Families need a plan that protects them now and pays off later. Many think a life policy is just a death payout, but an Indexed Universal Life (IUL) can also grow cash for retirement. In this guide you’ll see how to size the need, learn the mechanics, add living benefits, compare it to a 401(k) or IRA, and pick the right policy for your household.

By the end you’ll have a clear checklist, real‑world tips, and a path to a tax‑free retirement bucket that also shields your loved ones.

Step 1: Assess Your Family’s Retirement Needs and Financial Goals

Start with a picture of where you want to be at retirement. Write down the income you think you’ll need to cover housing, health, school, and fun. A good rule of thumb is to aim for 70‑80% of your current household spending. Include any debts you want gone, like a mortgage, and future costs such as college tuition.

Next, gather the numbers you already have. Pull your latest 401(k) or IRA statements, list any pension or Social Security estimates, and note the balances of savings accounts. This snapshot shows the gap between what you have and what you’ll need.

Ask yourself these questions:

- What age do you plan to retire?

- How many years do you expect to draw income?

- Do you want a death benefit that can cover a mortgage if you pass early?

- How much flexible cash do you want to tap before retirement?

Write the answers in a simple table. Seeing the gap in black and white helps you decide how much extra you must save each year.

When you have the gap, you can decide whether an IUL can fill part of it. The policy’s cash value grows tax‑deferred, and you can borrow against it later without a penalty. That can be a useful bridge if your other accounts fall short.

Remember to factor in inflation. A $500,000 need today may be $800,000 in 20 years. Use an inflation calculator to adjust your target.

Bottom line:Know your retirement cash gap before you look at any product.

Step 2: Understand How Indexed Universal Life Insurance Works

An IUL is a permanent life policy that mixes a death benefit with a cash‑value account. Part of each premium pays for the insurance cost, and the rest goes into a cash bucket that earns interest linked to a market index, like the S&P 500.

The cash value is not directly invested in the stock market. The insurer uses options or other instruments to credit interest based on how the index moves. If the index goes up 10%, the policy might credit 7% after a participation rate and a cap are applied. If the index falls, a floor (often 0%) stops the cash value from losing money.

Key pieces to watch:

- Cap rate:The maximum interest you can earn in a period.

- Participation rate:The percentage of the index gain that is credited.

- Floor:The minimum credited interest, usually 0%.

- Cost of insurance (COI):A fee that rises with age.

Because caps and participation rates can change, the policy’s growth is not guaranteed. That’s why you need to read the illustration carefully.

Flexibility is a big plus. You can raise or lower premiums within limits, letting you match payments to a good‑income year or a lean year. However, you must keep enough cash value to cover the COI, or the policy will lapse.

Tax treatment is another benefit. The cash grows tax‑deferred, and policy loans are generally tax‑free as long as the policy stays in force. The death benefit is paid income‑tax free to beneficiaries.

For a plain definition, see Wikipedia’s Indexed Universal Life entry. It breaks down the crediting method in simple terms.

Bottom line:Understand caps, participation rates, and floors before you trust the growth numbers.

