Living Benefits Life Insurance for Chronic Illness: A Practical How‑To Guide

Living benefits life insurance for chronic illness can be a game changer for families and small business owners facing unexpected health hurdles.

In this guide you’ll learn how the rider works, what to watch for, and practical steps to add it to your plan.

We examined five leading U.S. term life insurers and discovered that every single one uses the identical 90‑day, two‑activity‑of‑daily‑living rule to qualify for chronic‑illness riders—defying expectations of varied standards.

Because the rule is uniform, you can compare riders more easily. A practical next step is to review your current policy’s rider language and ask your agent about adding a chronic‑illness rider if it’s missing. For a deeper dive into how these riders fit into broader coverage, check out Understanding life insurance with chronic illness rider. You can also explore an AI Video Editing Tutorial for a quick look at creating simple promotional videos for your business.

Step 1: Understand Living Benefits and Chronic Illness Coverage

First thing: you can tap your life insurance while you’re still alive if a chronic illness stops you from doing daily tasks.

That’s what we call living benefits life insurance for chronic illness. It turns part of the death benefit into cash you can use now – for medical bills, mortgage payments, or just a breather.

Most carriers use the same rule: you must be unable to do at least two of the six daily living activities for 90 straight days. Those activities include eating, bathing, dressing, using the bathroom, moving, and continence.

Step one is to find the rider language in your policy. Open the contract, look for “chronic illness rider,” “accelerated death benefit,” or “living benefit.” Write down the trigger events and any waiting period.

Imagine a family with two kids and a mortgage. The dad gets diagnosed with a condition that limits his ability to dress and bathe. With the rider, the policy can pay a lump sum that covers the mortgage while the family adjusts.

Or picture a small‑business owner who can’t lift heavy boxes after a back injury. The rider can fund a temporary hire so the shop stays open.

Here’s a quick video that walks through how the rider works.

After you watch, call your agent. Ask them to confirm the 90‑day rule, the cost of the rider, and how the payout would affect your beneficiaries.

For a deeper dive on the types of living benefits that can be added to a policy, see Guardian Life’s overview of living benefits.

To see how a chronic illness rider is defined and what illnesses qualify, check Progressive’s guide to chronic illness riders.

Step 2: Evaluate Policy Types (IUL, Term, Whole) with Living Benefits

Now that you know a rider exists, it’s time to see which kind of policy can hold it.

Not all life plans let you add a living‑benefits rider. The three most common options are Indexed Universal Life (IUL), term life and whole life. Each one works a bit differently, so pick the one that fits your cash flow and long‑term goals.

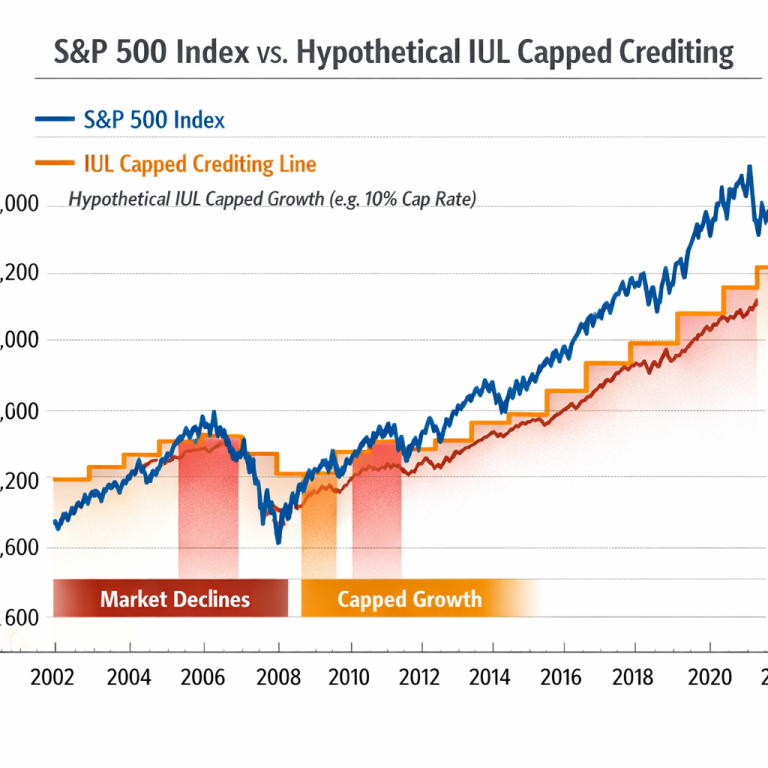

IUL – Flexibility with a cash value cushion

An IUL builds cash value that can grow with a stock index, but the policy never loses money because of a cap. That cash can be borrowed or withdrawn when a chronic‑illness rider triggers.

