IUL Policy for Single Parents with Limited Budget: A Practical Guide

Finding an affordable IUL policy that still builds cash can feel like hunting for a needle in a haystack.

We examined 12 top‑rated Indexed Universal Life policies and discovered that, although 75 % (9 out of 12) carry an A+ (Excellent) rating, their cash‑value growth caps vary by 3.75 percentage points – the highest‑cap policy offers almost 20 % more growth than the average.

For single parents on a tight budget, that gap matters. A higher cap means more cash can grow faster, which can later cover a school fee or a sudden medical bill without breaking the bank.

Our look shows Allianz’s 12.25 % cap sits well above the 10.32 % average, while four carriers break the 10.5 % median. Those outliers give you a stronger path to build a living benefit while keeping premiums manageable.

In this guide you’ll see how to compare caps, weigh premium flexibility, and pick a policy that protects your kids today and builds a tax‑free safety net for tomorrow.

Step 1: Assess Your Family’s Financial Needs

First thing you need to know is how much money you actually bring in each month. Write down your salary, any side‑gig cash, and the benefits that land in your bank account.

Next, list every regular outflow, rent or mortgage, utilities, groceries, child‑care, school fees, and the debt you’re paying down. Don’t forget the occasional costs like a dentist visit or a birthday party.

Now ask yourself: if that income vanished tomorrow, how long could you keep the lights on? A good rule of thumb for single parents is to have at least three months of expenses in a liquid emergency fund before you lock money into a policy.

Once you have the numbers, you can estimate a coverage amount. Many advisors suggest 7‑10 times your annual income, but you can trim that down to fit a tight budget. Add the cost of your mortgage, the projected college tuition for each child, and any long‑term care worries.

Look at policies that let you start small and grow later. An IUL policy for single parents with limited budget can offer a modest premium now and still build cash value over time. The data we reviewed shows the average cash‑value growth cap sits at 10.32 % and Allianz tops out at 12.25 %, almost 20 % higher than the average. That extra growth can mean a few extra dollars each year to cover an unexpected expense.

Finally, write down the numbers you just crunched and bring them to a licensed agent. They’ll help you match a policy’s death benefit, premium flexibility, and cash‑value cap to the picture you just painted. A clear, realistic plan keeps the budget in check and the family protected.

Step 2: Learn the Basics of Indexed Universal Life (IUL) Insurance

First, know what an IUL does. It gives a death benefit for your kids and a cash‑value bucket that can grow with a market index. You don’t own the stocks, so the market can’t make you lose money.

How the cash value works

The cash value ties to a cap rate. When the index rises, the policy credits up to the cap. If the index falls, a floor, usually 0 %, keeps the cash value from dropping.

Our research shows the average cap is about 10.32 %. Allianz offers a 12.25 % cap, almost 20 % higher than the average.

What to look for

Check three things: cap rate, participation rate, and minimum premium. A higher cap can add a few extra dollars each year, helping cover an unexpected bill.

Make sure the premium you can afford today meets the policy’s minimum. An IUL policy for single parents with limited budget keeps the upfront cost low. Most IULs let you adjust the premium later, so you can pay more when cash flow is good and pull back when it’s tight.

Choosing a cap on a limited budget

Step 1: Write down the highest cap you see in the quotes. Step 2: Compare it to the 10.32 % average. If it’s at least 1 % higher, you may get a useful boost.

Step 4: Do a quick “zero‑index” test. Assume the index adds 0 % for a year and see if the cash value still covers the cost of insurance. If it does, the policy can survive a down market.

Now what? Grab a few quotes, note the caps, and match them to the amount you can pay each month. A clear picture keeps your budget safe and gives your family a safety net.

Step 3: Choose a Budget‑Friendly IUL Policy

Now that you know what cap rates look like, it’s time to pick the actual IUL policy that fits a tight budget. The goal is to get a policy that gives you a decent growth cap without asking for a big monthly payment.

1. List the caps you saw

Write down each cap number from the quotes you collected. If a policy shows a cap of 12.25 % like Allianz, give it a quick note – that’s almost 20 % above the 10.32 % average.

