How to Choose Indexed Universal Life Insurance for Retirement Planning

Most people think retirement is all about 401(k)s and IRAs. The truth is, many retirees miss out on a tool that can protect a family, grow tax‑deferred cash, and still pay a death benefit. That tool is an indexed universal life (IUL) policy. In this guide you’ll see how to choose indexed universal life insurance for retirement planning step by step. We’ll walk through the mechanics, match the policy to your goals, compare carriers, and show you how to lock in the right riders and costs. By the end you’ll have a clear roadmap to pick a policy that fits your life and your future.

Step 1: Understand How Indexed Universal Life Insurance Works

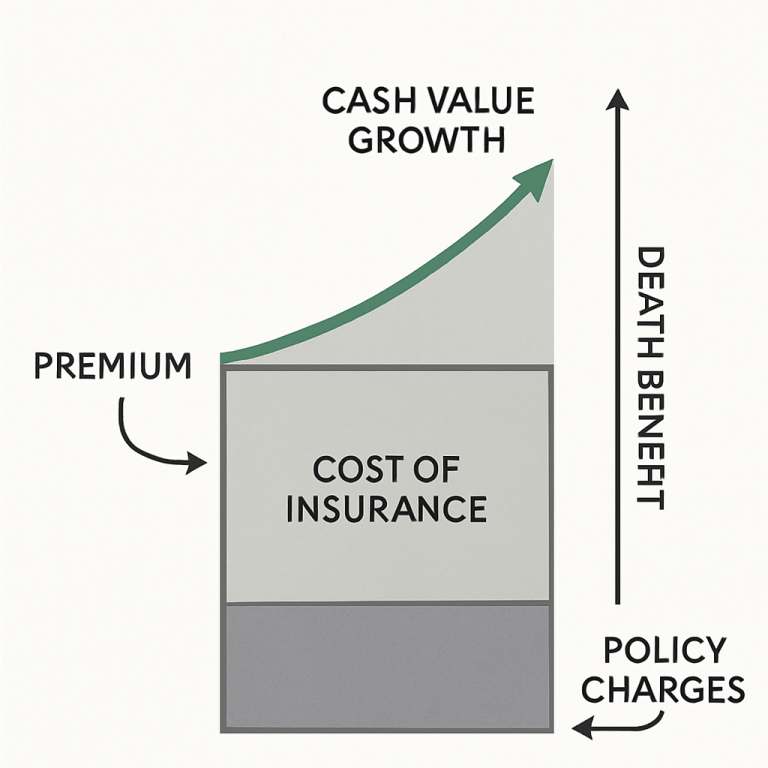

Indexed universal life is a permanent life insurance policy that also builds cash value. The cash value grows based on a stock market index, but you never own the index directly. The insurer uses options to credit interest. If the index climbs, you get a capped credit; if it falls, a floor (often 0%) protects you.

Every premium you pay splits into two buckets. One covers the cost of insurance, fees, and the death benefit. The rest goes into the cash‑value account. Over time the cash value can be used for loans, withdrawals, or to pay future premiums.

Caps limit the upside. For example, a 12% cap means that even if the S&P 500 returns 15%, you only see 12% credited. Floors keep the cash value from dropping when the market is down.

The policy stays alive as long as the cash value can cover the cost‑of‑insurance (COI) charges. If the cash value falls short, you must add extra premium or the policy will lapse.

Tax treatment is a big draw. The cash value grows tax‑deferred, and policy loans are generally tax‑free as long as the policy stays in force. However, if the policy becomes a Modified Endowment Contract (MEC), withdrawals may be taxed.

Because the policy is more complex than term life, you’ll want to review the illustration with an advisor each year. Look for the crediting method, the cap, the floor, and any participation rate.

According to Western Southern, most IULs use a 0% floor and a cap that can change each year. That flexibility is a strength, but it also means you need to stay on top of the numbers.

Bottom line:Know the cap, floor, and premium split, then watch the cash value each year.

Step 2: Assess Your Retirement Goals and Risk Tolerance

Before you shop, write down three concrete retirement goals. Maybe you want to replace 30% of your expected Social Security, pay off a mortgage, and leave a legacy for grandchildren.