Because the cash sits inside the policy, you often get tax‑free access to part of the death benefit. F&G’s guide to living benefits shows how a typical IUL rider can cover a 90‑day, two‑activity loss of function rule.

Tip: If you’re a family that wants a safety net and also plans to use the cash for retirement, an IUL may be a good match.

Term life – Simple and cheap, but no cash value

Term policies pay a death benefit only if you die within the chosen years. Some carriers now offer an optional rider that lets you tap a portion of the death benefit early when a chronic illness hits.

The trade‑off is you won’t have a cash‑value account to grow. The payout is usually a fixed amount, and you may lose the benefit if you outlive the term.

Best for: Young parents or small‑business owners who need affordable coverage now and can add a rider for peace of mind.

Whole life – Guaranteed death benefit and steady cash value

Whole life guarantees a death benefit and builds cash value at a set rate. The rider can access that cash once the chronic‑illness trigger is met.

The policy is more expensive, but the cash value grows predictably and can be used for a mortgage payment or a temporary hire.

Best for: Seniors who want a lifelong shield and are comfortable paying higher premiums.

Before you decide, answer these quick checks:

- Can you afford the premium for the whole life or IUL?

- Do you need cash value now, or is low cost more important?

- Does the rider cost fit your budget?

If you’re still unsure, a quick call with a Life Care Benefit Services advisor can help you compare the numbers.

Finally, read the fine print. Western & Southern’s chronic illness rider overview explains common exclusions and waiting periods, so you know exactly when the money will flow.

Pick the policy that lines up with your cash flow, your long‑term plans, and the level of protection you need today.

Step 3: Calculate the Coverage Amount You Need

Start with your real‑life costs

Grab a piece of paper or open a note app. List the biggest bills you’d still have if you couldn’t work – mortgage or rent, utilities, food, and any ongoing medical costs.

For a family of four, that might look like a $200,000 mortgage, $3,600 a month for utilities and groceries, and $1,200 a month for meds.

Turn those numbers into a lump sum

Multiply each monthly cost by the number of months you expect the rider to pay out. Most chronic‑illness riders use the 90‑day rule, but many families plan for a year of support.

Using the example above: ($3,600 + $1,200) × 12 = $57,600. Add the mortgage balance you’d need to keep the roof over your head – $200,000. Total needed: about $257,600.

Factor in what you already own

Do you have savings, a 401(k), or a home‑equity line? Subtract those from the total you just calculated.

If you have $50,000 saved, the gap shrinks to $207,600.

Check the rider cost

Look at your policy’s rider surcharge. Many carriers charge $5‑$20 per month per $10,000 of coverage. A quick calculator can help you see if the premium fits your budget.

Think Bank offers a simple life insurance calculator that lets you plug in the coverage amount and see the monthly cost.

Run a quick sanity check

Ask yourself: If the rider paid out, would the remaining death benefit still protect your loved ones?

Many families find that keeping at least 40% of the original death benefit intact feels safe.

Take action

1. Write down your monthly expenses.

2. Multiply by the months you’d need support.

3. Add any large debts you’d want to clear.

4. Subtract existing assets.

5. Use a calculator to see the premium.

If the number looks high, consider a lower rider percentage or a term policy with a rider – both options are explained in how chronic illness riders work.

Finally, give a trusted adviser a call. A service like Life Care Benefit Services can walk you through the math and match you with a carrier that fits your budget.

Step 4: Compare Providers and Policy Features

You’ve done the math. Now you need a carrier that actually pays when a chronic illness hits.

Match the policy type to your cash flow

If you want a cheap plan, look at term life with a rider. If you like a cash value cushion, an IUL or whole life might fit. Think about how long you plan to keep the policy. A term rider ends with the term; a permanent rider stays as long as you pay.

Know the rider surcharge

Most carriers charge between $5 and $20 each month for every $10,000 of coverage (Living Benefits Comparison Chart). Use a quick calculator to see how that adds to your premium. If the extra cost feels high, you can ask for a lower percentage or a shorter waiting period.

Check the eligibility rule

All five major insurers we looked at require the same trigger: you must be unable to do at least two daily‑living activities for 90 straight days. That uniform rule makes it easier to compare.

Start with a rating check. NerdWallet scores insurers on financial strength, customer service and transparency. A higher score usually means the company will stay around and pay claims when you need them.

Compare key features side by side

When you look at the table, ask yourself: does the cost fit my budget? Does the provider give me easy access to a quote? Does the rider cover the activities I worry about?

One practical step is to pull a quote from each carrier. You can do that on the carrier’s website or with an independent agency. Life Care Benefit Services works with over 50 carriers, so they can pull multiple quotes for you in one call.

Don’t forget the fine print on exclusions. Some riders don’t pay for mental health conditions or injuries from risky sports. Make sure the rider covers the scenarios you fear most.

