IUL Cash Value Withdrawal Rules for Retirees: 18 Strategies

Ever wonder if you can actually pull money out of your IUL without blowing up your death benefit or getting hit with a surprise tax bill? You’re not alone. Many retirees assume all Indexed Universal Life policies come with steep early-withdrawal fees. But that’s not always true. The IUL product from Life Care Benefit Services, for example, doesn’t even list a surrender-charge period. That’s a big deal for retirees who need flexible access to their cash value. In this article, we break down the exact rules that apply once you’re retired. You’ll learn the smartest ways to turn that cash value into tax-free income. We cover withdrawals, loans, tax rules, and how to avoid costly mistakes. Let’s cut through the jargon and get to what matters.

1. Tax-Free Basis Withdrawals , Understand Your Cost Basis

When you put money into an IUL, those premiums create your cost basis. That’s the total amount you’ve paid in. You can withdraw up to that amount tax-free. The IRS calls this a return of your basis. Anything above that is a gain and gets taxed as ordinary income. So the first rule is: know your cost basis. Keep track of every premium payment. That number is your safe withdrawal limit. Withdraw only up to that if you want to avoid taxes. For example, if you paid $100,000 in premiums over the years, you can take out $100,000 tax-free. After that, the IRS wants its share. This is a huge advantage over 401(k)s where every withdrawal is taxable. But don’t forget: withdrawals reduce your cash value and death benefit. So use this strategy sparingly. Only take what you really need. And always check with a tax advisor before making big moves. The cash value grows tax-deferred, so you’re not paying taxes on growth until you take it out. That’s the trade-off. For retirees, this rule is a major change. You can supplement Social Security with tax-free money. Just be smart about how much you take.

2. Policy Loans (Fixed Rate) , Predictable Access to Cash

Policy loans are another way to tap your cash value. With a fixed-rate loan, the insurance company charges you a set interest rate. Often that rate is around 2% to 5%. The key is that some policies offer a “zero-wash” loan. That means the money you borrow still earns interest inside the policy at the same rate. So the loan cost is neutral. You’re basically paying yourself interest. That’s why many experts call it tax-free income. The loan itself is not taxable because it’s not a withdrawal. As long as the policy stays in force, you never pay taxes on that money. But there are risks. If the policy lapses with an unpaid loan, the IRS treats the loan balance as income. That could be a huge tax bill. So you need to keep the policy active. Fixed-rate loans give you predictable costs. You know exactly what you’ll pay. That’s helpful for budgeting in retirement. Many retirees use fixed-rate loans for big expenses like medical bills or home repairs. Just make sure you understand the terms before you borrow. Some policies have lower credited rates on the borrowed amount. That means you lose a little growth. But it’s still a solid option for tax-free access.

3. Policy Loans (Variable Rate) , Flexibility with Rate Caps

Variable-rate loans work differently. The interest rate floats but has a cap. For example, the loan might charge you up to 5% variable. But while your money is loaned out, it still gets credited based on the index. So if the index goes up 10%, you earn 10% on the borrowed amount. You pay 5% in loan interest, so you net 5% on money you already spent. That’s powerful. But there’s a downside. If the index goes down, you earn 0%, but you still pay the loan interest. That can eat into your cash value. So variable loans work best when markets are rising. They give you flexibility. You can take larger loans without worrying about the interest rate being too high. The cap protects you from runaway rates. Many companies set the cap around 5% to 8%. For retirees who want to maximize growth while borrowing, variable loans can be smart. But you need to monitor the market. If you expect a downturn, consider using fixed-rate loans instead. The choice depends on your risk tolerance and market outlook. Some experts prefer variable loans because they can boost returns. Others like the certainty of fixed. Talk to your agent about which option your policy offers.

4. Partial Surrender , Tapping Cash Without Full Exit

A partial surrender means you take a permanent withdrawal from your policy. You don’t borrow. You just take cash out. The amount you withdraw reduces both your cash value and death benefit. The tax treatment follows the FIFO rule (first in, first out), which we’ll cover later. But here’s the key: a partial surrender is like a permanent cash-out. You don’t have to pay it back. That can be useful for one-time expenses. But it also reduces the growth potential of your policy. Every dollar you take out stops growing. Over time, that can add up. So only use partial surrenders for small amounts. A good rule of thumb is to keep them under your cost basis to avoid taxes. If you take more than your basis, the excess is taxable. Also, some policies have surrender charges in the early years. Those can eat into your cash. So check your contract. The Western & Southern tax guide explains that withdrawals from cash value life insurance are generally tax-friendly as long as you follow the rules. For retirees, partial surrenders can be a quick way to get cash without loan interest. But they permanently shrink your coverage. Weigh that against the benefits.

