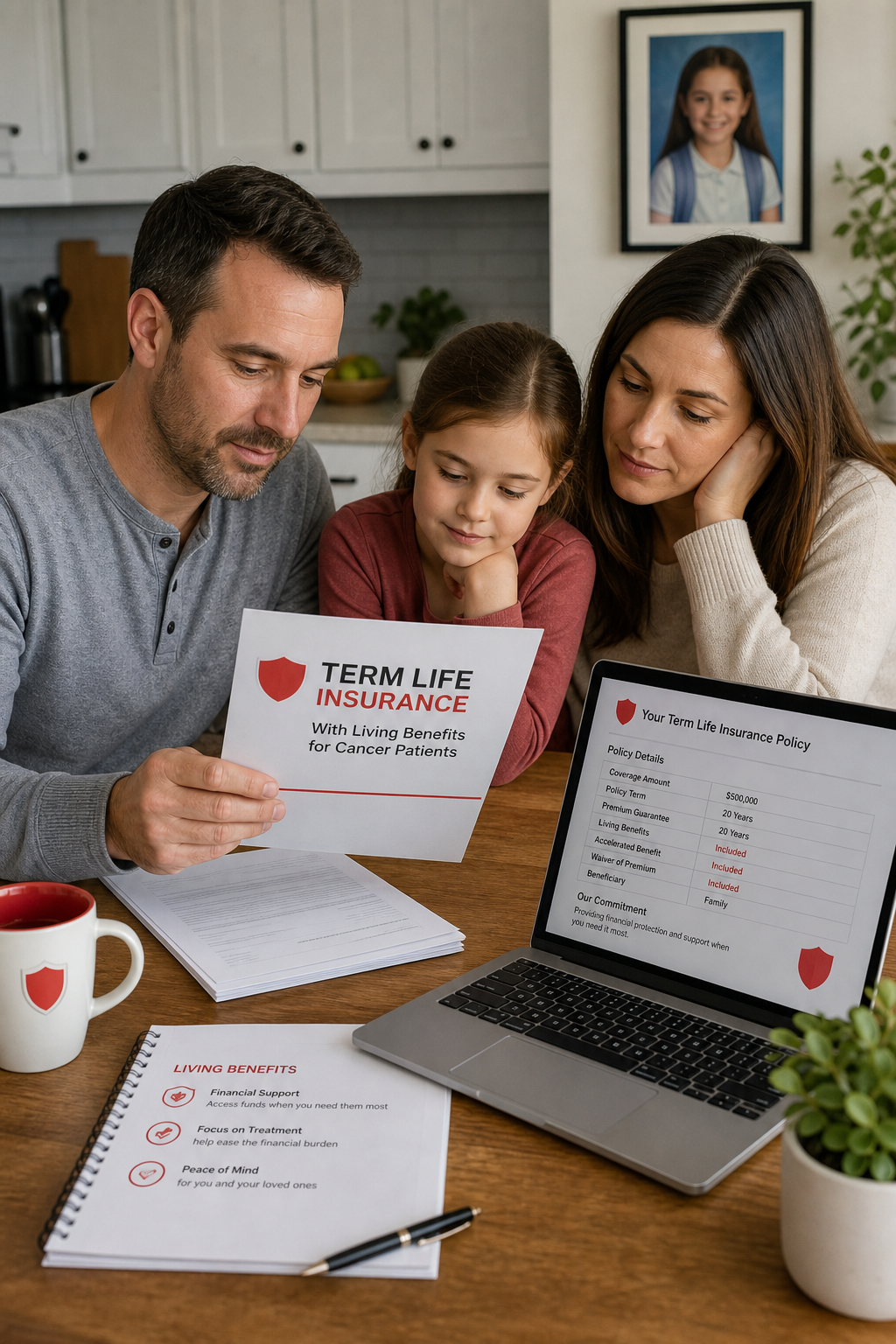

Top Living Benefits Life Insurance for Cancer Patients (2026)

When a cancer diagnosis hits, bills can pile up fast. You need money now, not later. Living‑benefits life insurance can turn a death benefit into cash you can use while you’re still alive. In this article you’ll see eight options, how they work, and tips to pick the right one for your situation.

