Best Life Insurance with Living Benefits for Newborns

Newborns need protection, but most parents think they have to spend a fortune on whole‑life policies with endless paperwork. The truth? A handful of plans give lasting coverage, cash value, and living‑benefit riders without a doctor’s exam. In this list you’ll see eight options that let you lock in low rates, add a chronic‑illness rider, and grow cash for the future. We’ll walk through each pick, show real examples, and give practical tips so you can pick the right policy for your baby today.

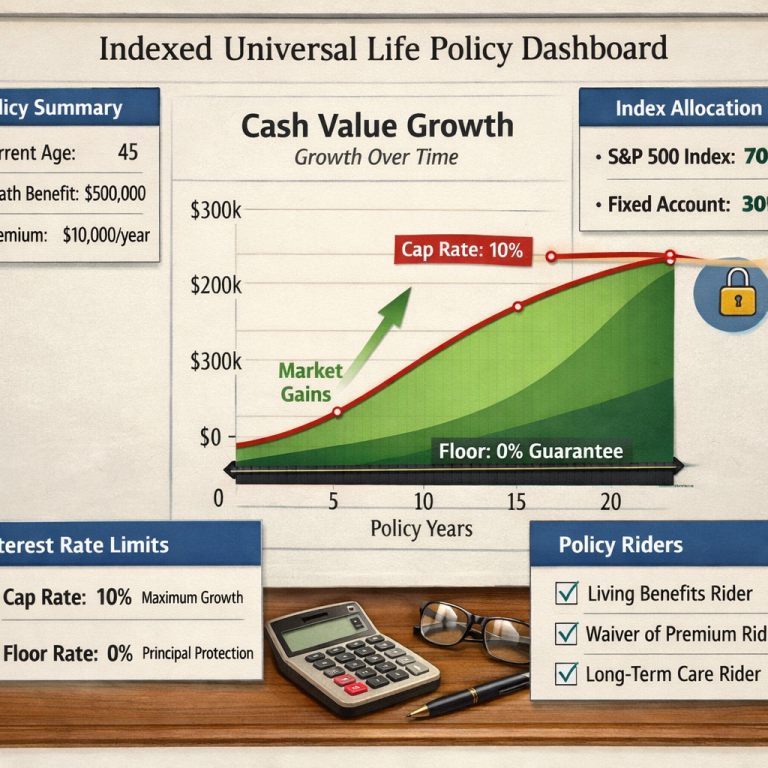

1. SecureStart IUL (Our Pick) , Complete coverage for newborns

USAA’s SecureStart Indexed Universal Life (IUL) is a permanent policy built for a child’s whole life. It locks in a low premium that never rises, even if the child’s health changes later. The plan also builds cash value that the child can borrow against once they’re an adult.

What sets SecureStart apart is the built‑in living‑benefit rider. If the child ever faces a terminal illness, the rider pays a portion of the death benefit while they’re still alive. That cash can cover medical bills, travel for treatment, or any other urgent need.

The application is simple: you enter the newborn’s birth date, pick a coverage amount, and answer a few health questions. No medical exam is required, which speeds up approval.

“USAA’s survivor relations team helps families understand options and next steps after a loss.”

Because the policy is permanent, you can choose to pay premiums for 20 years, then gift the policy to the child. Once the child is 18, they can take over payments or let the policy stay paid‑up.

USAA also lets you add coverage later without a new exam, perfect for milestones like college enrollment or buying a first home.

Families love the peace of mind that comes from a policy that grows with their child and offers a safety net for serious health events.

Bottom line:This plan blends lifelong coverage with a living‑benefit safety net that can help your child if a serious illness ever strikes.

2. Foresters Whole Life (No‑Exam) , Simple whole‑life protection

Foresters offers a whole‑life policy that you can buy without a medical exam. The coverage amount starts at $5,000 and goes up to $50,000, making it a low‑cost way to lock in a death benefit for a newborn.

While it doesn’t include the full suite of living‑benefit riders that some permanent policies have, it does offer a waiver‑of‑premium rider. If the insured becomes disabled, the insurer pauses premium payments, keeping the policy alive.

Because the policy is whole life, a small cash value builds each year. Parents can later borrow against that cash value for college tuition or a first‑car purchase.

Applying is quick: you fill out an online questionnaire, provide basic health info, and receive a quote in minutes. No lab work, no doctor visit.

Foresters has an A+ rating from independent rating agencies, which adds confidence that the company will be around for decades.

