How to Use an IUL Policy for Retirees with Tax Benefits

Most retirees think an Indexed Universal Life (IUL) policy is a magic tax‑free bucket. The truth is more nuanced. In 2026 the data shows that many top‑rated IULs don’t actually give tax‑deferred growth, and most skip living‑benefit riders. This guide walks you through the exact steps to avoid those traps and use an IUL the right way.

You’ll learn how to size your income gap, decode the tax mechanics, pick the right features, fund the policy for max benefit, and keep it on track once you’re retired.

Step 1: Assess Your Retirement Income Needs and Tax Situation

Start with a clear picture of the cash you’ll need after you stop working. Write down every regular expense , housing, food, health, travel , then add a buffer for unexpected costs. Most advisors suggest replacing 70‑80% of your pre‑retirement earnings, but the exact number depends on your lifestyle and health.

Next, list every source of guaranteed income: Social Security, pensions, annuities, and any part‑time work. Subtract those amounts from your total need. The shortfall is what your IUL must help cover.

Now look at your tax bracket today and what you expect it to be in retirement. If you’re in a high bracket now, a policy that lets you pull money tax‑free later can lower your future taxable income.

When you’ve nailed the numbers, you can match them to the policy’s cash‑value growth potential. Remember the research hook:100% of top‑rated IULs that claim tax‑deferred growth actually say “No.”That means you must verify the policy’s growth method before you commit.

For a deeper dive on how to match your needs to an IUL, see How to Choose an IUL Policy for Retirement Income. The guide walks you through the same worksheet we just described.

Bottom line: precise numbers give you use when you compare policies later.

