IUL Riders for Long Term Care: A Step-by-Step Guide

Long-term care can cost over $100,000 a year. IUL riders for long term care coverage let you tap your life insurance policy to pay for it. Here’s how to pick and use one.

Step 1: Understand How IUL Riders for Long Term Care Coverage Work

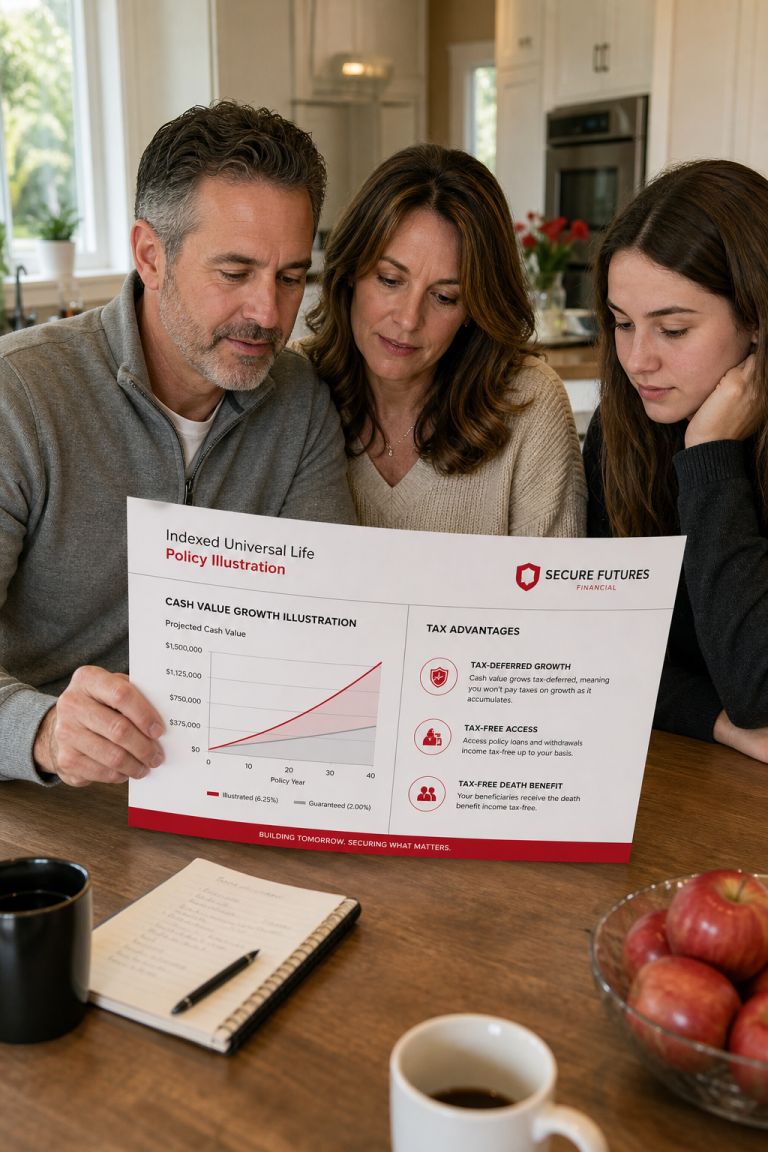

An IUL policy grows cash value based on a stock market index. A long-term care rider lets you take a portion of the death benefit early if you need care. You don’t buy a separate LTC policy , the rider attaches to your existing life insurance.

Here’s how it works: If you become chronically ill and can’t perform two of six activities of daily living (bathing, dressing, eating, etc.), the rider pays out a monthly benefit. The money comes from accelerating the death benefit. For example, a 2% monthly acceleration on a $500,000 policy gives you $10,000 per month.

Carriers like Equitable offer optional LTC riders on their IUL policies. According to their documentation, the rider provides a monthly benefit for qualified long-term care services through an acceleration of the death benefit. You choose an acceleration percentage , typically 1%, 2%, or 3% per month. The amount you receive reduces the death benefit your beneficiaries get later.

Riders have a cost. A monthly charge is deducted from your policy’s cash value. That charge continues until you turn 100 (age 121 on a guaranteed basis) or until you start receiving benefits. Some policies have a 90-day elimination period before benefits start. Check with your agent about specific terms.

Step 2: Evaluate Your Long Term Care Needs and Budget

Before you buy a rider, figure out how much care might cost and how you’d pay. The national average for a semi-private nursing home room is over $112,000 per year, according to the Federal Long Term Care Insurance Program website. If inflation averages 2.5%, that could hit $186,000 in 20 years.

Think about where you’d want care: at home, in an assisted living facility, or in a nursing home. Home care is often cheaper but still runs about $33 per hour for a home health aide. Multiply that by hours per week , it adds up fast.