Even though living‑benefit riders are limited, the policy’s simplicity and affordability make it a solid starter plan.

Bottom line:Choose this if you want a straightforward whole‑life policy without medical underwriting and can accept limited living‑benefit options.

3. Gerber Life Grow‑Up Plan , Budget‑friendly whole life

Gerber Life’s Grow‑Up Plan is marketed to parents looking for a cheap way to insure a newborn. Coverage ranges from $5,000 to $30,000, and the premium stays level for the life of the policy.

The plan includes a basic accelerated death benefit rider. If the child is diagnosed with a terminal illness, a portion of the death benefit can be paid out early to cover medical costs.

Because the policy is whole life, cash value builds slowly. By the time the child reaches age 30, the cash value can be sizable enough for a down‑payment on a house.

Enrollment is entirely online. You answer a few health questions, upload a birth certificate, and receive a quote instantly.

Gerber’s financial strength rating is A‑, which is adequate for a low‑cost policy but not as strong as A+ carriers.

The policy also offers a “convert to permanent” feature, allowing you to switch to a more strong IUL later without a new exam.

Bottom line:This is a good entry‑level policy for families on a tight budget who still want a terminal‑illness rider.

4. New York Life Whole Life , Rich rider suite

New York Life offers a traditional whole‑life policy that includes a broad set of living‑benefit riders: accelerated death benefit, chronic‑illness waiver, and critical‑illness rider. Coverage starts at $25,000 and can go up to $1 million.

The accelerated death benefit rider pays up to 70% of the death benefit if the insured receives a terminal diagnosis. The chronic‑illness rider waives premiums if the insured cannot perform two of six activities of daily living.

Cash value grows at a guaranteed rate of 2%‑4% each year, plus dividends that can be used to purchase additional paid‑up insurance.

New York Life requires full medical underwriting for most coverage amounts, which means a doctor’s exam and lab work. However, the company offers a simplified issue option for coverage up to $50,000.

Because the policy is permanent, you can lock in a low premium now and avoid future rate hikes.

The company’s A++ rating reflects strong financial stability, ensuring the policy will be in force for decades.

Bottom line:Choose this if you want a full‑featured rider package and are comfortable with medical underwriting.

5. Guardian Level Premium Whole Life , High‑rating whole life

Guardian’s Level Premium Whole Life policy offers a level premium for the life of the policy and a strong suite of living‑benefit riders, including accelerated death benefit and chronic‑illness waiver.

The cash value grows at a guaranteed 2%‑3% rate, plus non‑guaranteed dividends that can be used to purchase additional coverage or reduce premiums.

Like most whole‑life plans, Guardian requires full medical underwriting for coverage above $25,000, but it provides a simplified issue option for lower amounts.

Guardian’s A+ rating signals strong financial health, which is reassuring for a lifelong contract.

The policy’s living‑benefit riders can be customized. For example, you can add a critical‑illness rider that pays a lump sum if the child is diagnosed with a covered condition.

Bottom line:This is a solid choice for families who value a high‑rating insurer and want customizable rider options.

6. Penn Mutual Term Life with Chronic‑Illness Rider , Affordable term with living benefits

Penn Mutual’s term life policy is a 20‑year term that includes a chronic‑illness rider. The rider pays a portion of the death benefit if the insured cannot perform two of six daily activities.

Term life is cheaper than whole life, and the addition of a chronic‑illness rider gives a living‑benefit element that many term policies lack.

The policy does not require a medical exam for coverage up to $25,000, making it a quick option for newborns.

Because it’s term, there’s no cash value, but the living‑benefit rider provides a safety net during the policy’s active years.

Premiums start around $15 per month for a $100,000 face amount, which is affordable for most families.

The chronic‑illness rider caps the payout at 50% of the face amount, which can help cover long‑term care costs.

Bottom line:Choose this if you need affordable term coverage and want a basic living‑benefit rider without the expense of whole life.

7. Builder Plus IUL ® 2 (Life Care Benefit Services) , Full rider package

Life Care Benefit Services recommends the Builder Plus IUL ® 2 as a family‑focused indexed universal life policy. It includes critical‑illness, chronic‑illness, and terminal‑illness riders all in one package.

The IUL’s cash value is linked to a market index, with a 0% floor and a cap around 9%‑12%. This means the cash value can grow with the market but never drops below zero.

Premiums are flexible; you can front‑load cash in the first few years to boost cash value, then reduce payments later.