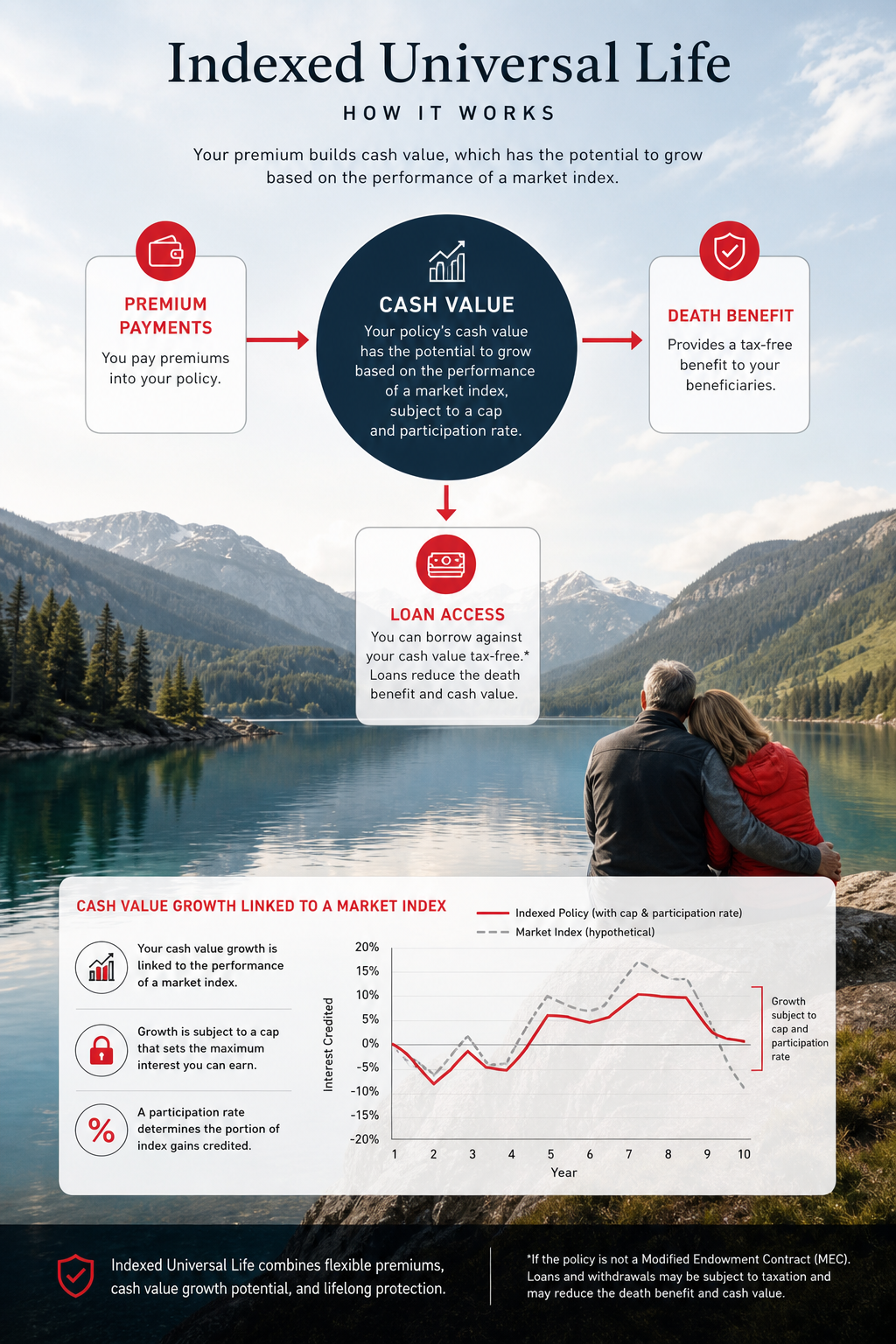

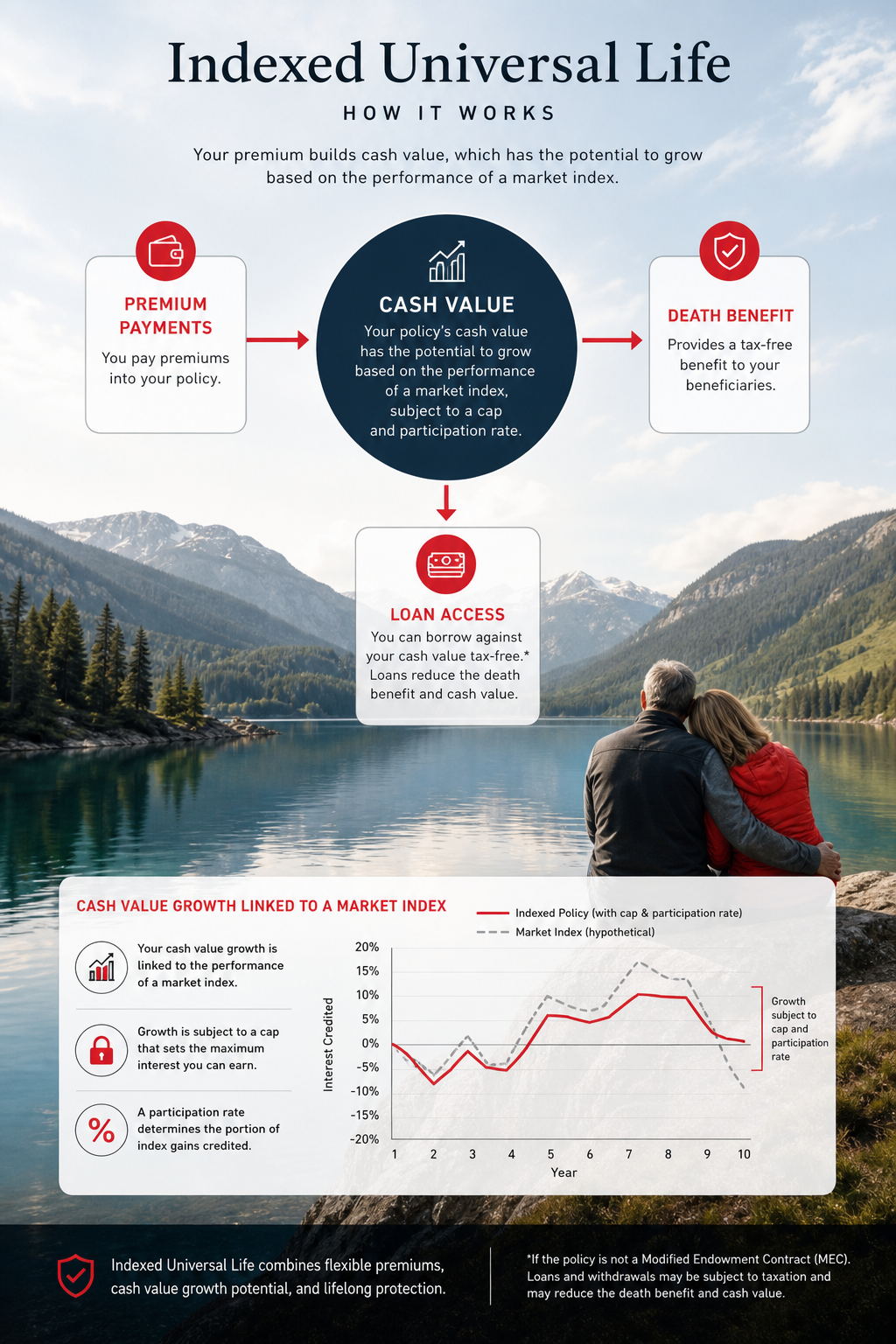

Step 2: Understand How IUL Policies Generate Tax‑Free Income

Unlike a traditional 401(k) or Roth IRA, an IUL builds cash value inside a life‑insurance wrapper. The cash grows based on a stock‑market index , usually the S&P 500 , but you never own the stocks. The policy credits interest using a participation rate, a cap, and a floor (often 0%).

Because the cash sits inside a life‑insurance contract, the IRS treats the growth as tax‑deferred under Section 7702. You don’t pay income tax each year the cash rises.

When you need money, you take a policy loan or a partial withdrawal. A loan isn’t counted as taxable income as long as the policy stays in force. That’s why many retirees call it “tax‑free retirement income.”

According to the IRS tax topic 401, loans against life‑insurance cash value are not taxable if the policy remains active.

Here’s a quick view of the mechanics:

Understanding these numbers lets you estimate how much cash you’ll have to borrow against in retirement.

Keep in mind that the growth is not truly tax‑deferred if the carrier mislabels the product. Always ask for the illustration and confirm the IRS‑approved 7702 status.

Step 3: Choose the Right IUL Policy Features for Retirement

Feature selection is where most retirees go wrong. The market offers many riders, premium options, and index choices. Pick only what aligns with your retirement goals.

First, decide on the death benefit size. A lower death benefit reduces the cost of insurance (COI) and lets more of your premium go toward cash value. For most retirees, a coverage amount that equals the mortgage balance plus any legacy goal works well.

Second, evaluate living‑benefit riders. These riders let you access part of the death benefit early if you face a chronic, critical, or terminal illness. The research shows that 73% of top‑rated IULs list “None” for living‑benefit riders. Life Care Benefit Services includes a clear rider option, making it a standout choice.

Third, compare index options and caps. A higher participation rate (80‑100%) with a modest cap (9‑12%) often yields better long‑term growth than a low participation rate with a high cap.

Here’s a short checklist:

- Death benefit amount that matches your legacy plan.

- Living‑benefit rider that covers chronic or critical illness.

- Participation rate ≥ 80% and cap around 10%.

- Flexible premium schedule you can afford.

Watch this short video for a visual walk‑through of the rider selection process:

After you pick the features, request an illustration from the carrier. The illustration should show projected cash value at age 65, loan interest rates, and the impact of the chosen riders.

Remember, a policy without a living‑benefit rider may leave you without a safety net if health issues arise.

That wraps up the feature‑selection step.

