Mortgage Protection Insurance for First‑Time Homebuyers: A Step‑by‑Step Guide

First‑time buyers often think the biggest cost is the down‑payment. The truth is the mortgage itself can become a huge risk if something happens to you. If you die or become disabled, the loan could fall on your family. This guide walks you through every step to protect that loan with mortgage protection insurance.

We’ll show how to size the coverage, compare it to traditional life insurance, add living‑benefit riders, pick the right carrier, apply, and keep the policy fresh. By the end you’ll have a clear action plan you can follow tonight.

Step 1: Assess Your Current Life Insurance and Financial Needs

Before you look at any new policy, you need a snapshot of what you already have. Grab any existing life‑insurance statements, term policies, or accidental death riders. Write down the face amount, the premium you pay each month, and the beneficiaries listed.

Next, list your monthly housing costs. The mortgage payment is the headline, but don’t forget property taxes, homeowners insurance, HOA fees, and any escrow items. Add them up , that’s the total cash flow you must protect.

Now think about your emergency fund. How many months of the total housing cost could you cover if the income stopped? Most experts suggest at least three months. If you fall short, that gap is where mortgage protection insurance can step in.

When you have those numbers, compare the death benefit of your existing life insurance to the remaining mortgage balance. If the life policy’s face amount is lower than the loan, you’ll need extra coverage.

Don’t forget future changes. If you plan to refinance, the loan balance could drop, which would lower the needed protection. Conversely, a home‑equity line could raise the amount you need to shield.

Finally, write a quick checklist:

- Current life‑insurance face amount

- Monthly mortgage‑related costs

- Emergency‑fund months covered

- Planned refinances or equity draws

Having this checklist makes the next steps far less intimidating. What Is Mortgage Protection Insurance? A Complete Guide offers a deeper look at why that checklist matters.

Step 2: Understand Mortgage Protection Insurance vs. Traditional Life Insurance

Mortgage protection insurance (MPI) is a policy that pays the lender directly if you die, become disabled, or in some plans, lose your job. Traditional life insurance pays a lump sum to a named beneficiary, who can use the money for anything.

Because MPI’s benefit matches the outstanding loan balance, the payout shrinks as you pay down the mortgage. The premium, however, usually stays the same. A term life policy’s death benefit stays level, which can be useful if you want cash for other debts.

One big difference is underwriting. Most MPI policies require little or no medical exam. Bankrate notes that many MPI plans offer guaranteed acceptance, while traditional life insurance looks at health, age, and occupation.

Cost is another factor. MPI premiums can range from $5 to $100 a month, depending on age, loan size, and health. Traditional term life for the same coverage amount often costs less because the benefit isn’t tied to the mortgage balance.

Both types have pros and cons. MPI gives peace of mind that the home stays paid, but the benefit cannot be used for other expenses. Term life offers flexibility, but you must manage the payout yourself.

When you decide which route fits, ask yourself:

- Do I need a benefit that goes straight to the lender?

- Am I comfortable with a decreasing benefit?

- Do I want the option to add riders for disability or critical illness?

Answering these questions helps you see where MPI or a term policy makes sense for your situation.

Step 3: Evaluate Policies with Living Benefits and Indexed Universal Life (IUL)

Living‑benefit riders let you tap the policy while you’re still alive. Common riders cover critical illness, chronic illness, or a short‑term disability that stops you from working. Those payouts can help cover mortgage payments, home repairs, or other bills.

Indexed Universal Life (IUL) blends a death benefit with a cash‑value component that grows based on a market index, not the stock market itself. The cash value can be borrowed against to pay the mortgage if needed, and the death benefit can stay level or increase.

According to Legacy Agent, UL and IUL policies can be designed to provide at least 20 years of coverage with a minimum premium. They also allow riders at no extra cost, which is rare in the MPI market.

When you compare options, look at three things:

- Premium stability , does the carrier lock the rate for the term?

- Rider availability , can you add a disability or critical‑illness rider?