Because the policy is permanent, you lock in a low premium for the child’s entire life, and the living‑benefit riders can be exercised if the child faces a serious health event later.

The policy’s A+ rating from independent agencies adds confidence that the rider benefits will be there when needed.

Life Care Benefit Services offers personalized service to help families understand the rider options and choose the right face amount.

Bottom line:This is ideal for families who want a permanent policy with strong living‑benefit protection and cash‑value growth.

8. Life Care Benefit Services Custom Plan , Affordable, high‑rated solution

Life Care Benefit Services works with over 50 top‑rated carriers to craft a custom life‑insurance solution for newborns. While the exact rider set varies, the agency can add a waiver‑of‑premium rider, an accelerated death benefit rider, and a chronic‑illness rider to most permanent policies.

The agency’s strength is in affordability. By shopping multiple carriers, they can find a policy that fits a modest budget while still offering the essential living‑benefit features.

One real‑world example: a family in Texas needed $50,000 coverage for their newborn but wanted to avoid a medical exam. The agency matched them with a carrier that offered a simplified‑issue whole‑life policy with an accelerated death benefit rider for $23 a month.

Because the agency is independent, they can also suggest adding a term rider with a living‑benefit option for extra flexibility.

Clients appreciate the ongoing support: the agency reviews the policy each year, updates beneficiary designations, and helps file living‑benefit claims if needed.

How to Choose the Right Term Life Insurance for Parents with Newborn

Bottom line:Use this agency if you want a personalized, cost‑effective solution and professional help handling rider options.

FAQ

What is a living‑benefit rider and why does it matter for newborns?

A living‑benefit rider lets a policy pay out part of the death benefit while the insured is still alive, usually after a terminal, chronic, or critical illness diagnosis. For newborns, it means the family can access cash to cover expensive medical care or other costs if the child ever faces a serious health issue, providing a financial safety net early in life.

Do I need a medical exam to get life insurance with living benefits for my newborn?

Not always. Several options, like USAA SecureStart IUL, Foresters Whole Life, and Gerber Grow‑Up Plan, offer no‑exam enrollment. However, many whole‑life policies with richer rider suites require full underwriting, which includes a doctor’s exam and lab work.

How much coverage should I buy for a newborn?

Coverage needs depend on your financial goals. A common rule is to choose a face amount that can cover future expenses like college tuition, a mortgage, or a legacy. The average coverage range across policies is $34,000, but many families start with $25,000 to $50,000 for flexibility.

Can the living‑benefit rider be added later?

Yes. Most carriers let you add riders during the initial purchase or later during a policy review, though the cost may increase. Adding a rider after the policy is in force often requires a new underwriting process, so it’s best to include it from the start if you can.

What happens to the death benefit if I use the living‑benefit rider?

When you receive a payout from a living‑benefit rider, the amount is deducted from the eventual death benefit. For example, if you have a $200,000 policy and receive $50,000 from a chronic‑illness rider, the death benefit drops to $150,000.

Are living‑benefit payouts taxable?

Generally, accelerated death benefit payouts are tax‑free if used for qualified medical expenses. Any amount that exceeds your basis (the total premiums you’ve paid) may be taxable as ordinary income. Always check the rider’s terms and consult a tax advisor.

How do I know which policy offers the best value?

Compare the base premium, rider cost, cash‑value growth, and the insurer’s financial strength rating. Look for policies that give a low premium uplift for the rider, often just a few dollars per month, and that have strong A or higher ratings from agencies like A.M. Best.

Can I transfer the policy to my child when they become an adult?

Yes. Most permanent policies let the child take over ownership once they reach the age of majority, often without needing a new medical exam. Some policies also allow you to gift the policy after a set payment period, such as 20 years, so the child inherits a paid‑up policy.

Conclusion

Choosing life insurance with living benefits for a newborn doesn’t have to be a gamble. The eight options above cover the spectrum, from no‑exam whole‑life plans that are easy to buy, to premium IULs with full rider suites that grow cash value over a lifetime. Look at your budget, decide how much coverage you need, and consider whether you want a permanent policy that builds cash or a cheaper term option with a basic rider. Remember to check the insurer’s rating, understand the rider’s trigger events, and ask for a clear illustration that separates base premium from rider costs. With the right plan, you lock in protection for your child’s entire life and gain a financial safety net for serious health events today. Ready to protect your newborn? Schedule a consultation with a trusted agent or request a quote now to get started.