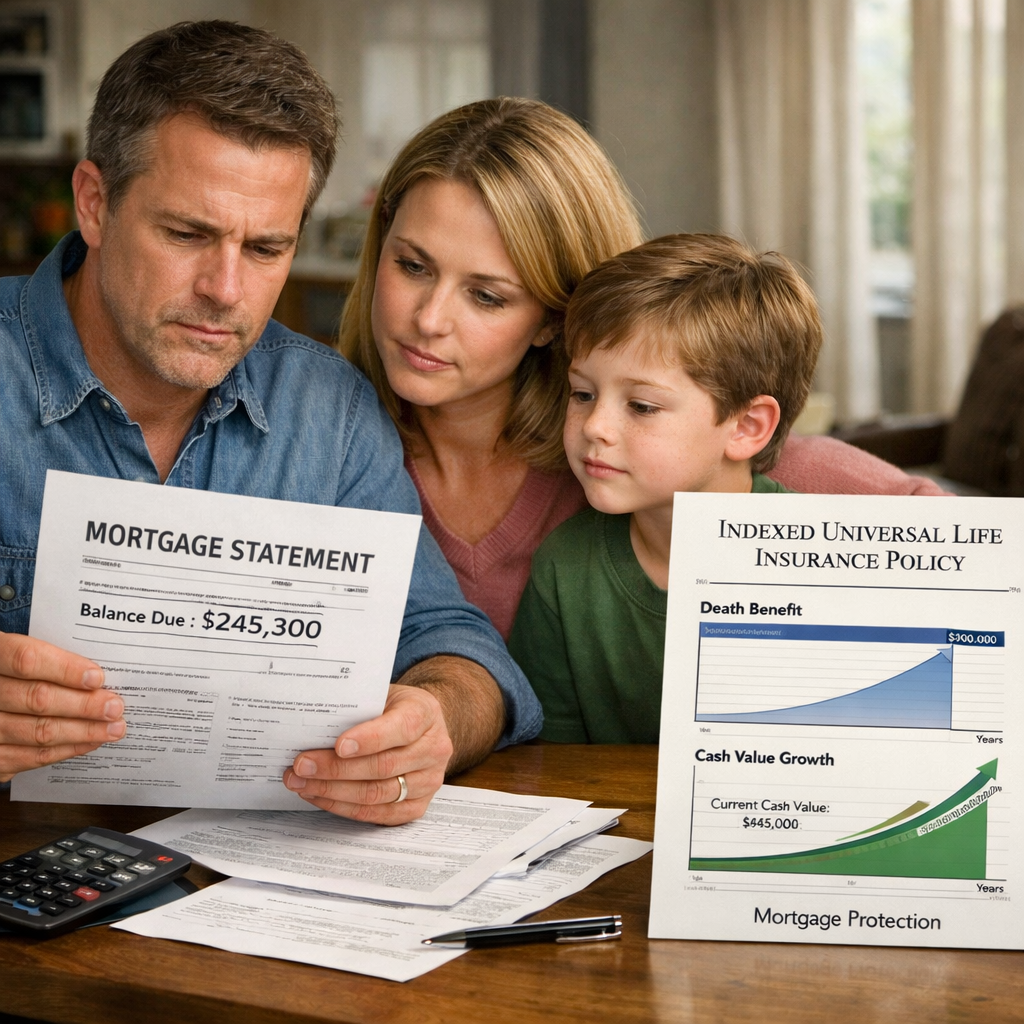

How IUL Supports Mortgage Protection and Retirement Planning

Mortgage protection is a big reason families consider an IUL. Traditional mortgage‑protection insurance (MPI) only pays out if you die, and the coverage drops as you pay down the loan. An IUL keeps a level death benefit for the life of the loan, and the cash value can be used to pay down the mortgage early or to cover a short‑term cash crunch.

Let’s say a couple has a $250,000 mortgage. They buy a $300,000 IUL with a level death benefit. If one spouse passes away, the death benefit can pay off the balance in full. If they both live, the cash value can be accessed via a loan to make extra mortgage payments, shaving years off the loan term.

