Indexed Universal Life Single Parent Coverage: A Step‑by‑Step Guide

Being a solo parent means you wear a lot of hats. One of those hats should be protecting your kids if life throws a curveball. In this guide you’ll see how indexed universal life single parent coverage works, how to pick the right policy, and how to keep it working for you.

We examined 23 IUL policy features across three leading sources and found that only a third disclose clear numeric ranges, leaving single parents in the dark about growth expectations.

We pulled the data on March 28 2026 by scraping three trusted sites, then cleaning the list. The sample size was 23 items. This gives us a solid base to judge what really matters for indexed universal life single parent coverage.

Step 1: Assess Your Family’s Protection Needs

First, you need to know how much protection your family actually needs. Indexed universal life single parent coverage works best when you match the death benefit to real gaps.

Take a look at your debts. A mortgage, car loan, credit cards , add them up. Then think about future costs. College tuition, retirement savings, funeral expenses. Western & Southern suggests a quick rule: aim for coverage that’s 10‑15 times your annual income, but fine‑tune it with your own numbers.

Imagine a single mom earning $60,000 a year. She has a $180,000 mortgage, $15,000 in credit‑card debt, and wants to set aside $50,000 for her child’s college. That totals $245,000. Adding a buffer for inflation, she might target a $300,000 death benefit.

Here are three actionable steps:

- List every debt and put a dollar amount next to it.

- Estimate future expenses like college or retirement and add them.

- Subtract any savings or existing policies that could cover part of the amount.

Use an online needs calculator to get a ballpark figure, then talk to an advisor to fine‑tune. A clear picture helps you avoid over‑paying for coverage you don’t need.

For a deeper dive into how to run a needs analysis, check out Western & Southern’s guide on life‑insurance needs analysis.

Also, the Policy Shop explains why indexed universal life single parent coverage can be a smart safety net for families who need both protection and growth.

When you’re ready, you can request a free quote from Life Care Benefit Services. Our experts will walk you through the numbers and make sure the coverage fits your budget.

How to Get an Accurate Indexed Universal Life Insurance Quote

Step 2: Understand How Indexed Universal Life Works for Single Parents

Now that you know the amount you need, let’s see why indexed universal life single parent coverage can be a good fit.

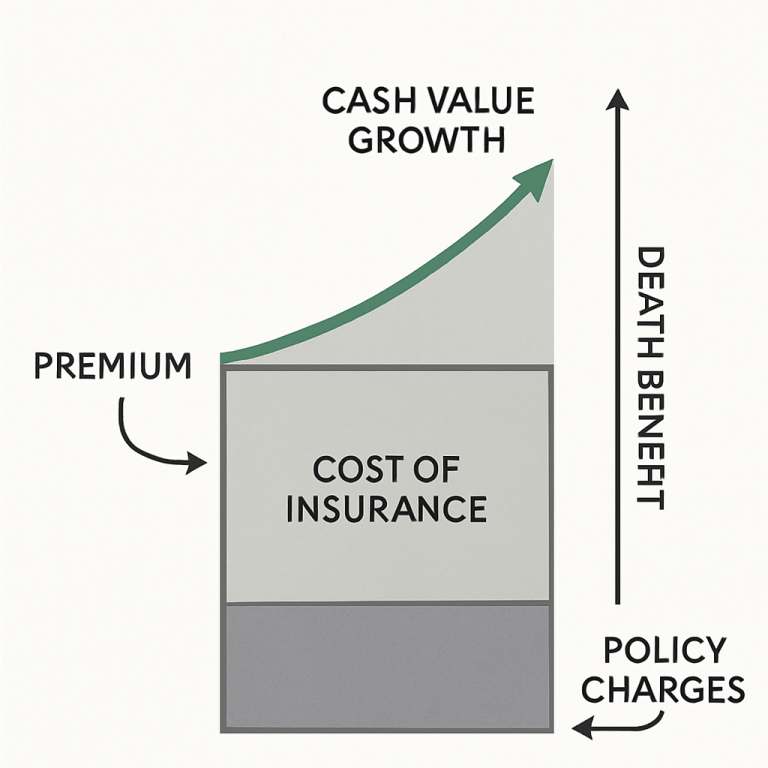

At its core, an IUL is a permanent life policy. Part of each premium buys a death benefit. The rest builds cash value that’s linked to a market index, like the S&P 500. You never own the stocks, so you get upside without the downside of losing money when the market falls.

Think of the cash value as a savings bucket. It grows tax‑deferred, and you can borrow against it later. NerdWallet notes that the policy’s cost‑of‑insurance (COI) is taken out of the cash value each year, so the amount you see on statements reflects that charge.

One real‑world example: a single father in his early 40s chose a $250,000 IUL with a 0% floor and an 11% cap. Over ten years the cash value grew about 6% a year, giving him a cushion he could tap for a home repair without tapping his emergency fund.

Key features to watch:

- Cap rate , the max credit you can earn each year.