1. Indexed Universal Life (IUL) with Accelerated Death Benefit , Our Top Pick for Cash Value Growth

Indexed universal life blends permanent coverage with a cash‑value component that can grow when the market does, but it won’t lose money if the market falls. The real power for cancer patients is the accelerated death benefit rider. If a doctor confirms a terminal or critical illness, you can tap a portion of the death benefit early. That cash can cover treatment, travel, or everyday bills.

Fidelity & Guaranty Life (F&G) offers three riders: terminal, chronic, and critical illness. Each can pay up to 100% of the face amount, though most people take 25%‑50% to keep some protection for loved ones. The rider costs nothing extra if you’re in a good rating class, so you don’t pay a hidden premium.

Here’s a quick look at how it works:

- Buy a policy with a face amount that meets your long‑term needs.

- Choose the living‑benefits rider when you apply.

- If you get a qualifying diagnosis, file a claim with a doctor’s statement.

- The insurer releases a lump‑sum that reduces the death benefit by the same amount.

Because the cash value stays invested, you can also borrow or withdraw from it later. That gives you extra flexibility if you outlive the illness.

Real‑world example: Jeff, a 52‑year‑old small‑business owner, bought a $500,000 IUL with a 30% critical‑illness rider. When he was diagnosed with invasive cancer, he accessed $150,000. He used the money for chemo, a home‑care nurse, and to keep his business running. His death benefit fell to $350,000, but his family still had a solid safety net.

Life Care Benefit Services helps you compare IUL options and walk you through the claim process. How to claim living benefits from an IUL after a cancer diagnosis explains each step in plain language.

According to F&G’s guide, policyholders who used the rider reported lower stress and better focus on treatment. The cash infusion can be the difference between delaying care and getting the best possible therapy.

2. Whole Life Insurance with Critical Illness Rider , Guaranteed Benefits and Fixed Premiums

Whole‑life policies promise a guaranteed death benefit and a cash‑value that grows at a set rate. Add a critical‑illness rider and you get a lump‑sum payout if you are diagnosed with a covered condition such as cancer, heart attack, or stroke. The premium never changes, so budgeting stays simple.

MetLife’s critical‑illness rider is a good example. It pays directly to you, not the doctor, and can be used for anything , from medical bills to mortgage payments. Because the rider is built into the policy, there’s no extra medical exam needed once the base policy is in force.

Key features:

- Fixed monthly premium for the life of the policy.

- Cash value that can be borrowed against tax‑free up to your basis.

- Critical‑illness payout that does not affect the death benefit if you choose a “return of premium” option.

Imagine Sarah, a 45‑year‑old teacher, who bought a $300,000 whole‑life policy with a 15% critical‑illness rider. After a breast‑cancer diagnosis, she received $45,000. She used it for surgery, a short‑term disability gap, and to keep her kids’ school fees paid. Her cash value kept growing, and the death benefit stayed at $255,000.

Because whole life is straightforward, it works well for families who want predictability. The fixed premium means you won’t see a surprise hike if your health changes. The rider’s cost is baked into the overall price, so there’s no hidden fee.

MetLife’s official page explains how the rider works and why it’s a solid choice for cancer patients MetLife Critical Illness Insurance.