5. Full Surrender , Complete Cash-Out and Tax Consequences

Full surrender means you cancel the policy entirely. You get the cash surrender value, which is the cash value minus any surrender charges. That lump sum is taxable if it exceeds your cost basis. The gain is taxed as ordinary income. And you lose the death benefit forever. So this is usually a last resort. For retirees, a full surrender might make sense if you no longer need life insurance and the cash value is large. But think about it carefully. If you surrender, you lose the tax-free growth potential and the death benefit protection. Also, if you have outstanding policy loans, those become taxable when the policy lapses. That can create a nasty surprise. The IRS treats the loan balance as income. So before you surrender, consider if you can take smaller withdrawals or loans instead. Some people sell their policy in a life settlement, which might get more than the surrender value. But that’s a different topic. The bottom line: full surrender should be your last option. It has permanent consequences. Make sure you understand all the tax implications before you sign anything.

6. FIFO Rule , How Withdrawals Are Taxed

The IRS uses the FIFO method for life insurance withdrawals. FIFO stands for First In, First Out. That means your withdrawals are considered a return of your premiums first. Only after you’ve taken out all your premiums do you start tapping into gains. That’s why you can take out your cost basis tax-free. The gains come out last. So the order matters. For example, if you have $100,000 in premiums and $50,000 in gains, the first $100,000 you withdraw is tax-free. The next $50,000 is taxable. This is different from annuities, which use LIFO (last in, first out). With annuities, gains come out first, so they’re taxable sooner. FIFO is a big advantage for IULs. It lets you access your own money tax-free up to the amount you paid in. That’s why many retirees use IUL cash value for income. As explained by Insurance Geek, withdrawals are FIFO for tax purposes. This rule is important for planning. If you need regular income, take withdrawals up to your basis first. Then switch to policy loans for the rest. That way you minimize taxes. Just keep good records of your premium payments. Without them, you can’t prove your cost basis.

7. 7-Pay Rule , Early-Year Withdrawal Limits

The 7-pay rule comes from IRS Section 7702. It limits how much premium you can pay in the first seven years without turning your policy into a Modified Endowment Contract (MEC). A MEC loses many tax advantages. Withdrawals and loans from a MEC are taxed like an annuity: gains come out first. That’s bad. So you need to avoid hitting the 7-pay limit. The rule calculates a maximum annual premium based on the death benefit. If you exceed that in any of the first seven years, the policy becomes a MEC. Once a MEC, always a MEC. You can’t fix it. That means your cash value withdrawal rules change dramatically. For retirees, this is important if you’re still funding your policy. If you’re already past the seven years, you’re safe. But if you’re adding money in early retirement, watch the limits. The insurance company’s illustration should show the MEC limit. Never exceed it. Some agents push overfunding to build cash value faster, but that can trigger MEC status. Stick to the safe zone. If you inherit a policy that might be a MEC, consult a tax professional. The 7-pay rule is complex, but understanding it can save you from losing tax-free access.