Next, rank those goals by importance. The highest priority will drive the amount of death benefit you need and how much cash value you want to build.

Now think about risk. IULs let you choose an index and a participation rate. If you’re comfortable with a 100% participation rate, you’ll capture more upside but may pay a higher premium. If you prefer a lower participation rate with a solid floor, you’ll sacrifice some growth for stability.

Here’s a quick worksheet you can print:

- Goal #1 , Amount needed , Time horizon

- Goal #2 , Amount needed , Time horizon

- Goal #3 , Amount needed , Time horizon

Plug those numbers into a basic cash‑flow model. See how much you can afford to fund each year without hurting your current budget.

And remember: the longer your horizon, the more you can let the cash value compound. A 30‑year horizon can smooth out years when the cap is low.

After you’ve set goals and risk comfort, you’ll have a clearer picture of the premium range that makes sense. That range becomes the baseline when you start comparing carriers.

Use the worksheet to ask yourself: if I need $10,000 extra cash each year for retirement, can my IUL premium cover that and still leave room for COI?

Bottom line:Clear goals and a realistic risk profile set the stage for smart IUL selection.

Step 3: Compare Top IUL Carriers and Policy Features

Now it’s time to line up the carriers. The market offers a mix of legacy insurers and newer digital platforms. Your job is to match the carrier’s strengths to the goals you set in Step 2.

Here are four carriers that consistently appear in independent rankings:

| Carrier | Best For | Key Features | Typical Cap Range |

|---|---|---|---|

| Amplify | Digital experience | AI‑driven illustration, real‑time dashboard | 8‑12% |

| Fidelity & Guaranty Life | Retirement income | Low‑cost loans, broad index choices | 9‑11% |

| Lincoln Financial | Estate planning | No‑lapse guarantees up to age 121 | 7‑10% |

| Nationwide | Long‑term care riders | Strong chronic‑illness rider options | 8‑11% |

When you compare, look beyond the headline cap. The research shows the highest advertised cap (12.25% from Allianz) isn’t the top retirement pick. Flexibility and transparent net returns matter more.

Check each carrier’s financial strength rating. A‑rated carriers such as Pacific Life and National Life Group have the ability to pay claims decades from now.

Also note participation rates. Some carriers lock in 100% participation, meaning you get the full index gain up to the cap. Others sit at 80% and charge lower premiums.

Read the policy illustration carefully. It should show the cost‑of‑insurance (COI) path, the cap and floor assumptions, and any rider costs.

According to Amplify’s guide, the best IULs combine easy onboarding, multiple index options, and living‑benefit riders. That combination aligns with the data that retirees value flexibility first.

Bottom line:Matching carrier strengths to your goals beats chasing the highest cap.