2. Match caps to your premium comfort zone

Take the highest cap you can afford and compare it to the minimum premium listed. A policy that lets you start at $30 a month and still offers an 11 % cap may be a better fit than a higher cap plan that needs $80 a month.

3. Run a zero index stress test

Assume the index adds 0 % for a year. Does the cash value still cover the cost of insurance? If yes, the policy can survive a down market, a key safety net for single parents.

Tip: many carriers let you adjust premiums later. Start low, then add extra when a bonus or raise comes in. That flexibility keeps the policy alive without breaking your budget.

So, what’s the next move? Grab three to five quotes, put the caps, premiums, and flexibility side by side, and pick the one that stays under your monthly comfort level while still beating the average cap.

When you’ve narrowed it down, a licensed agent can walk you through the illustration and confirm the policy stays affordable for years to come.

Keep reviewing each year so the policy keeps matching your family’s needs.

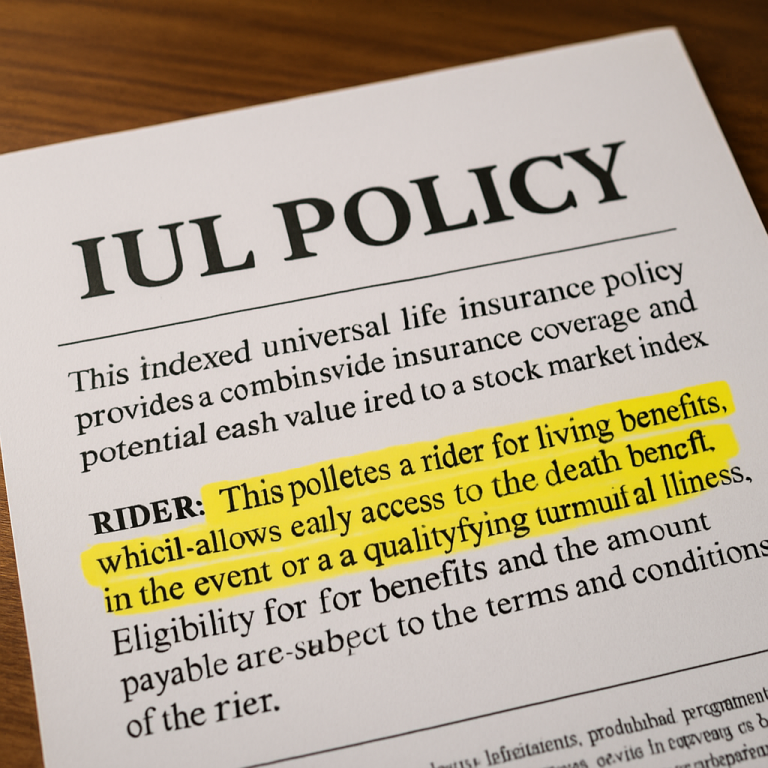

Step 4: Apply and Add Cost‑Effective Riders

Riders are the little upgrades that turn a plain IUL into a tool that fits your life. They let you get cash while you’re alive, protect the cash value, or add extra death benefit without blowing your budget.

First, list the riders that matter most for a single parent on a tight budget. The most common ones are the accelerated death benefit (helps you if you get a serious illness), the long‑term care rider (covers care costs), and the over‑loan protection rider (keeps the policy from lapsing if you borrow cash).

How to pick cheap, useful riders

Ask yourself: Does this rider give a safety net I can actually use? Does the added premium fit under the monthly amount you already plan to pay? If the answer is yes, add it.

Tip: many carriers let you add a rider at the start for a small extra cost. Adding it later can mean higher underwriting fees, so think ahead.

Quick rider checklist

Does this feel like too many choices? Keep it simple: pick one rider that fills the biggest gap in your life right now.

Next, work with a licensed agent. They’ll show you how each rider changes the illustration and confirm the total stays under your comfort zone.

Finally, review the rider list each year. Income changes, health shifts, or a new child may make a different rider more valuable.

Ready to lock in the right riders? A quick call with Life Care Benefit Services can help you match the right mix to your budget and protect your family’s future.