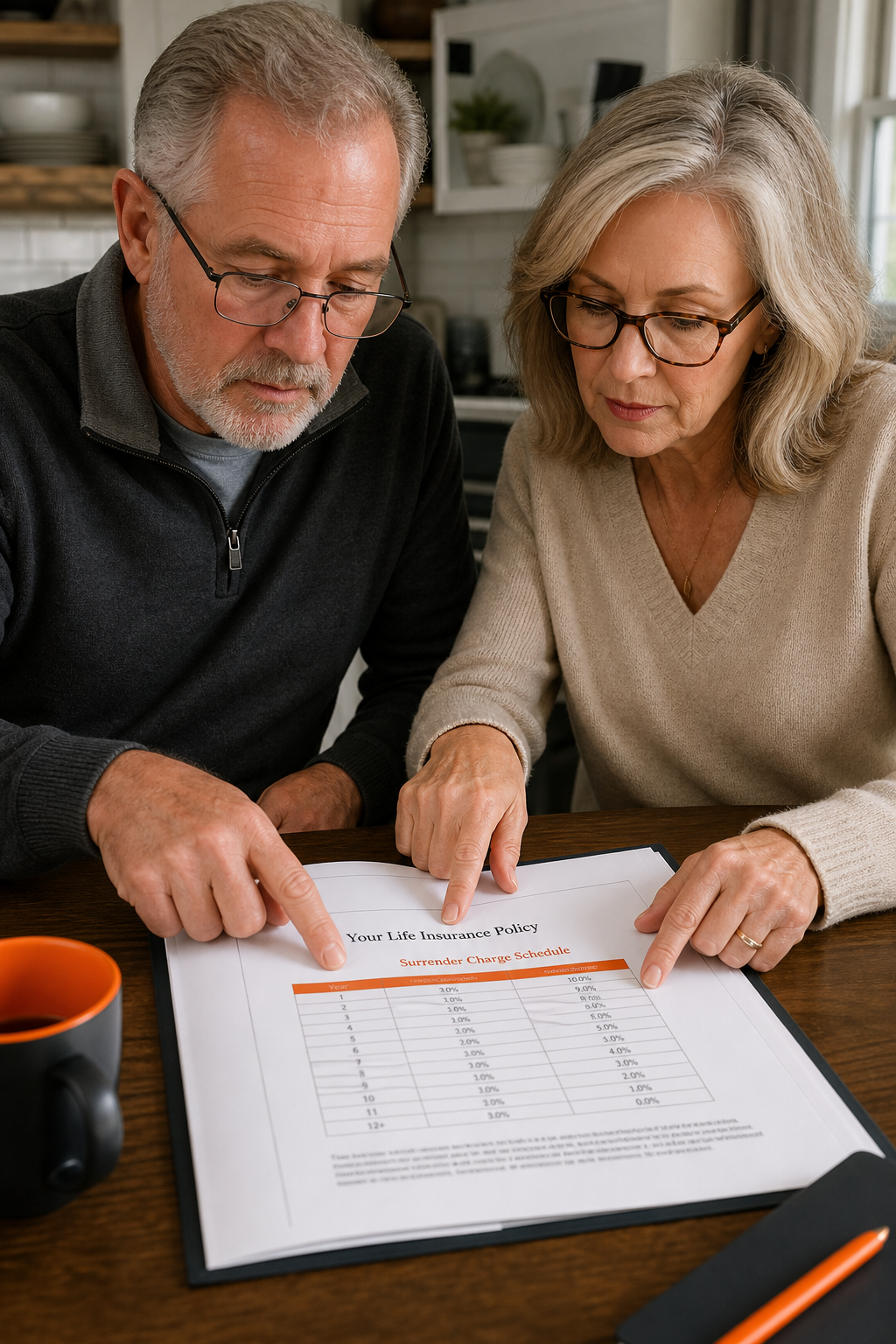

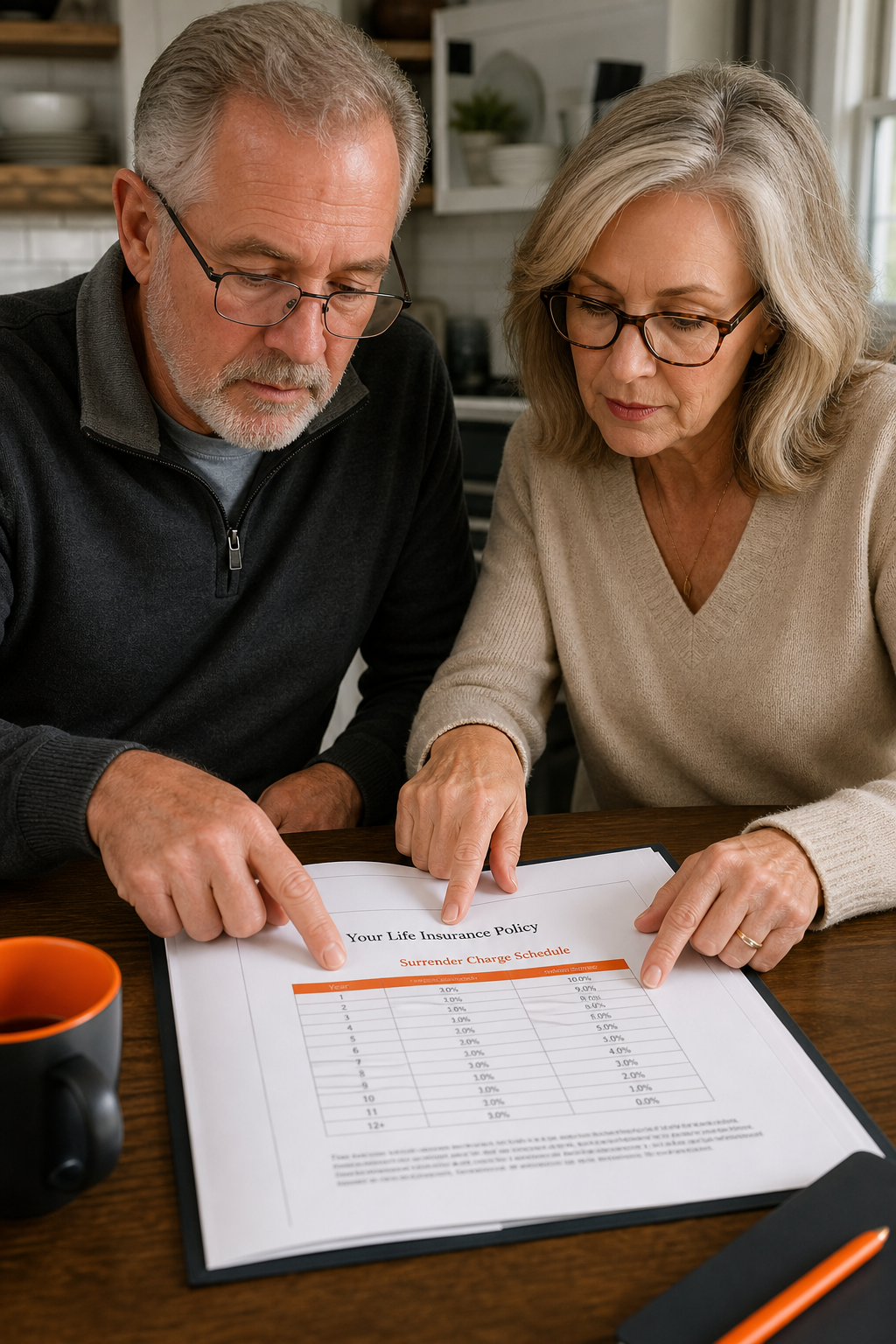

8. State Surrender Charge Schedules , Know Your Policy Year

Surrender charges are fees the insurance company takes if you withdraw too much or cancel early. These charges decline over time. Typically, they last 10 to 15 years. For example, the Foundations Indexed Universal Life policy has an 11-year surrender charge period. That means if you take a large withdrawal in year 5, you’ll pay a penalty. But the Life Care Benefit Services IUL doesn’t have a surrender charge period. That’s a big difference. Every state has its own regulations, but the surrender charge schedule is set by the insurance company, not the state. However, state law may limit how steep the charges can be. For retirees, the key is to know where you are in that schedule. If you’re still in the surrender charge period, think twice before taking big withdrawals. They can eat up a big chunk of your cash. Check your policy contract for the surrender charge table. It will show the percentage by year. For example, year 1 might be 10%, year 2 is 9%, etc. After 10-15 years, it drops to zero. That’s when you have full access. If you absolutely need money during the surrender period, consider a policy loan instead. Loans are not subject to surrender charges. Partial surrenders usually are. So prioritize loans until the surrender period ends. This one rule can save you thousands.

9. Age 59½ Rule Does Not Apply , IUL vs 401(k)

With a 401(k) or IRA, you can’t take penalty-free withdrawals until age 59½. That’s a federal rule. But IUL policies have no such age restriction. You can access your cash value at any age. There’s no 10% early withdrawal penalty from the IRS for life insurance withdrawals or loans. That’s a huge difference. For retirees, this means flexibility. If you retire early at 55, you can use your IUL cash value without penalties. Many people use IULs as a bridge to Social Security. You can take tax-free loans or withdrawals to cover expenses until you qualify for Medicare and Social Security. Just be aware that if you take withdrawals above your cost basis, you’ll owe income tax. But no penalty. So if you’re under 59½ and need money, your IUL is a much better option than tapping your 401(k). The 401(k) would hit you with a 10% penalty plus income tax. That’s a big hit. So IULs are great for early retirees. But remember, the policy must be properly structured to have enough cash value. You can’t just buy a small policy and expect huge withdrawals. You need to fund it adequately over time.