- Cash‑value growth , does the IUL credit interest based on a reliable index?

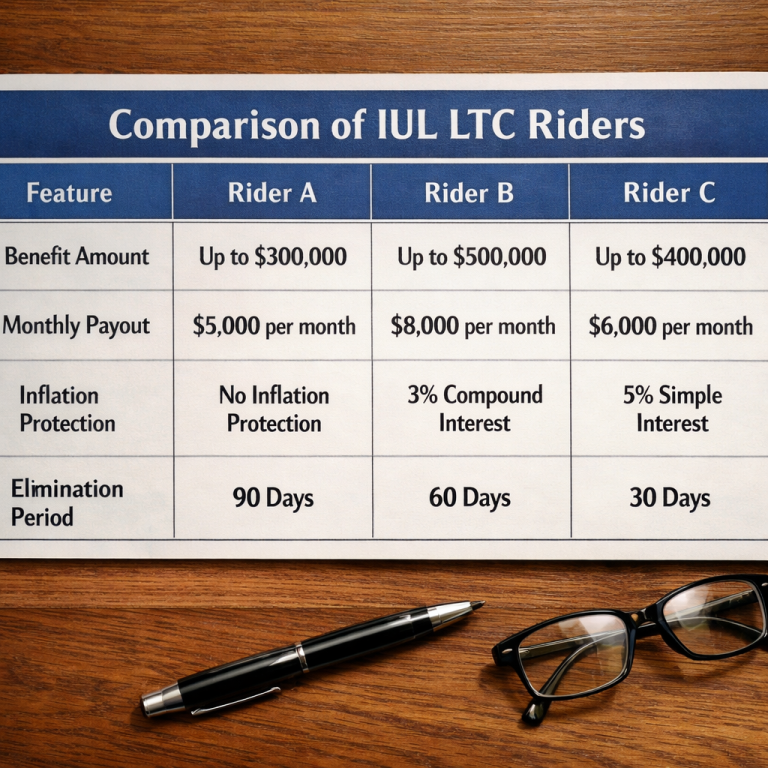

Below is a quick matrix to help you see the trade‑offs.

Imagine you’re 45, own a $250K mortgage, and want a policy that lasts 20 years. A term policy might cost $30 a month, an MPI could be $45, and an IUL could start at $55 but give you a cash reserve you can draw on later.

Step 4: Compare Top Providers and Get Quotes

Now that you know what features matter, it’s time to see which carriers actually offer them. Look for insurers with strong financial ratings (A‑M or higher from AM Best) and a solid track record in mortgage protection.

Life Care Benefit Services partners with over 50 carriers, but a few stand out for first‑time buyers:

- Provider A, offers a no‑exam MPI with a 30‑day waiting period and optional disability rider.

- Provider B, combines a decreasing term mortgage policy with a low‑cost critical‑illness rider.

- Provider C, sells an IUL product that lets you add a living‑benefit rider at no extra charge.

When you request quotes, ask for a side‑by‑side comparison that includes:

- Monthly premium for the exact loan balance.

- All riders and their costs.

- Policy length and any renewal rules.

Don’t forget to verify the underwriting process. Some carriers require a full medical exam; others only need a health questionnaire. The easier the process, the faster you can lock in a rate.

New York Life explains that a flexible mortgage‑protection plan can include both term and permanent layers, giving you the ability to keep coverage after the loan is paid off New York Life’s homeowner overview. That flexibility can be valuable if you want cash value later on.

Once you have three quotes, line them up in a simple grid. Rate the carriers on price, rider options, underwriting ease, and customer service. Choose the one that scores highest on the criteria that matter most to you.

Step 5: Apply for Your Policy and Set Up Coverage

Application time is where many people stall. Keep the process smooth by having these items ready:

- Most recent mortgage statement.

- Proof of identity (driver’s license or passport).

- Two years of tax returns if you’re self‑employed.

- Answers to basic health questions (smoking status, chronic conditions).