Now look at your retirement savings, Social Security, and other income. Can you cover a big expense without wrecking your plan? The average 65-year-old today will need about $135,000 set aside just for future LTC costs. If you don’t have that, an IUL rider might fill the gap.

Step 3: Compare IUL Policies with LTC Riders from Top Carriers

Not all IUL riders are the same. Carriers differ in monthly benefit percentages, elimination periods, and costs. Here are some well-known options based on publicly available information:

- Equitable: Offers a Long-Term Care Services Rider with 1%, 2%, or 3% monthly acceleration. Maximum enrollment age is 70. Has a 90-day elimination period that can be satisfied with 60 service days.

- Brighthouse SmartCare: A hybrid policy that can be linked to an IUL. Offers a cash indemnity payout , you get the full monthly benefit without submitting receipts. Good for simplicity.

- Nationwide CareMatters: Combines life insurance with LTC. Available up to age 75. Pays up to $20,000 per month in cash. You can choose benefit periods from 2 to 7 years.

- MassMutual CareChoice: A whole life hybrid, but they also offer riders on some IUL products. Best known for high customer satisfaction scores.

When comparing, look at the monthly benefit amount, how long it pays, and the elimination period. A CNBC review of LTC insurance notes that the best policies offer inflation protection and flexible care options. Ask for side-by-side illustrations from each carrier.

For families and small business owners, the combination of growth potential and living benefits makes IUL riders attractive. An agent can run illustrations showing how different acceleration percentages affect your death benefit and cash value.

Step 4: Review Policy Riders and Exclusions Carefully

The fine print matters. Many long-term care insurance policies have tricky terms that can delay or deny a claim. The same is true for IUL riders. Read the rider endorsement closely with your agent.

Common exclusions include pre-existing conditions, certain neurological disorders, and requirements that care be provided by licensed non-family members. Some policies won’t cover adult day care or services that let you age in place. from Jonathan M. Feigenbaum, Esquire, ambiguous policy language often benefits the insurance company unless challenged.

Also check if the rider requires a certain number of days of care per week to qualify. The elimination period might be 90 days of continuous care. Make sure you understand what ‘qualified long-term care services’ means in your policy.

One way to avoid surprises is to work with an independent agent who can explain the differences between carriers. Life Care Benefit Services, for example, partners with over 50 carriers and can help you compare riders side by side.

Step 5: Apply with a Trusted Independent Agent Like Life Care Benefit Services

Once you know what you need and which carriers fit, it’s time to apply. You can’t add an LTC rider to any IUL , you need a policy that offers it at issue. That’s where an independent agent adds value.

Life Care Benefit Services helps families and small business owners find affordable, highly-rated IUL policies with living benefit riders. They shop across multiple carriers, not just one. You get quotes from carriers like Equitable, Brighthouse, and Nationwide. Their agents explain the differences in plain language.

To start, you’ll provide basic health history and financial goals. The agent runs illustrations showing how much monthly LTC benefit you’d get and how it impacts the death benefit. Then you choose the policy that fits.

If you want to learn more about how living benefits work in practice, : how to access living benefits on your IUL policy.

Applying with an independent agent means you get unbiased advice. You’re not locked into one company’s products. And you have someone to help if you ever need to file a claim.

Frequently Asked Questions

How much does an IUL long-term care rider cost?

The cost varies by carrier, age, health, and the acceleration percentage you choose. Typically, a monthly charge is deducted from your policy’s cash value. For a 55-year-old in good health, the rider cost might be a small percentage of the premium. Get an illustration for exact numbers.

Can I add an LTC rider to an existing IUL policy?

Usually no. Most carriers require the LTC rider to be selected at the time you apply for the policy. You cannot add it later. However, some carriers allow adding a chronic illness rider within a certain period after issue. Check with your agent.

What’s the difference between an LTC rider and a chronic illness rider?

Both accelerate the death benefit, but the triggers differ. An LTC rider often requires you to need help with at least two activities of daily living for a period of time. A chronic illness rider may have similar triggers but can be less strict about care location. Some policies use the terms interchangeably.

Does an IUL LTC rider cover home health care?

It depends on the carrier. Some riders cover care in any setting, including your home. Others restrict benefits to licensed facilities. Read the rider language carefully. Many modern policies cover home health aides if they are licensed and provide certified care.

Will the LTC rider reduce my death benefit permanently?

Yes. Any benefit you receive through the rider reduces the death benefit dollar for dollar (or sometimes more, depending on the carrier). If you use all the available LTC benefit, the death benefit could be zero. Make sure you understand the trade-off.

Conclusion: Secure Your Future with IUL LTC Riders

IUL riders for long term care coverage give you a way to protect your savings from high care costs without buying a standalone LTC policy. The key is to understand how they work, compare carriers, and review exclusions. Work with an independent agent like Life Care Benefit Services to find the right fit for your family. Then apply while you’re still healthy enough to qualify.