10. Step-by-Step Withdrawal Request , Process Overview

How do you actually get the money? The process is simpler than you think. First, log into your policy’s online portal. Most insurance companies have a website where you can see your cash value. Look for a “Withdrawals” or “Loans” section. You’ll need to fill out a form. It asks how much you want and the method (loan or withdrawal). You may need to provide a reason, but that’s rare. Then submit. The company will process it, usually within a few days. They might send a check or direct deposit. Some allow electronic transfers to your bank. Make sure you have the correct paperwork. For larger amounts, you might need a signature guarantee or notarized form. That’s to prevent fraud. The whole process takes about a week. If you’re doing a loan, the interest rate is set. They’ll tell you the terms. Keep a copy for your records. One tip: test the process with a small amount first. That way you know how it works before you need a big sum. Also, check if your policy has any fees. Some companies charge a small processing fee, like $50. That’s rare but possible. The Foundations IUL charges a $50 withdrawal fee, so be aware. If you’re with Life Care Benefit Services, there may be no fee. So the process is straightforward. Just follow the steps.

11. Cost Comparison: Withdrawals vs Loans , Interest Caps and Risks

Choosing between withdrawals and loans depends on your goals. Here’s a side-by-side comparison:

The right choice depends on your situation. Withdrawals are simpler but reduce your coverage. Loans preserve more growth but require you to think about interest. Many retirees use a combination: take withdrawals up to the basis first, then use loans for the rest. That minimizes taxes and keeps the policy healthy. Always run the numbers. If you expect high market returns, a variable loan might let you benefit. If you want certainty, a fixed loan or withdrawal is safer. The Policy Shop notes that policy loans are generally tax-free if the policy stays in force. That’s a key advantage. But remember, if the policy lapses, the loan becomes taxable. So manage your cash value carefully.

12. Operational Case Study , Retirement Income Scenario

Let’s make this concrete. Imagine a 65-year-old retiree named Susan. She has an IUL policy with $300,000 in cash value. Her cost basis is $200,000. She wants $20,000 per year in retirement income for 10 years. Option A: Take $20,000 per year as a withdrawal. For the first 10 years, she takes $200,000 total, which is exactly her basis. That’s tax-free. But after 10 years, her cash value is about $100,000 left (assuming no growth). She also lost death benefit protection. Option B: Use policy loans. She takes a $20,000 loan each year. The loan is tax-free. Her cash value continues to earn interest on the loaned amount (if variable). She pays loan interest, but if the index does well, she nets a positive spread. After 10 years, she has a loan balance of $200,000 plus interest. That reduces her death benefit. She can choose not to repay, but the debt will be subtracted from the death benefit. Which is better? Option A gives certainty but reduces the policy. Option B gives potential growth but adds risk. Most retirees mix both. Susan might take $10,000 withdrawal (tax-free from basis) and $10,000 loan each year. That way she stretches her basis further and keeps more cash value working. This case study shows why you need a personalized strategy. There’s no one-size-fits-all.

13. Policy Expenses and Fee Erosion , Impact on Withdrawable Cash

Every IUL policy has expenses. These include cost of insurance (COI), administrative fees, and rider charges. These costs eat into your cash value every month. Over time, they can significantly reduce how much you can withdraw. For example, if your policy has high COI charges, your cash value may grow slower than expected. That means less available for withdrawals. That’s why it’s important to choose a policy with low expenses. The Life Care Benefit Services IUL, according to research, does not disclose a surrender charge period, which suggests flexible terms. But expenses still apply. You need to look at the policy illustration. It shows the projected cash value under different interest rates. Pay attention to the guaranteed column. That shows the worst-case scenario. If expenses are high, the guaranteed cash value might be very low. For retirees, that’s a red flag. You want a policy where the cash value grows enough to support your income needs. Some policies have a no-lapse guarantee rider, which keeps the policy in force even if cash value drops. That can be valuable. But it adds cost. Balance your need for low expenses with adequate protection. A good agent can show you how expenses change over time. Generally, expenses are higher in the early years and level off later. So if you’re already retired, the heavy front-end costs are behind you. But still, review your annual statement to see how much is going to fees.