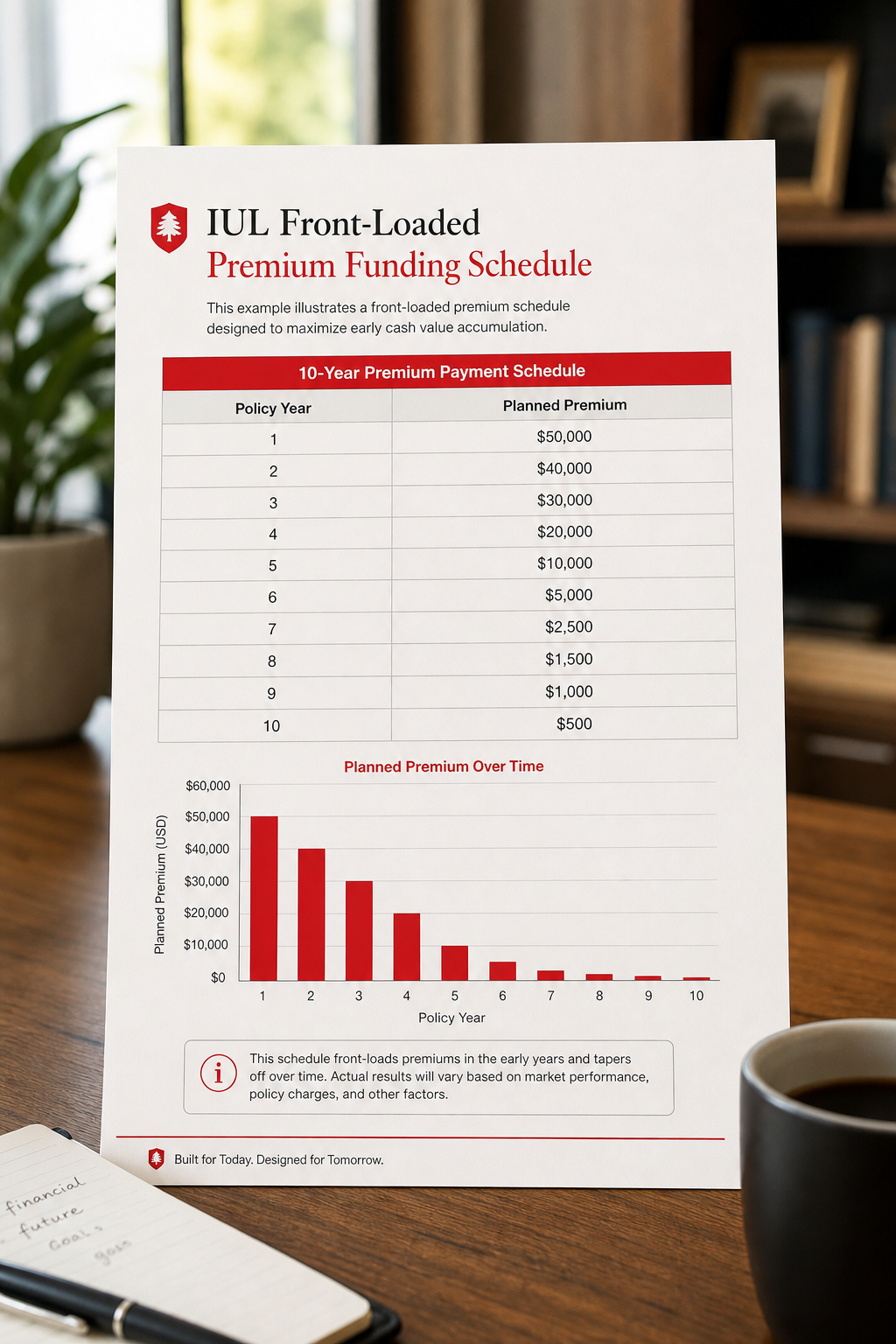

Step 4: Fund Your IUL Policy Strategically for Maximum Tax Benefits

Funding strategy determines how much cash you’ll have to borrow in retirement. The goal is to front‑load premiums during your high‑earning years, then let the cash grow tax‑deferred.

Start by calculating the minimum premium needed to keep the policy in force. Then add an extra amount , often called “over‑funding” , for the first 5‑10 years. This creates a larger cash cushion early on, which compounds over time.

Be aware of the Modified Endowment Contract (MEC) rules. If you fund too much too quickly, the policy can become a MEC, and loans may lose their tax‑free status. The IRS defines a MEC in Publication 770. Stay under the 7‑pay limit to avoid it.

Here’s a usable funding timeline:

- Year 1‑3: Pay 150% of the minimum premium.

- Year 4‑7: Reduce to 120% as cash value builds.

- Year 8‑10: Drop to the minimum premium, let cash grow.

Adjust the amounts based on your cash flow and tax bracket. If you’re still working part‑time, you can keep the higher funding longer.