Log onto the insurer’s quote portal, enter the loan balance, choose the coverage amount, and select any riders you need. The system will instantly show a premium estimate.

Review the illustration carefully. It should show the monthly premium, the death benefit amount at each year, and any rider costs. If the numbers look high, tweak the coverage or switch from a decreasing to a level benefit.

When you’re satisfied, submit the application. The insurer will run a quick underwriting check. Because many MPI policies have minimal underwriting, you’ll often hear back within 48 hours.

After approval, you’ll receive a policy packet. Sign the documents, pay the first month’s premium, and keep a digital copy in a safe folder labeled “Mortgage Protection.”

Below is a short video that walks you through the online quote flow step by step.

Once the policy is active, the insurer will send you a welcome letter that includes the beneficiary (the lender) and the exact benefit amount. Keep that letter with your mortgage paperwork.

Step 6: Review and Update Your Policy Annually

Mortgage protection isn’t a set‑and‑forget product. Each year, pull your latest mortgage statement and compare the outstanding balance to the policy’s death benefit. If the balance has dropped far below the coverage, you might lower the benefit and save on premiums.

Also check for new riders. A disability rider you didn’t need last year could become valuable if your job changes. Likewise, if you’ve added a home equity line, you may want to increase coverage.

Finally, watch for premium changes. Some carriers guarantee the rate for the life of the policy, while others adjust after a set period. If the premium jumps, shop quotes again , you may find a better deal.

Mark your calendar for the policy’s renewal date. Set a reminder two weeks before, then spend an hour reviewing the numbers. Small tweaks each year can keep the protection affordable and aligned with your real needs.

Frequently Asked Questions

What is the difference between mortgage protection insurance and private mortgage insurance (PMI)?

Mortgage protection insurance (MPI) is optional and pays the lender if you die or become disabled. Private mortgage insurance (PMI) is required by lenders when the down‑payment is under 20 % and only covers default risk. MPI benefits the borrower’s family; PMI protects the lender.

Can I add a living‑benefit rider to a standard term life policy?

Yes, many carriers let you attach a critical‑illness or disability rider to a term policy for an extra cost. The rider pays a portion of the death benefit while you’re alive, helping with mortgage payments if you can’t work.

Do I need a medical exam for mortgage protection insurance?

Most MPI plans offer no‑exam options that rely on a health questionnaire and income documentation. This makes them popular with gig‑workers and self‑employed borrowers.

How does an Indexed Universal Life policy differ from a regular whole‑life policy?

An IUL ties cash‑value growth to a market index, offering higher potential gains without direct stock market risk. Whole‑life policies provide a guaranteed cash‑value increase but usually at a lower rate.

Will the MPI premium stay the same as my mortgage balance shrinks?

In most cases, the premium is fixed for the term you choose. The death benefit, however, decreases as you pay down the loan, so you may end up paying more than the current balance.

What happens if I refinance my mortgage?

Refinancing changes the loan balance and possibly the term. You’ll need to adjust your MPI coverage to match the new balance, which may involve a new quote or a rider amendment.

Is mortgage protection insurance worth it if I already have a term life policy?

If your term policy’s death benefit exceeds the mortgage balance, you may not need a separate MPI. However, MPI can offer lower premiums for the exact loan amount and may include disability riders that term policies lack.

Can I cancel my mortgage protection policy if I sell the house?

Yes, you can cancel the policy at any time. Make sure to request a refund of any unused premium if the policy includes a return‑of‑premium feature.

Conclusion

Protecting your home is more than buying a roof. Mortgage protection insurance fills the gap when life throws a curveball. By assessing your current coverage, understanding how MPI stacks up against term life, evaluating living‑benefit riders and IUL options, comparing providers, and following a clear application process, you can lock in the right protection.

Remember to review the policy each year, especially after major life events or mortgage changes. A small adjustment now can save a lot of worry later. If you’re ready to take the next step, reach out to a trusted independent agent at Life Care Benefit Services for personalized quotes and guidance.