14. Coordination with Social Security , Tax Implications

Social Security benefits can be taxed if your provisional income exceeds certain thresholds. Provisional income includes adjusted gross income plus half of Social Security benefits. If you take large IUL withdrawals, they increase your AGI. That could push you into a higher bracket and cause up to 85% of your Social Security to become taxable. Policy loans, on the other hand, are not counted as income when you take them. They don’t impact your provisional income. That’s a strategic advantage. So if you want to minimize taxes on Social Security, use policy loans instead of withdrawals. For example, if you need $30,000 per year, take it as a loan. Your AGI stays low, and your Social Security remains mostly tax-free. If you take a withdrawal, $30,000 adds to your AGI. That could trigger the tax on Social Security. This coordination is a key reason why IULs are popular for retirement. They give you control over your tax bracket. Just be careful: loans reduce your death benefit, and if the policy lapses, the loan becomes taxable. But if you manage it well, it’s a powerful tool. Talk to a tax professional about your specific numbers.

15. Medicare Premium Impact , IRMAA Considerations

Medicare Part B and Part D premiums are income-based. If your modified adjusted gross income is above a certain threshold, you pay an Income-Related Monthly Adjustment Amount (IRMAA). IRMAA can significantly increase your Medicare costs. For 2026, the thresholds are indexed. IUL withdrawals count as income and could push you over the IRMAA limit. Policy loans do not count as income. So again, loans give you a way to access cash without raising your Medicare premiums. This is especially important for retirees who are near the IRMAA cliffs. For example, an IRMAA surcharge can easily be $100, $200 per month per person. That’s thousands per year. If a large IUL withdrawal triggers IRMAA, it could cost you more than the tax on the withdrawal itself. So the smarter move is to use loans for income until you die or until your income is lower. Some people also withdraw up to their basis in years when their income is low, then switch to loans later. That avoids IRMAA and taxes. Plan your withdrawals with Medicare in mind. Your agent or tax advisor can help you model different scenarios.

16. Preventing Policy Lapse , Strategies for Regular Withdrawals

If you take regular withdrawals or loans, you need to make sure the policy doesn’t lapse. A lapse means you lose coverage and the IRS may tax any outstanding loan balance. To prevent that, monitor your policy’s cash value. Never let loans exceed a certain percentage of the cash value. A common rule is to keep loans under 90% of cash value. Also, pay attention to the cost of insurance. As you age, COI increases. If your cash value is shrinking due to withdrawals, it might not cover COI. That can cause the policy to lapse. Consider using a no-lapse guarantee rider if available. It adds a cost but ensures the policy stays in force even if cash value drops to zero. Another strategy is to keep some cash value untouched as a buffer. Or pay some premiums out of pocket to keep the policy healthy. The key is to review your policy annually. Check the projected crediting rates and expenses. If the policy is underperforming, you might need to reduce your withdrawals. Some people use a dynamic strategy: in years when the index performs well, they take larger withdrawals; in bad years, they take less. That helps preserve the policy. Life Care Benefit Services can help you set up a sustainable withdrawal plan. The goal is to never trigger a lapse.

17. Death Benefit Reduction , Understanding the Trade-Off

Every dollar you withdraw or borrow reduces the death benefit your beneficiaries will receive. With a withdrawal, the reduction is direct. With a loan, the reduction equals the loan balance plus accrued interest. So using your cash value always comes at a cost to your heirs. That’s the trade-off. You get to enjoy the money now, but your loved ones get less later. Sometimes that’s acceptable. If you need the money to live, it’s worth it. But if you want to leave a legacy, you might want to minimize tapping the cash value. Some policies allow you to carry a loan indefinitely. The death benefit will be reduced by the loan, but the policy stays in force. That can be a good compromise. You get tax-free income, and your heirs still get something. Also, if the policy has a guaranteed minimum death benefit, that might protect part of it. But read the contract. The death benefit reduction is permanent. So think about what matters most: your lifestyle in retirement or the inheritance? Balance accordingly.