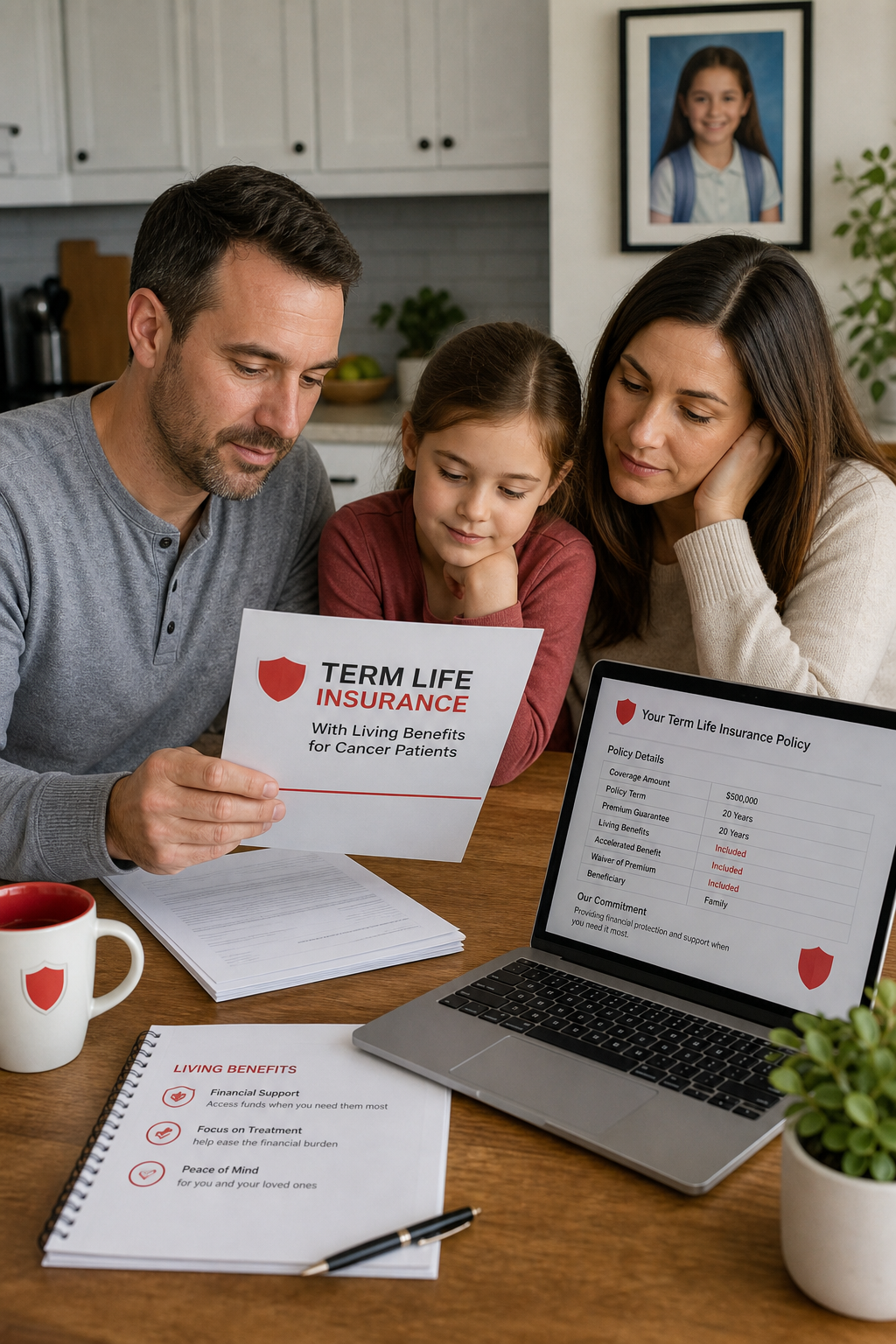

3. Term Life Insurance with Living Benefits Rider , Affordable Coverage That Converts on Diagnosis

Term life is the most affordable way to get a death benefit for a set number of years. When a living‑benefits rider is added, the policy can pay out a portion of the benefit if you are diagnosed with a serious illness during the term. The rider usually offers 10‑30% of the face amount, but you keep the rest for your beneficiaries.

This option works well for younger families who need coverage while the kids are in school or the mortgage is being paid down. The base premium stays low, and the rider adds a layer of protection without turning the policy into a cash‑value vehicle.

How the rider kicks in:

- You buy a 20‑year term with a $500,000 face amount.

- You add a living‑benefits rider that can pay up to 20% ($100,000) on a qualifying diagnosis.