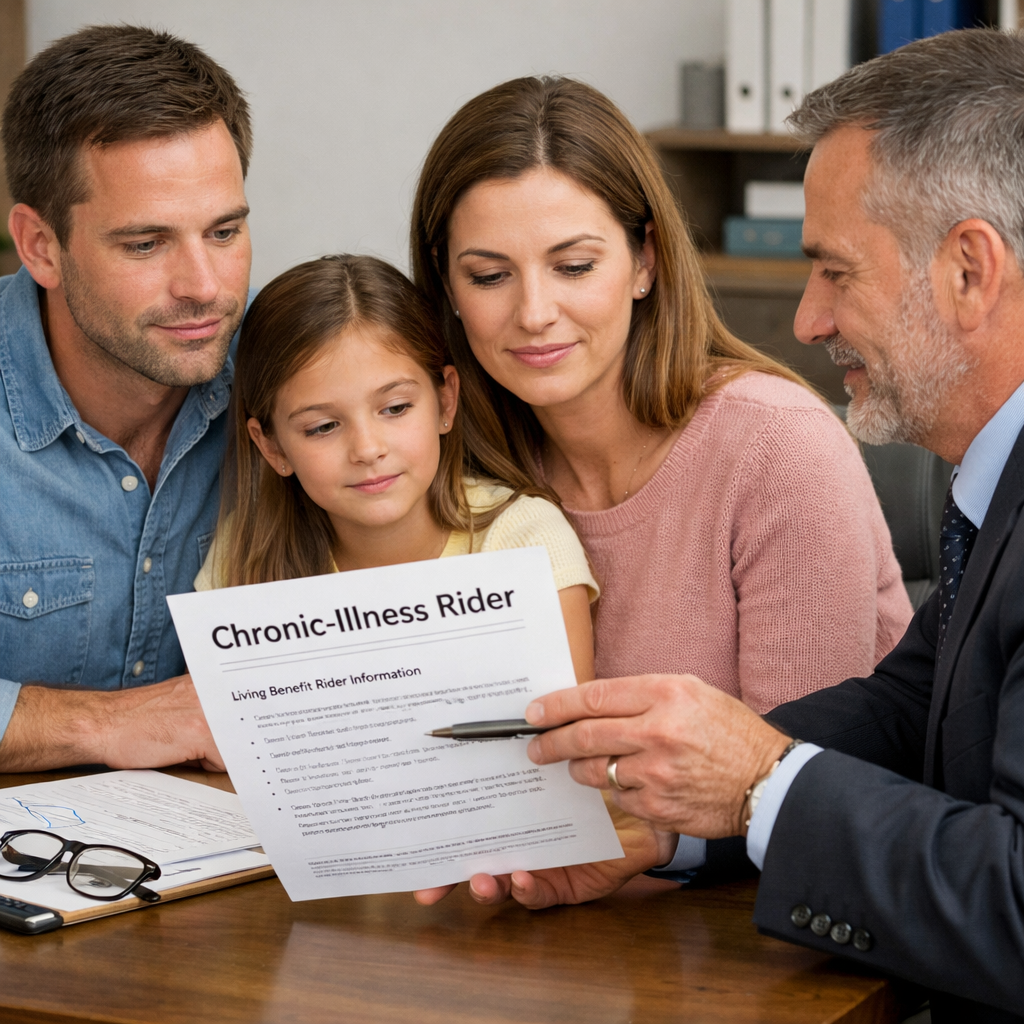

Step 3: Use Living Benefits for Family Protection

Living benefits are riders that let you use part of the death benefit while you’re still alive. Common riders cover chronic illness, critical illness, or long‑term care. When a qualifying event happens, the insurer pays a percentage of the death benefit early, usually tax‑free.

Imagine your child needs a costly surgery, or you face a disability that stops work. A chronic‑illness rider could give you a lump sum that fills the gap without touching your savings.

These riders cost extra, often $10‑$20 a month, but they add a safety net that many families find priceless. The Transamerica chronic‑illness guide shows how a 20% rider on a $500,000 policy could release $100,000 when you qualify.

“Living benefits turn a life policy into a financial safety net you can tap before the end of life.”

When you add a rider, check the trigger events. Some policies require a doctor’s statement and proof of expenses. Keep that paperwork ready so you can file quickly.

Remember the cash value must stay above the COI. If you take a living‑benefit payout, the cash value drops, so you may need to add a premium to keep the policy alive.

Bottom line:Living benefits give you tax‑free cash when life throws a curveball, but they cost a bit and lower cash value.

Step 4: Compare IUL with Traditional Retirement Accounts

A 401(k) lets you defer taxes on contributions and grow money in mutual funds or ETFs. You must take required minimum distributions (RMDs) after age 73, and withdrawals before 59½ may incur a 10% penalty.

An IUL also grows tax‑deferred, but you can borrow against the cash value at any age without a penalty. The loan isn’t taxed as income as long as the policy stays in force.

Here are some side‑by‑side points:

Caps can limit upside, but they also protect you from market crashes. A 401(k) can lose value in a downturn, while an IUL’s floor keeps the cash value from dropping below zero.

Another difference is contribution limits. In 2026 you can put up to $7,500 (plus catch‑up) in a Roth IRA, but an IUL has no annual limit. You can front‑load premiums to build cash faster.