- Participation rate , the percentage of index gains that actually get credited.

- Floor , usually 0%, meaning your cash value won’t go negative.

Because single parents often have irregular income, the flexibility to adjust premiums is a big win. If you get a bonus at work, you can add it to the cash bucket. If cash flow tightens, the cash value can cover the COI for a while.

For more technical details, read NerdWallet’s explanation of indexed universal life insurance.

Another useful resource is the same NerdWallet page, which breaks down how the interest crediting works and what the caps and floors mean for your growth.

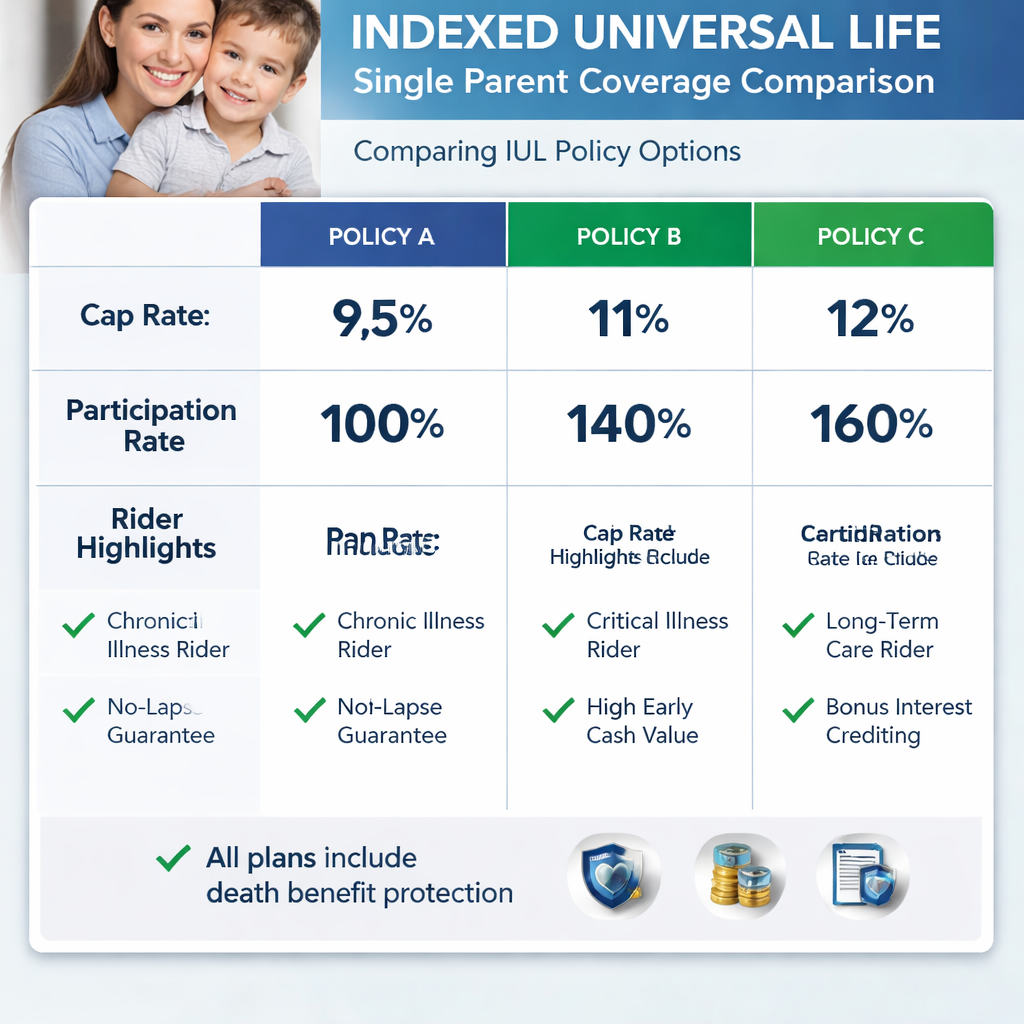

Step 3: Visualize Policy Options with a Comparison Chart

With the basics clear, it’s time to compare actual policies. Indexed universal life single parent coverage comes from many carriers, each with its own caps, fees, and riders.

Here’s a quick snapshot of three popular options that many families find reliable. The data comes from GetAmplifyLife and OgleTreeFinancial, two sources we trust for up‑to‑date numbers.

Notice how the caps differ. A higher cap can boost cash growth, but it often comes with higher fees. Look for a carrier that balances the two.

Real‑world tip: A single parent in Texas chose the Amplify plan because the digital portal let her track cash value daily. She set up automatic premium increases when she got a raise, which helped the cash bucket grow faster.

When you compare policies, ask yourself:

- What is the cap and does it match my risk tolerance?

- Does the carrier have a good track record of treating policyholders fairly? (OgleTreeFinancial’s analysis shows that companies with strong treatment histories tend to keep caps stable.)

- Are the living‑benefit riders worth the extra cost for my situation?