18. Withdrawal Limits and Policy Performance , What You Can Safely Take

How much can you safely withdraw without risking the policy? It depends on the cash value growth rate. A common guideline is to withdraw no more than 4% to 6% of the cash value per year. That’s similar to the 4% rule for retirement accounts. But the exact number depends on your policy’s crediting rate, expenses, and your age. If your IUL averages 6% growth, you might be able to withdraw 5% annually and keep the cash value stable. But if expenses are high or growth is lower, you need to withdraw less. The best way to find your safe limit is to use an illustration or calculator. Life Care Benefit Services offers an IUL cash value calculator on their blog to help you project. You can input your premiums, expected growth, and expenses. See how different withdrawal amounts affect the policy over time. Aim for a plan where the cash value never drops below zero. Also, leave a buffer for unexpected expenses or poor market years. The key is to be conservative. It’s better to take a little less than risk a lapse. If you’re unsure, start with a lower withdrawal and increase later as the policy grows. Regular monitoring is essential.

Frequently Asked Questions

Can I withdraw cash value from my IUL tax-free?

Yes, but only up to the amount of premiums you’ve paid (your cost basis). That’s because the IRS treats those withdrawals as a return of your investment. Any amount above your basis is considered a gain and is taxable as ordinary income. Policy loans, however, are generally tax-free as long as the policy remains in force. So most retirees use loans for tax-free income.

What happens if I take a loan from my IUL and never pay it back?

The loan balance plus accrued interest will be deducted from the death benefit. You are not required to repay the loan during your lifetime. However, if the policy lapses with an outstanding loan, the IRS treats the loan amount as taxable income. That can result in a big tax bill. So it’s important to keep the policy in force.

Is there a penalty for withdrawing from an IUL before age 59½?

No. Unlike 401(k)s and IRAs, IULs do not have an early withdrawal penalty. You can access your cash value at any age without incurring the IRS 10% penalty. However, any withdrawals above your cost basis are subject to ordinary income tax. Policy loans are generally tax-free regardless of age.

How does a partial surrender affect my death benefit?

A partial surrender reduces both the cash value and the death benefit by the amount withdrawn. Some policies reduce the death benefit by more than the withdrawal amount, depending on the policy’s corridor test. Check your contract. Withdrawals are permanent, so you cannot add the death benefit back later.

What is the 7-pay rule and why does it matter?

The 7-pay rule is an IRS regulation that limits how much premium you can pay in the first seven years of a life insurance policy. If you exceed that limit, the policy becomes a Modified Endowment Contract (MEC). Once a MEC, withdrawals and loans are taxed less favorably , gains come out first. Avoid exceeding the 7-pay limit.

Can I use an IUL to supplement my Social Security without increasing taxes?

Yes, by using policy loans instead of withdrawals. Loans do not count as income for Social Security tax calculations or for Medicare IRMAA. That means you can access cash without pushing your provisional income higher. This helps you keep more of your Social Security benefits and avoid higher Medicare premiums.

What happens to my IUL cash value when I die?

The cash value generally becomes the property of the insurance company when the insured dies. The death benefit is paid to the beneficiaries. If there are outstanding loans, the loan balance is deducted from the death benefit. The remaining death benefit is paid tax-free to the beneficiaries.

How do I know if my IUL has surrender charges?

Check your policy contract. Look for a table titled “Surrender Charges” or “Cash Surrender Value.” It will show a percentage that declines over time. Some policies, like the one from Life Care Benefit Services, may have no surrender charges. If you’re unsure, ask your agent or call the insurance company. They can tell you the schedule.

Conclusion

We’ve covered 18 strategies for accessing your IUL cash value in retirement. The key takeaways are simple: know your cost basis, choose between withdrawals and loans carefully, and be aware of how your choices affect taxes, Medicare, and your death benefit. Policy loans are the most tax-efficient way to get income, especially if you want to keep Social Security and Medicare costs low. But they come with risks, like policy lapse and loan interest. Withdrawals are simpler but reduce your coverage permanently. The best approach is often a mix. Use withdrawals up to your basis, then switch to loans. Monitor your policy annually to avoid surprises. And always consult a tax professional and a trusted agent. Life Care Benefit Services can help you design a strategy that fits your retirement goals. Remember, the rules are not static. As market conditions and your needs change, adjust your approach. With the right plan, your IUL can be a powerful source of tax-free retirement income.