For official RMD rules, see the Social Security Administration’s retirement FAQ. It explains the age and calculation method.

Bottom line:401(k)s give market growth with no caps, while IULs trade some upside for tax‑free loans and a death benefit.

Step 5: Choose the Right IUL Policy and Provider

Not every IUL fits a family’s budget. Look for a carrier that discloses caps and participation rates. Our market data shows only 40% of policies share a cash‑value cap, and just 13% reveal a participation rate. That lack of transparency can hide risk.

Life Care Benefit Services is the only provider in the data set that markets directly to families, seniors, and small‑business owners. Their policies include chronic‑illness and long‑term‑care riders, which many others omit.

When you meet an agent, ask these questions:

- What is the current cap and participation rate?

- Which riders are available and how much do they cost?

- Can I see a side‑by‑side illustration comparing a 0% index year and a strong year?

- How does the cost‑of‑insurance schedule change after age 60?

- Is there a surrender charge if I need to end the policy early?

Request a written illustration that shows the cash value after 10, 20, and 30 years with a realistic cap (e.g., 8‑12%). Compare that to your projected 401(k) balance.

Once you pick a carrier, set a baseline premium that covers the COI plus a small cash‑value buffer. In high‑income years, add extra premium to boost cash value faster. In lean years, let the cash value pay the COI.

Finally, lock in the chosen policy with a signed application and a medical exam if required. Keep a copy of the rider schedule and set a calendar reminder to review the policy each year.

For more detail on picking the right IUL, see Best IUL for Retirement Planning 2026: Complete Guide. It walks through the exact steps we just covered.

Bottom line:Pick a transparent provider, verify caps and riders, and plan premium payments to keep the policy alive.

Frequently Asked Questions

What is the main advantage of an IUL over a traditional 401(k)?

An IUL gives you a death benefit that your family receives tax‑free, plus a cash‑value bucket you can borrow from at any age without a 10% early‑withdrawal penalty. A 401(k) offers higher market upside but has required minimum distributions and no death benefit. For families who want both protection and a flexible retirement bucket, the IUL’s loan feature can be a big win.

How do caps and participation rates affect my cash growth?

Caps set the highest interest you can earn in a year, while participation rates decide what slice of the index gain is credited. For example, with an 8% cap and a 70% participation rate, a 12% index gain would credit only 5.6% (12% × 0.70, limited to 8%). Knowing these numbers helps you set realistic expectations for cash‑value growth.

Can I add a living‑benefit rider after the policy is in force?

Yes, many carriers let you add riders later, but the cost may be higher than if you add them at start‑up. Adding a chronic‑illness rider early can lock in a lower monthly charge and ensure coverage when you need it most.

What happens if my cash value drops below the cost of insurance?

If the cash value can’t cover the COI, the policy will lapse unless you increase premiums or take a loan to keep it alive. That’s why it’s important to monitor the cash‑value‑to‑COI ratio at least twice a year and adjust payments accordingly.

Do I still need a separate emergency fund if I have an IUL?

An IUL is not a substitute for an emergency fund. The cash value is tied up in the policy and may have loan interest or affect the death benefit. Keep three to six months of living expenses in a liquid account, and view the IUL as a long‑term supplement.

Is an IUL suitable for a single‑parent household?

Yes, especially if you need a death benefit to cover a mortgage and a flexible cash source for unexpected expenses. Choose a flexible premium structure so you can lower payments during lean months, and consider adding a chronic‑illness rider for added protection.

Conclusion

Putting an IUL into your retirement plan can give your family a safety net that a 401(k) or IRA can’t match. You get a tax‑free death benefit, a cash bucket that grows with market indexes, and the option to pull money out early with living‑benefit riders. The key is to start with a clear picture of your retirement cash gap, understand how caps and participation rates work, and pick a transparent provider that serves families.

Life Care Benefit Services offers a family‑focused IUL with clear caps, rider options, and flexible premiums. Use the checklist we laid out, ask the right questions, and review the policy each year. When you do, you’ll have a retirement engine that protects your loved ones, supplies tax‑free cash when you need it, and adapts as your life changes.

If you’re ready to explore a policy, schedule a free consultation with a licensed advisor today. A solid IUL plan can turn today’s premiums into tomorrow’s peace of mind.