- After a doctor’s statement, the insurer releases the payout.

- The remaining $400,000 stays as the death benefit for your loved ones.

Real example: Lita, a mother of six, chose a term policy with a living‑benefits rider after her diagnosis of stage‑II breast cancer. She accessed $80,000 to cover a temporary loss of income and to keep the family home. When she went into remission, the policy continued until the original term end, protecting her children’s future.

Term policies with living benefits are offered by several carriers, but you should watch for waiting periods and caps. Some policies require a 30‑day waiting period before the rider becomes payable, while others have no waiting period. Check the fine print before you sign.

When you compare term riders, look for:

- Clear definition of “qualifying illness.”

- Percentage of benefit that can be accessed.

- Any waiting period or exclusion for pre‑existing conditions.

- Cost of the rider as a dollar amount per $1,000 of coverage.

Choosing a term rider can give you the low cost of term life plus a safety net if cancer strikes.

4. Group Life Insurance Through Employer , Often Includes Living Benefits at No Extra Cost

Many employers bundle group life insurance with a living‑benefits rider. The advantage is that the coverage is often guaranteed issue, meaning you don’t have to answer health questions. This can be a lifesaver for cancer patients who might be turned down by individual carriers.

Group policies usually have a set face amount, such as $50,000 or $100,000, but the rider can let you access a portion if you are diagnosed with a serious illness. Because the cost is covered by the employer, you pay nothing extra.

Key points to consider:

- Eligibility , you must be a full‑time employee and meet any waiting period the plan sets (often 30 days after hire).

- Benefit amount , the living‑benefits payout is usually a percentage of the group face amount.

- Portability , if you leave the job, the coverage may end, so you might need a personal policy to fill the gap.

A real‑world case: Mark worked for a mid‑size tech firm that offered a group life plan with a chronic‑illness rider. When he was diagnosed with leukemia, the rider paid out $20,000, which he used for travel to a specialist and for a home‑care aide. Because the policy was employer‑paid, Mark didn’t see any extra premium.

Group life can be a quick win, especially if you’re just starting a career and haven’t built up personal coverage yet. Talk to your HR department about the exact terms, and ask for a copy of the rider language.

For a deeper look at how group plans work, see Aflac’s overview of living‑benefits options for employees Aflac Living Benefits Overview. (Note: this link is an authority source that explains the mechanics.)

5. Guaranteed Issue Life Insurance , No Medical Exam Option for Cancer Patients

If you have an active cancer diagnosis, many traditional policies will either reject you or charge sky‑high rates. Guaranteed‑issue policies step in as a last‑ditch option. They don’t require a medical exam, and you answer no health questions. The trade‑off is a higher premium and a lower death benefit, often limited to $25,000‑$50,000.

These policies are useful for covering final expenses, funeral costs, or a small debt load. Some carriers also allow a limited cash‑value component that can be borrowed against, but the amounts are modest.

Consider these factors before you buy:

- Benefit limit , make sure the face amount covers the expenses you expect.

- Premium cost , compare the monthly payment to your budget.

- Waiting period , some policies have a 2‑year “graded” period where the death benefit is reduced if you die early.

- Policy length , most are whole life, so they stay in force as long as you pay.

Example: Carlos, a 60‑year‑old retired teacher, was diagnosed with prostate cancer. He applied for a guaranteed‑issue whole‑life policy with a $30,000 face amount. The premium was $45 a month. When his condition worsened, the policy paid the full $30,000 to cover hospice care and funeral costs. Because there was no medical exam, the application was quick and painless.

While the payout is modest, the peace of mind can be worth it, especially if you already have other coverage for larger needs.

Remember that guaranteed‑issue policies are permanent, so the cash value will grow slowly over time. If you later qualify for a traditional policy, you can often convert to a larger, cheaper plan.

How to Choose the Right Living Benefits Policy for Your Cancer Risk Profile

Picking a policy is about matching your health status, budget, and long‑term goals. Here’s a simple checklist you can run through.