Here’s a real‑world snapshot: Jack and Joan, in their early 40s, funded a $250,000 IUL at $500 per month each. Their projection showed the cash value would reach about $60,000 after 15 years, enough to cover a large portion of their mortgage if they chose.

Beyond mortgages, IUL can act as a retirement‑income supplement. Once the cash value is large enough to cover the COI, you can start taking tax‑free loans. Those loans can replace part of your 401(k) withdrawals, which might lower your taxable income in retirement.

The policy also offers a no‑required‑minimum‑distribution (RMD) feature, unlike traditional retirement accounts. That means you can let the cash grow as long as you want, then tap it when you need it.

To make the most of this strategy, follow these steps:

- Set a death benefit that covers the full mortgage balance plus a buffer.

- Front‑load premiums for the first 5‑7 years to build cash quickly.

- Monitor the illustration yearly; adjust premiums if the cash value drifts low.

- Plan loan repayments so the cash value stays healthy.

Allianz Life notes that the cash value can be accessed without penalty before age 59½, as long as the policy stays in force. Allianz explains the retirement‑planning angle.

Bottom line:With an IUL you get a death benefit that can erase a mortgage and a cash bucket you can tap for retirement.

IUL vs. Other Life Insurance: Term, Whole Life, and Variable Life

When families shop for protection, they usually compare term, whole, and universal options. Here’s howindexed universal life insurance benefits for familiesstack up.

| Feature | IUL | Term | Whole Life | Variable Life |

|---|---|---|---|---|

| Premium Flexibility | Adjustable within limits | Fixed for term length | Fixed whole‑life premium | Adjustable but tied to investment performance |

| Cash Value | Index‑linked, tax‑deferred | None | Guaranteed growth | Market‑linked, risk of loss |

| Downside Protection | 0% floor protects cash | None | Guaranteed cash | No floor – can lose value |

| Growth Potential | Cap‑limited upside | None | Modest guaranteed | Full market upside |

| Living Benefits | Accelerated death, LTC riders | None | Limited (optional riders) | Often available but costly |

Term life is cheap and pure protection. It works well for a specific need, like a 20‑year mortgage, but it ends when the term ends. Whole life gives a guaranteed cash value, but growth is slower and premiums are higher.

Variable universal life (VUL) lets you invest the cash value in mutual‑fund‑like sub‑accounts. You can capture the full market upside, but you also bear the full downside. That makes VUL riskier for families who need stability.

IUL sits in the middle. You get more upside than whole life because the index can credit higher rates, but you have a floor that stops losses. The trade‑off is the cap and participation rate, which limit the max credit each year.

According to Western & Southern, the cap typically sits between 8%‑12% and participation rates range from 50%‑100%. Those numbers shape how fast the cash value grows.

When you weigh the options, ask yourself these questions:

- Do you need a permanent death benefit?

- Is tax‑deferred cash growth important?

- Can you tolerate caps on upside?

- Do you want the ability to borrow against cash value?

Bottom line:IUL offers families flexibility and cash value that term can’t, while keeping risk lower than VUL.

Is IUL Right for Your Family? Key Considerations

Not every household will benefit from an IUL. Here are the key factors to weigh.

Income stabilitymatters. Premiums can be adjusted, but you still need enough cash value to cover the cost of insurance (COI). If your income fluctuates wildly, you might struggle to keep the policy in force.

Age and horizonare also big. IUL shines when you have at least 15‑20 years before retirement, giving the cash value time to grow past the early‑year fees.

High‑earning families who have maxed out 401(k) and IRA contributions often use IUL as a supplemental tax‑advantaged bucket. The policy’s high contribution limits let you shelter extra cash.

On the flip side, families on a tight budget may find the caps and fees erode the early cash value. In that case, a term policy for pure protection plus a separate investment account might be cheaper.

Here’s a quick checklist you can run through with your agent:

- Do you have a need for permanent protection (e.g., mortgage, legacy)?