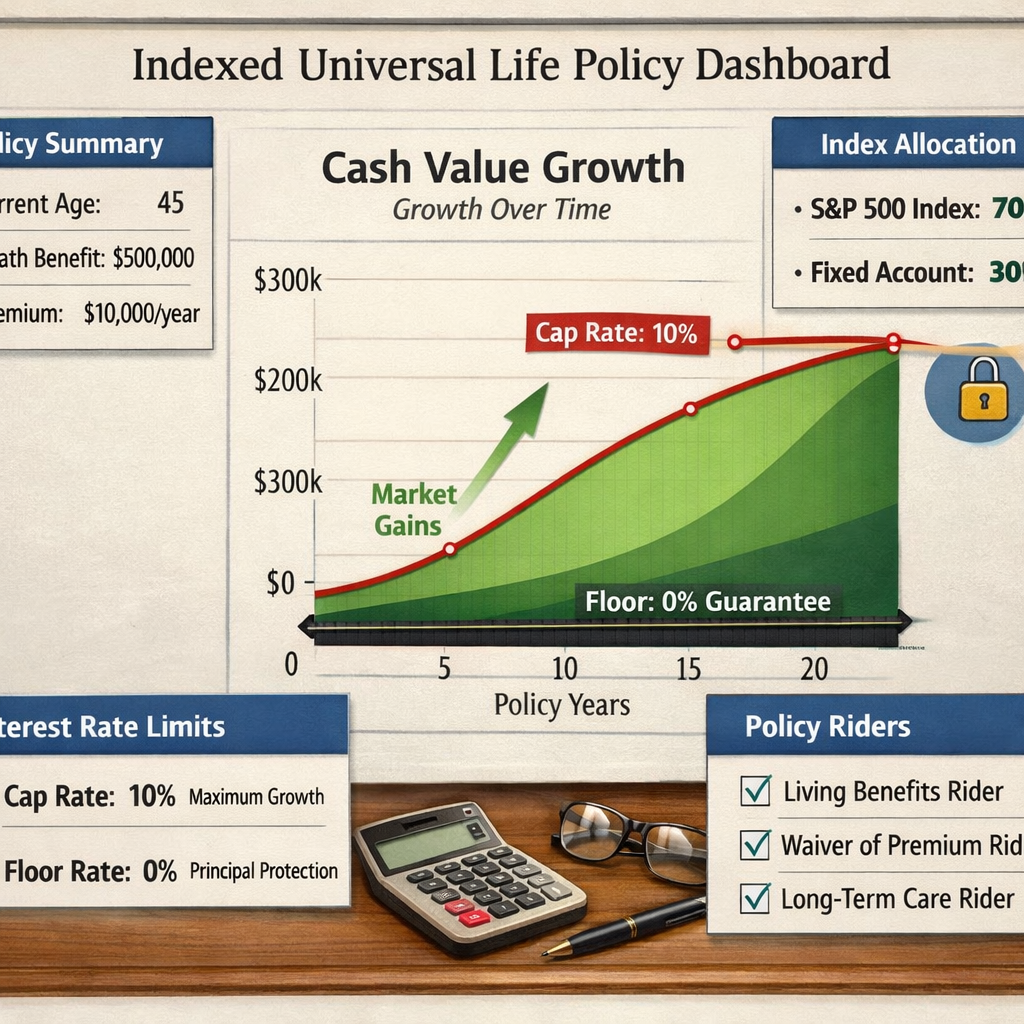

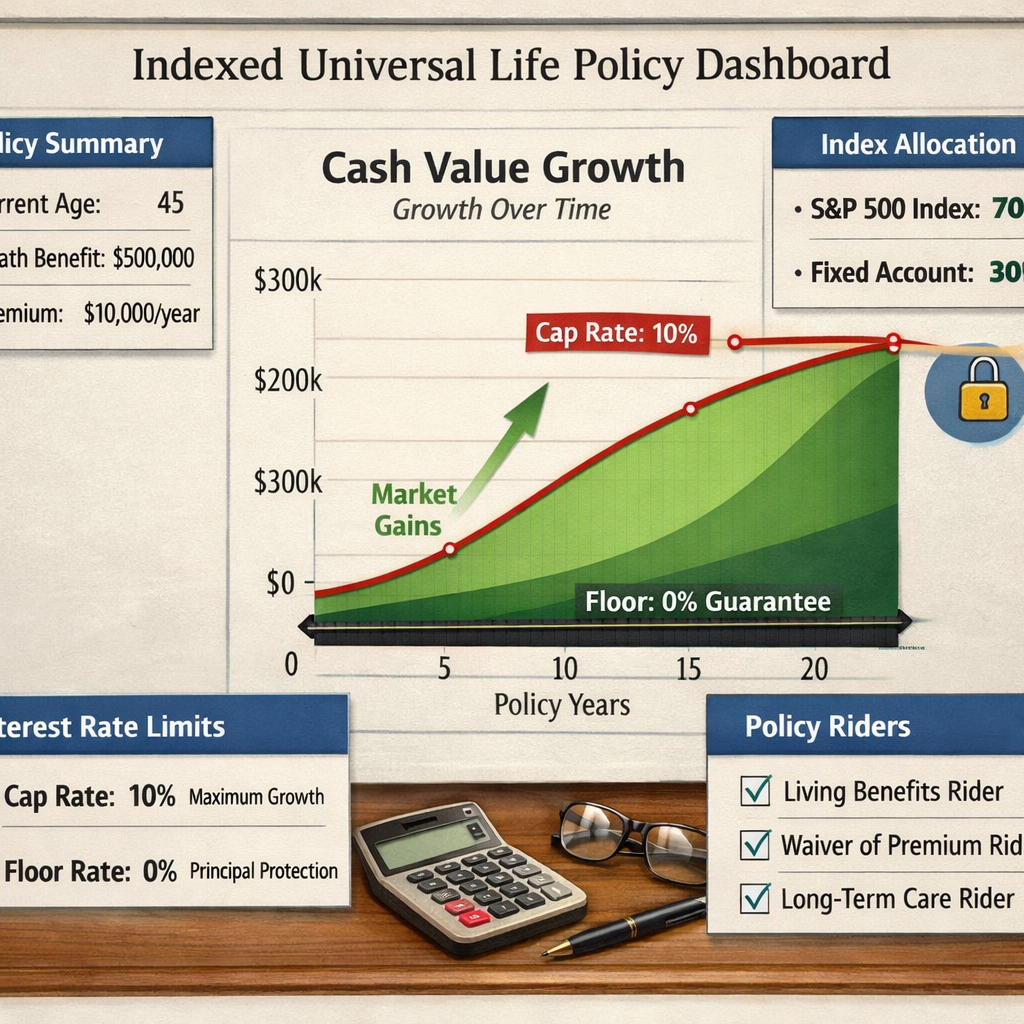

Step 4: Prioritize Living Benefits and Riders

Living‑benefit riders turn a death‑only policy into a tool you can use while you’re alive. Common riders include accelerated death benefit, chronic‑illness, and long‑term‑care add‑ons.

Ask yourself which scenarios you want covered. If you worry about a chronic condition that could limit your ability to work, a chronic‑illness rider that pays a portion of the death benefit early can keep cash flowing.

Another popular rider is the disability waiver of premium. If you become disabled, the insurer waives future premium payments while the cash value keeps the policy alive.

Each rider adds a cost, usually a small percent of the face amount. For example, a chronic‑illness rider might add $600‑$800 per year on a $500,000 policy.

When you add riders, recalculate the projected cash value. Some riders reduce the amount that can be borrowed later because they lower the death benefit base.

Below is a quick matrix to help you decide which riders matter most:

| Rider | When It Helps | Typical Cost |

|---|---|---|

| Accelerated Death Benefit | Serious illness diagnosis | 1‑2% of face |

| Chronic‑Illness | Long‑term care needs | $600‑$800 per year |

| Disability Waiver | Loss of earning ability | 0.5‑1% of face |

| Guaranteed Minimum Interest | Desire for floor >0% | Varies by carrier |

Make sure the rider’s trigger events match your health concerns. If you have a family history of heart disease, a chronic‑illness rider may be essential.