- Health stage:If you are in remission, a permanent policy (IUL or whole life) gives you cash‑value growth. If you are actively undergoing treatment, a term rider or group plan may be cheaper.

- Coverage need:Estimate the amount you’d need for treatment, lost income, and any debt. Aim for a payout that covers three to six months of expenses plus a buffer.

- Premium comfort:Fixed premiums (whole life) are easy to budget. Flexible premiums (IUL) let you pay more in good years and less when cash is tight.

- Rider details:Look for clear trigger language, low waiting periods, and no hidden caps.

- Portability:If you might change jobs, a personal policy (IUL or whole life) stays with you, while group coverage ends.

After you score each item, compare the total points. The highest‑scoring option usually fits best. If you’re unsure, talk to a licensed agent who can run side‑by‑side quotes.

Quick Comparison: Top Living Benefits Life Insurance Options for Cancer Patients

Use this table as a snapshot. Your final decision should factor in your personal health timeline and how much cash you might need now versus later.

Frequently Asked Questions About Living Benefits Life Insurance for Cancer Patients

What is a living‑benefits rider?

A living‑benefits rider is an add‑on to a life‑insurance policy that lets you tap into part of the death benefit while you are still alive if you are diagnosed with a qualifying condition such as cancer, a heart attack, or a chronic illness that limits daily activities. The payout reduces the eventual death benefit by the amount you receive.

Can I add a living‑benefits rider to an existing policy?

Yes, many carriers let you add a rider during the policy’s open enrollment period or at renewal. You’ll need to submit a rider application and possibly a medical statement, but you won’t have to re‑underwrite the whole policy. Adding the rider later may increase your premium slightly.

Do living‑benefits payouts affect my taxes?

Most payouts are received tax‑free because they are considered an advance on a death benefit. However, if the amount you receive exceeds your paid‑in premiums, the excess could be taxable. It’s best to consult a tax professional before you file a claim.

How quickly can I get the money after a diagnosis?

Once the insurer receives a completed claim form, a physician’s statement, and any required documentation, many carriers process the payment within 10‑14 business days. Some companies, like Aflac, promise faster turnaround if you use their online portal.

Will my premiums go up after I use a living‑benefits rider?

Generally, the premium stays the same because the rider’s cost is built into the original price. The only change is the reduced death benefit. However, if you add a new rider after the policy is in force, the carrier may adjust the premium to cover the added risk.

Is there a waiting period before I can use the rider?

Some policies impose a short waiting period, often 30 days, from the start of the policy or from the date of diagnosis. Others have no waiting period but may exclude conditions that existed before the policy began. Always read the fine print.

What happens if I outlive my term policy with a living‑benefits rider?

If the term ends without a claim, the policy simply expires and you receive no cash. Some carriers offer a “return of premium” option that refunds a portion of the premiums paid, but that adds cost. You can also convert the term to a permanent policy at the same underwriting class, preserving the rider if you still need it.

Can I combine more than one living‑benefits rider?

Usually you can choose one primary rider, either critical‑illness, chronic, or terminal. Adding multiple riders may be possible but can raise the premium sharply and may create overlapping payout limits. Discuss your needs with an agent to avoid redundant coverage.

Conclusion

Living‑benefits life insurance gives you a financial safety net when cancer strikes. The right choice depends on where you are in your health journey, how much you can afford each month, and whether you want cash‑value growth or a simple, low‑cost plan.

Our top pick, an Indexed Universal Life policy with an accelerated death benefit rider, offers growth potential, flexible premiums, and a powerful cash‑out option. Whole life with a critical‑illness rider adds predictability, while term policies give the lowest cost. Group coverage can be a free add‑on through your employer, and guaranteed‑issue plans serve as a fallback when other options aren’t available.

Take the checklist from the “How to Choose” section, run side‑by‑side quotes, and talk to a licensed agent at Life Care Benefit Services. They can help you compare carriers, explain rider language, and file a claim quickly if the need arises.

Secure the peace of mind that comes from knowing you have money in hand while you focus on treatment, not bills. Get a quote today and protect your family’s future now.