- Can you afford a minimum premium that covers COI for the next 5‑10 years?

- Do you understand the policy’s cap, participation rate, and floor?

- Have you reviewed the rider costs (chronic illness, LTC, etc.)?

- Is the insurer’s financial strength solid? Look for A‑M ratings.

Life Care Benefit Services can help you run these numbers and match you with a carrier that offers transparent caps and low fees.

Remember that an IUL is a long‑term commitment. If you need to surrender early, you may face surrender charges that eat into cash value.

Bottom line:Evaluate income stability, age, and cash‑value goals before choosing an IUL.

Frequently Asked Questions About Indexed Universal Life Insurance

What is the main purpose of an indexed universal life insurance policy?

An IUL gives you a permanent death benefit while letting a portion of your premiums grow in a cash‑value account linked to a market index. The cash grows tax‑deferred, can be borrowed tax‑free, and the policy includes living‑benefit riders for illness or long‑term care. Families use it for protection, mortgage payoff, and a supplemental retirement bucket.

How does the cash value grow if it’s not actually invested in the stock market?

The insurer uses options or other financial instruments to credit interest based on the index’s performance. If the index goes up, you earn a percentage (the participation rate) up to a cap. If the index falls, a floor, usually 0%, keeps the cash value from dropping. This method gives upside potential without market loss risk.

Can I change my premium payments after the policy starts?

Yes. IUL policies are designed with flexible premiums. You can increase payments to boost cash value or reduce them (as long as the cash value can cover the cost of insurance). This flexibility is handy for families whose income may rise or dip over time.

What are the tax benefits of an IUL compared to a traditional retirement account?

The cash value grows inside a life‑insurance wrapper, so you don’t pay income tax on the gains each year. Policy loans are generally tax‑free, and the death benefit passes to beneficiaries income‑tax‑free. This triple‑tax advantage makes IUL a powerful tool for families looking to supplement retirement income.

What living‑benefit riders are available, and how do they work?

Common riders include accelerated death benefits for chronic or terminal illness, a long‑term‑care (LTC) rider that pays a monthly indemnity, and a disability rider that lets you access a portion of the death benefit early. When a qualifying event occurs, you file a claim with the insurer, and the rider pays out either as a lump sum or installments, usually tax‑free.

How does an IUL help with mortgage protection?

The death benefit can be set high enough to cover the entire mortgage balance. If a spouse passes away, the benefit pays off the loan in full. Meanwhile, the cash value can be borrowed to make extra mortgage payments, potentially shaving years off the loan term.

Is an IUL suitable for a small business owner?

Yes. Business owners often need flexible premium schedules and may use the cash value as collateral for a key‑person buy‑sell agreement. The policy can also provide a supplemental retirement reserve that isn’t tied to market volatility.

What should I watch out for when choosing an IUL?

Pay close attention to the cap, participation rate, and policy fees. High caps and participation rates boost growth, but fees can eat returns in the early years. Also, ensure the insurer has strong financial ratings and that the policy includes the riders you need.

Conclusion: Secure Your Family’s Future with IUL

Indexed universal life insurance brings together a lifelong death benefit, tax‑free cash growth, and living‑benefit options that can cover medical costs, mortgage balances, or retirement shortfalls. When you work with a trusted agency like Life Care Benefit Services, you get personalized guidance to match a policy’s cap, participation rate, and rider suite to your family’s unique goals.

Start by gathering quotes, reviewing the illustrations, and asking about premium flexibility and rider costs. Use the checklist we provided to compare term, whole, and variable options. If you have stable income, a long‑term horizon, and a desire for tax‑advantaged growth, an IUL can be a smart addition to your financial plan.

Ready to protect your loved ones and build a tax‑free cash reserve? Schedule a free consultation with Life Care Benefit Services today and see how an IUL can fit into your family’s roadmap.

Bottom line:IUL offers families lasting protection, cash growth, and flexible benefits that traditional policies can’t match.