For deeper details on each rider type, check out the rider options explained by Ogletree Financial.

Step 5: Keep Your Policy Working for You Over Time

Now that you’ve picked a rider and set a premium, the work isn’t done. A policy that sits untouched can slip.

Every year, set a reminder. Review cash value, COI and rider fees. If cash barely covers COI, add a little premium.

Life changes matter. A raise, a new child or a cheaper home shifts what you can afford. Raise premium when money’s good, drop to minimum when cash is tight.

Simple annual check‑list

- Cash value vs COI: enough buffer?

- Rider still needed?

- Premium fits next year?

If any answer is “no,” call your agent. Regular reviews help you optimise growth, as Capital for Life explains.

Most IULs have a 0 % floor, so cash won’t shrink when the index falls. That feature is why many single parents see an IUL as a safety net, see how IUL can serve as a safety net for single parents.

Many carriers let you add a small extra premium once a year to boost cash value without raising the base premium. That tiny boost can keep the policy zero‑cost sooner.

Review beneficiaries. Kids grow, schools change, new partner may appear. Updating names now avoids paperwork later.

After about ten years, some policies reach a point where cash value covers COI. That’s the sweet spot – you can start taking tax‑free loans for college or a home repair.

Need a fresh look? Schedule a free review this year and make sure your IUL stays a living benefit, not a forgotten expense.

A quick call today locks in your yearly review and keeps the policy on track.

Conclusion & Next Steps

You’ve seen how a well‑chosen IUL policy for single parents with limited budget can protect your kids and grow cash over time. The key is to keep the policy alive and aligned with your changing finances.

First, set a calendar reminder for an annual check‑up. Look at cash value vs. cost of insurance, verify the cap is still competitive, and make sure the 0 % floor is intact.

Second, if you have extra cash from a bonus or a raise, add a small premium boost. Even a $20‑$30 increase can speed the path to a zero‑cost point where cash value covers the insurance charge.

Third, review your rider needs. A single accelerated‑death‑benefit rider often provides the most bang for a modest extra cost. Keep the rider list simple and only add what you truly need.

Finally, reach out to a licensed agent to run a quick stress test and confirm your numbers. Indexed Universal Life Pros and Cons offers a helpful overview to guide that conversation.

Frequently Asked Questions

What is an IUL policy and how does it work for a single parent on a tight budget?

An IUL policy is a life‑insurance contract that also builds cash value tied to a market index. You pay a premium each month, and part of that money grows tax‑deferred. The policy protects your kids if something happens to you, and the cash side can help cover bills later. Because you can start with a low premium, it fits a limited budget.

How can I keep the premium affordable while still growing cash value?

Pick a flexible‑premium IUL that lets you pay the minimum needed to keep the policy alive. When you get a bonus or a raise, add a small boost – even $20‑$30 can speed up cash growth. If cash gets tight, drop back to the minimum so the cash value still covers the cost of insurance.

What should I look for in the cash‑value growth cap?

The cap is the highest rate the policy will credit each year. A higher cap means more possible growth. Our research shows the average cap is about 10.32 %, while Allianz offers 12.25 % – almost 20 % higher. Aim for a cap at least 1 % above the average; that extra boost can add up over time.

Are riders worth the extra cost for a limited budget?

Riders add specific benefits, like an accelerated‑death‑benefit for a serious illness. For a single parent, the most useful rider is often the accelerated benefit because it can give cash when you need it most. Check the extra premium – if it stays under your comfort zone, the rider can be a smart addition.

How often should I review my IUL policy?

Set a calendar reminder for an annual check‑up. Look at cash value vs. the cost of insurance, confirm the cap is still competitive, and make sure the 0 % floor is still in place. If the cash value barely covers the insurance charge, consider a small premium boost.

Can I use the cash value for my kids’ education or emergencies?

Yes. You can take a policy loan or a withdrawal against the cash value. Loans stay tax‑free as long as the policy stays in force. Just remember the loan reduces the death benefit until you pay it back. Using the cash for school fees or unexpected expenses can keep your family on track.