Remember that some carriers bundle riders at no extra charge, while others treat each as an add‑on. Get the cost breakdown in writing.

“The best time to start building cash value was yesterday,” says many seasoned advisors.

Bottom line:Riders add protection, but they also raise the cost; pick only those you truly need.

Step 5: Analyze Policy Costs and Projected Returns

Costs in an IUL fall into several buckets: premium load, administration fees, cost of insurance (COI), surrender charges, and rider fees.

Premium load is taken off each premium before any cash value is credited. It usually sits between 5% and 10% of the premium.

Administration fees are a flat monthly amount, often $5‑$15. COI rises with age and the size of the death benefit. In the early years COI is low, but by age 60 it can become a sizable chunk of the cash value.

Surrender charges apply if you cancel the policy in the first 10‑15 years. They taper down each year and disappear after the surrender period.

When you run an illustration, focus on the net cash‑value growth after subtracting all fees. A common benchmark is a net 3%‑4% after fees for a conservative policy.

Here’s a simple step‑by‑step way to test a quote:

- Take the projected cash value after Year 10.

- Subtract the total of COI, admin fees, and rider costs for each year.

- Divide the result by the total premiums paid to get a net return.

- Compare that net return to a low‑risk investment benchmark like a high‑yield savings account.

If the net return is lower than what you could earn elsewhere, the policy may not be worth the protection.