For a deeper dive into the best IUL carriers, read the GetAmplifyLife article on top indexed universal life insurance options.

OgleTreeFinancial also publishes a detailed look at how caps and participation rates affect cash growth.

Step 4: Choose and Purchase the Right IUL Policy

Now you have the numbers, it’s time to lock in a policy. Indexed universal life single parent coverage isn’t a one‑size‑fits‑all product, so follow these steps.

1. Pick a carrier with A+ ratings from A.M. Best. That signals the company can pay claims for decades.

2. Decide on a death benefit amount based on the needs analysis you did in Step 1.

3. Choose a premium schedule you can afford. Remember you can raise or lower payments later.

4. Add any riders that matter , a living‑benefits rider, a long‑term‑care rider, or an accelerated death‑benefit rider.

5. Get a personalized illustration. This shows projected cash value, cap credits, and COI over time.

Real‑world example: A single mother in Florida used Life Care Benefit Services to compare three quotes. She chose the Nationwide option because its low COI kept the cash value from eroding, and the LTC rider gave her peace of mind for future health needs.

When you work with an independent agency like Life Care Benefit Services, you get access to over 50 carriers. That means the quote you receive reflects the best match for your budget and goals.

After you sign, the insurer will ask for a medical exam. It’s usually quick , a blood draw and a short questionnaire. Once approved, you’ll receive the policy documents and can start paying premiums.

Don’t forget to set up online access so you can watch the cash value grow. Most carriers let you log in and see the numbers in real time.

Step 5: Keep Your Coverage Flexible with Ongoing Reviews

The job isn’t done after you buy. Indexed universal life single parent coverage needs a yearly check‑up to stay on track.

Investopedia explains that cash value is credited each year based on the index performance. If the market does poorly, your cash value may barely move. If the market soars, you could see a nice bump, but only up to the cap.

Schedule a review at least once a year. During the review, look at:

- Cash‑value balance versus projected growth.

- Cost‑of‑insurance charges , they rise with age, so make sure you have enough cash to cover them.

- Any life changes , a new job, a raise, a child graduating.

Here’s a quick checklist you can print:

- Pull the latest annual statement.

- Compare actual cash growth to the illustration.

- Adjust premiums if the cash value is lagging.

- Consider adding or removing riders based on new needs.

Watch a short video on how to run a policy review. It walks you through the steps and shows what numbers to focus on.

Guardian Life notes that the COI tends to climb after age 60, so many families boost their premium contributions in their 50s to build a larger cash cushion.

Finally, keep beneficiary designations up to date. A new child, a divorce, or a new partner changes who should receive the death benefit.

FAQ

What does indexed universal life single parent coverage protect?

It gives a tax‑free death benefit to your kids or other loved ones if you pass away. At the same time, the policy builds cash value that you can borrow against for emergencies, college costs, or retirement. The cash grows based on a market index, but a floor protects it from losing value when markets drop.

How much premium should I expect to pay?

Premiums depend on age, health, and the death benefit you choose. A typical single parent in their 30s might pay $80‑$120 a month for a $250,000 death benefit with a modest cash‑value component. You can start lower and increase payments later as your income grows.

Can I change the death benefit later?

Yes. Indexed universal life single parent coverage lets you raise or lower the death benefit, as long as the policy stays in force. Raising the benefit may require higher premiums, while lowering it can free up cash to grow the cash value.

What are the main fees I should watch?

The biggest fee is the cost‑of‑insurance (COI), which covers the death benefit protection. There are also administrative fees and any rider charges you add. Look for carriers with low COI, like Nationwide, because lower fees mean more of your premium goes to cash growth.

How do I access cash value without hurting the policy?

You can take a policy loan. The loan is tax‑free as long as the policy stays active. The loan amount plus interest is deducted from the death benefit when you pass away. Keep the loan‑to‑value ratio below 80% to avoid a taxable event.

Do I need a medical exam?

Most indexed universal life single parent coverage plans require a quick medical exam , a few blood draws and a short health questionnaire. Some carriers offer simplified issue policies with no exam if you’re under a certain age and in good health.

Is this better than a term policy with a rider?

Term policies are cheaper but only last for a set number of years and have no cash value. Indexed universal life single parent coverage gives lifelong protection and a cash‑value bucket you can use while you’re alive. If you want both protection and a way to save for college or retirement, IUL usually wins.

Conclusion & Next Steps

Indexed universal life single parent coverage blends protection and growth in one plan. You get a death benefit for your kids, a cash‑value account that can help with school costs or a mortgage, and the flexibility to adjust premiums as life changes.

Start by running a needs analysis, compare a few carriers, and get a personalized illustration. Then lock in a policy with a carrier that has strong ratings and low COI. Finally, set a yearly review reminder so you can keep the policy on track.

If you’re ready to take the next step, schedule a free consultation with Life Care Benefit Services. Our agents will walk you through the numbers, answer any questions, and help you file the paperwork. Protect your family today and build a financial safety net for tomorrow.