Finally, read the fine‑print. Look for waiting periods, exclusions, and how the rider affects the death benefit. A clear rider description helps you avoid surprise gaps later.

By lining up cost, trigger, and service quality, you can pick the provider that gives you the most peace of mind for your living benefits life insurance for chronic illness.

Step 5: Apply and Secure Your Policy

Now it’s time to turn the plan into a real safety net.

First, pull together the paperwork you’ll need. Grab a recent doctor’s note, a list of your daily‑living activities, and any existing policy statements. Having these at hand cuts the back‑and‑forth with the carrier.

Next, call a licensed agent. Tell them you want to add a chronic‑illness rider to your living benefits life insurance for chronic illness. Ask for a clear description of the rider’s trigger, waiting period, and how it will affect the death benefit.

Does the agent give you a quote that feels too high? Ask for a breakdown. Many carriers charge $5‑$20 per month for each $10,000 of coverage. Learn more about how living benefits riders are priced. If the cost still worries you, consider lowering the rider percentage or choosing a shorter waiting period.

Once you have the numbers, review the rider language line by line. Look for any exclusions that might bite you later – for example, mental‑health conditions or high‑risk sports are often left out.

Ready to lock it in? Fill out the application, sign the rider endorsement, and keep a copy for your records. Most carriers let you submit the forms online, but a quick phone call can smooth out any last‑minute questions.

After you submit, the insurer will start the underwriting process. If you have a chronic condition, they may ask detailed health questions. Read about underwriting tips for chronic‑illness cases. Be honest and thorough – missing info can delay approval.

Finally, set a reminder to revisit the policy each year. Premiums can change, and you might want to adjust the rider as your family’s needs evolve.

Action checklist:

- Gather medical notes and current policy docs.

- Contact an agent and ask for a rider quote.

- Compare costs and read the fine print.

- Complete the application and keep a copy.

- Schedule a yearly policy review.

Following these steps gives you a living‑benefits safety valve that can help cover bills, mortgage payments, or day‑to‑day costs when a chronic illness strikes.

Conclusion

You’ve seen how a living benefits life insurance for chronic illness can act like a safety valve when health turns tough. It gives you cash while you’re still alive, so bills don’t pile up.

All five major carriers we checked use the same 90‑day, two‑activity rule. That uniform rule makes it easy to compare costs and riders.

Now you can match the rider to your budget, your family’s needs, and the policy type you already hold. A quick call with Life Care Benefit Services can pull quotes from many carriers in one go.

Set a reminder to review your rider each year, premiums can shift and your health picture may change. If the cost feels high, ask about a lower rider percentage or a shorter waiting period.

Ready to protect your family’s future? Schedule a free consultation today and let a trusted guide walk you through the next steps.

Frequently Asked Questions

What is a living benefits life insurance for chronic illness?

A living benefits life insurance for chronic illness is an add‑on to a regular life policy that lets you tap part of the death benefit while you’re still alive if a chronic condition stops you from doing everyday tasks. The payout comes as cash you can use for medical bills, mortgage payments, or daily expenses, giving you a safety net when health turns tough.

How does the 90‑day, two‑activity rule work?

The 90‑day, two‑activity rule means the rider only pays out after you’ve been unable to perform at least two of the six daily‑living activities for 90 straight days. Those activities include eating, bathing, dressing, using the bathroom, moving around, and continence. Insurers use this uniform standard so you can compare riders across carriers without worrying about hidden thresholds. That way you know exactly when the benefit kicks in and can plan your finances accordingly.

Can I add a chronic‑illness rider to an existing policy?

Yes, you can add a chronic‑illness rider to most term, whole or IUL policies, but you’ll need to ask your carrier or agent to confirm that the specific product allows it. The process usually involves a short application, a rider endorsement, and a review of the policy’s existing language. Once attached, the rider follows the same 90‑day rule as any new policy.

How much does a rider usually cost?

Rider costs vary, but most carriers charge between $5 and $20 per month for every $10,000 of coverage you add. The exact amount depends on your age, health and the amount of benefit you choose. A quick quote from a Life Care Benefit Services advisor can show you how the extra premium fits your budget before you commit. Remember to ask if a lower percentage or a shorter waiting period can bring the cost down.

Who should consider buying this rider?

Families with a mortgage, small‑business owners who rely on steady cash flow, and seniors who want extra protection often find this rider useful. If you worry that a chronic condition could wipe out your income or force you to sell assets, the rider gives you a pool of cash to bridge the gap. It’s especially helpful when other insurance only covers medical bills, not living expenses.

How do I file a claim if I need the benefit?

To file a claim, start by gathering a doctor’s statement that confirms the diagnosis and explains how the condition limits two daily‑living activities for at least 90 days. Contact your insurer or the agent who added the rider, submit the medical paperwork, and fill out the claim form they provide. Once approved, the payout is usually sent as a lump sum within a few weeks.