One real‑world example: a 35‑year‑old male funded a $500,000 IUL with a $10,000 annual premium. After ten years, the illustration showed $150,000 cash value, but $30,000 had been eaten by COI and fees, leaving a net 3.5% annual growth. That matched the client’s retirement cash‑flow goal.

Bottom line:A policy that nets 3%‑4% after fees can be a solid retirement supplement.

Step 6: Consult a Professional and Request a Personalized Quote

The IUL landscape is full of fine print. An independent advisor can pull illustrations from multiple carriers, explain rider trade‑offs, and run “what‑if” scenarios tailored to your budget.

When you meet with an advisor, bring your goal worksheet, your current budget, and any health information that might affect underwriting.

Ask for a side‑by‑side quote that shows the premium, COI path, cap, floor, and rider costs. Review the illustration line by line. If something looks vague, demand clarification.

Life Care Benefit Services works with more than 50 top‑rated carriers and can match you with a policy that fits your retirement plan. Their experts can also help you file the necessary medical paperwork and explain the tax implications.

Schedule a call today to get a personalized illustration. Use the internal link below to jump straight to their IUL guide.

Best IUL for Retirement Planning 2026 guide

Bottom line:Professional advice ensures you pick the right policy and avoid costly mistakes.

Frequently Asked Questions

What is the main advantage of an IUL over a traditional whole life policy?

An IUL lets you earn interest linked to a market index while protecting the cash value from downside losses. This can produce higher growth than the fixed interest of whole life, yet you still keep a death benefit. The flexibility to adjust premiums also helps fit changing cash‑flow needs, making it a useful tool for retirement planning.

Can I change the index my IUL is tied to after the policy is issued?

Most carriers allow one index switch per year without resetting the cash value. You’ll pay a small switch fee, but the ability to move to a more stable index can improve returns if market conditions shift. Check the policy illustration for the exact switch rules.

How do living‑benefit riders affect my cash‑value growth?

Riders add a cost that reduces the net cash value each year. However, they also provide a safety net that can pay out early if you face a chronic illness or disability. The trade‑off is worth it if the rider protects a risk that would otherwise force you to dip into retirement savings.

What happens if the policy’s cash value can’t cover the COI?

When cash value drops below the COI, you must either pay extra premium or the policy will lapse. Some policies include a no‑lapse guarantee that lets the death benefit stay in force as long as you keep up with a minimum premium.

Is the cash value in an IUL accessible before retirement?

Yes. You can take loans or withdrawals up to the cash‑value amount. Loans are tax‑free but accrue interest, and unpaid loans reduce the death benefit. Withdrawals up to your cost basis are also tax‑free, but any amount above that may be taxed as income.

How do I know if the cap rate is realistic?

Compare the cap to historic index returns. A cap of 8%‑12% is typical. If the cap is far above the long‑term average return of the index, the insurer may reduce it later. Look for a cap that balances upside potential with an affordable premium.

Do I need a medical exam to get an IUL?

Most carriers require a brief medical exam, especially for higher face amounts. Some digital platforms offer simplified issue options for smaller policies, but the exam helps lock in lower COI rates.

Can I convert a term policy to an IUL later?

Many insurers offer a conversion privilege that lets you switch from term to a permanent policy like an IUL without a new medical exam, as long as you do it within the conversion window (often 10‑12 years). This can be a handy way to add cash value later in life.

Conclusion

Choosing indexed universal life insurance for retirement planning isn’t about chasing the highest cap. It’s about matching a flexible, tax‑advantaged policy to your personal goals, risk comfort, and budget. By understanding how the policy works, assessing your retirement needs, comparing carriers, picking the right riders, and crunching the cost numbers, you can build a retirement supplement that also protects your loved ones.

Remember to involve a trusted advisor, someone who can pull side‑by‑side quotes, run realistic what‑if scenarios, and keep the policy on track as you age. With the right IUL in place, you’ll have a lifelong safety net and a cash‑value engine that can help fund your retirement dreams.

Ready to start? Contact Life Care Benefit Services today for a free, no‑obligation illustration and take the first step toward a secure retirement.