Pro tip: Set up automatic premium payments. Missing a payment can cause the policy to lapse, which would trigger a taxable event.

Once the cash value reaches a healthy level (often $100k‑$150k for a single retiree), you can start planning loan withdrawals.

That concludes the funding step.

Step 5: Monitor and Adjust Your IUL Strategy in Retirement

Even the best‑designed IUL needs regular check‑ups. Treat it like a personal bank you run a quarterly review on.

First, track the loan‑to‑value (LTV) ratio. Keep it below 80% to avoid a taxable event. If you borrow too much, the policy could lapse and the loan becomes taxable.

Second, watch the cost of insurance (COI) as you age. COI rises with age, so you may need to increase premiums or reduce loans to keep the policy healthy.

Third, re‑evaluate your living‑benefit rider each year. Some riders have waiting periods or caps that change with policy age.

Use this simple quarterly checklist:

- Review policy statements for cash value and loan balance.

- Confirm LTV is under 80%.

- Check COI charges and adjust premium if needed.

- Verify rider eligibility and trigger events.

- Discuss any changes with your independent insurance agent.

Speaking of agents, retirees often benefit from working with an independent insurance agent. They can compare carriers, explain rider nuances, and help you keep the policy on track without bias.

If market conditions shift, you might switch the index allocation within the policy (if allowed). Moving from a high‑volatility index to a more stable one can protect cash value during downturns.

Finally, integrate the IUL into your broader estate plan. The death benefit can provide a tax‑free inheritance, complementing other assets.

Bottom line: Ongoing monitoring turns a static policy into a dynamic retirement tool.

Frequently Asked Questions

What makes an IUL different from a traditional whole life policy?

An IUL ties cash‑value growth to a market index, offering upside potential with a floor that protects against losses. Whole life uses a fixed interest rate and typically has lower growth. The index link can generate more cash for loans, but you must manage caps and participation rates.

Can I withdraw cash from an IUL without paying taxes?

Yes, if you take a policy loan or a partial withdrawal up to your cost‑basis, the amount isn’t considered taxable income as long as the policy stays in force. This is why retirees use IUL loans to supplement Social Security without triggering a tax bill.

Do I need a living‑benefit rider to get tax‑free access?

No, the rider isn’t required for tax‑free loans. However, a rider can provide a lump‑sum payout for chronic or critical illness, giving you extra liquidity without borrowing.

How does the MEC rule affect my IUL?

If the policy becomes a Modified Endowment Contract, loans lose their tax‑free status and are taxed as ordinary income. Stay under the 7‑pay limit and monitor cumulative premiums to avoid MEC classification.

What happens if I miss a premium payment?

Missing a payment can cause the policy to lapse, which would make any outstanding loans taxable and end the death benefit. Many carriers offer a grace period; use automatic payments to stay safe.

Is the cash value guaranteed?

The cash value isn’t guaranteed; it depends on index performance, caps, and participation rates. However, the floor (often 0%) ensures you won’t lose cash value due to market drops.

Can I use an IUL to fund long‑term care?

Yes, if the policy includes a long‑term‑care rider or you take a loan against the cash value. The funds can pay for qualified care expenses without being taxed.

How does an IUL fit into my estate plan?

The death benefit passes tax‑free to beneficiaries, bypassing probate. This can be a powerful legacy tool, especially when combined with other tax‑advantaged accounts.

Conclusion

Using an IUL policy for retirees with tax benefits is a multi‑step process. First, you map out your income gap and tax picture. Then you learn how the policy builds cash value and how loans stay tax‑free. Next you pick the right riders and index features, fund the policy wisely, and finally you monitor the loan balance, COI, and rider status each year.

Because most publicly listed IULs fall short on tax‑deferred growth and living benefits, choosing a transparent carrier like Life Care Benefit Services gives you a clear view of costs and features. Their policy includes the riders many competitors lack, letting you protect your health and your legacy.

If you’re ready to add a tax‑free income stream to your retirement plan, start with a personal review of your cash‑flow needs, then schedule a consultation with a licensed advisor who can pull a side‑by‑side illustration.

Take the first step today , the sooner you fund the policy, the more you can grow tax‑free for a comfortable retirement.